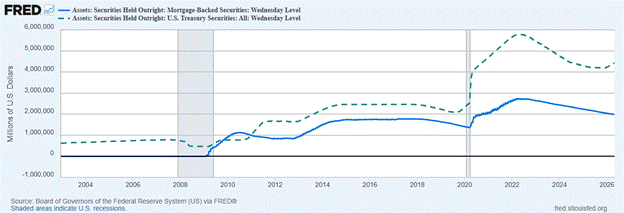

Remember Mortgage-Backed Securities (MBS)? Since the Financial Crisis of 2008, they became a multi-trillion-dollar tool for the Federal Reserve to artificially prop up the housing market through its money creation process. At its peak in 2022, the Fed’s MBS holdings reached $2.74 trillion. By most estimates, the Federal Reserve owned one-third of all mortgages in the United States.

Since 2022, as part of the Quantitative Tightening (QT) process, the Fed allowed these assets to roll off its books. However, since December 2025, the Fed has been increasing its purchase of Treasuries at a stated goal of $40 billion a month.

Even though the balance sheet continues to increase as expected from Quantitative Easing (QE), calling the process Reserve Management Policy (RMP) makes sense in retrospect. They are deflating the MBS balance while inflating their Treasuries balance. To understand the implications, let’s recap how the MBS process works.

When you take out a mortgage, there’s a high probability that the bank quickly sells your loan to a government-sponsored enterprise (GSE) like Fannie Mae or Freddie Mac. This is great for your bank because the debt leaves their books immediately. They get their money back to lend again and collect a small service fee over the life of your loan. It’s a brilliant setup: the bank faces no default risk, as it has been passed on to society.

Fannie and Freddie then bundle these mortgages into a MBS and sell them to private institutions, like insurance companies and pension funds, as well as the Federal Reserve since 2009. For an organization that should not exist to begin with, the Fed’s involvement in the mortgage market distorts the price of housing and the cost of credit. Nonetheless, the Fed appears committed to ending this process.

When you make your mortgage payment or pay off your loan, that money eventually flows back to the Federal Reserve. Normally, under QT, that money would be deleted from the system. However, the rules changed:

In December 2025, the Federal Reserve began purchasing Treasury bills through open market operations in order to reinvest principal payments on its holdings of agency mortgage-backed securities as well as maintain an ample supply of reserves on an ongoing basis.

The Fedspeak requires translation: As MBS balances decline, the Fed is no longer deleting the money. Instead, they are using those proceeds to buy U.S. Treasuries.

If executed perfectly, this swap allows the Fed to neutralize a shrinking money supply by swapping $2 trillion in mortgages for $2 trillion in government debt. The Fed would exit the mortgage market entirely, but its Treasury holdings would spike to a new high of $6 trillion-plus; but this also ignores the creation of all other new money to purchase additional Treasuries.

While a housing market without the Fed is a step closer to a free market, rolling over the proceeds to further entrench itself into the debt market is not a desired outcome. Even if the money supply remained perfectly static, the Cantillon Effect reminds us that where the money goes first is just as important as how much money exists.

As the Fed leaves the housing market, private actors like insurance companies and pension funds must step in to fill the gap. Rest assured, they will demand a higher rate of return for their efforts than the central bank did.

The Fed continues to re-arrange deck chairs on a sinking ship; but the causal-realist approach tells us there is an iceberg up ahead. And so, I’d rather just hear the band play.