In spite of more than four years of claiming that price inflation was transitory, and that it would quickly return to the Fed’s two-percent target, the Fed has insisted on more easy-money policy over the past 18 months. In that time, the Fed has cut the target interest rate by 175 basis points and has returned to quantitative easing through monthly $40 billion purchases of Treasurys. Through it all, Fed Chairman Jerome Powell has repeatedly described monetary policy using some variation of “restrictive.” In his most recent FOMC press conference, for example, Powell described the Fed’s policy as “borderline restrictive” or “modestly restrictive.” To be fair, this suggests a slight movement away from Powell’s earlier dubbing of US monetary policy as “relatively restrictive” late last year, and as “clearly restrictive” before that.

Indeed, it may be that current policy is “restrictive” compared to, say, the policies of Bernanke and Yellen. But recent data on the money supply suggests that the money supply in recent months is finding plenty of room to increase rapidly, in spite of what Fed officials say. All these claims of restrictive monetary policy fail to ring true when we look at actual movement in the money supply.

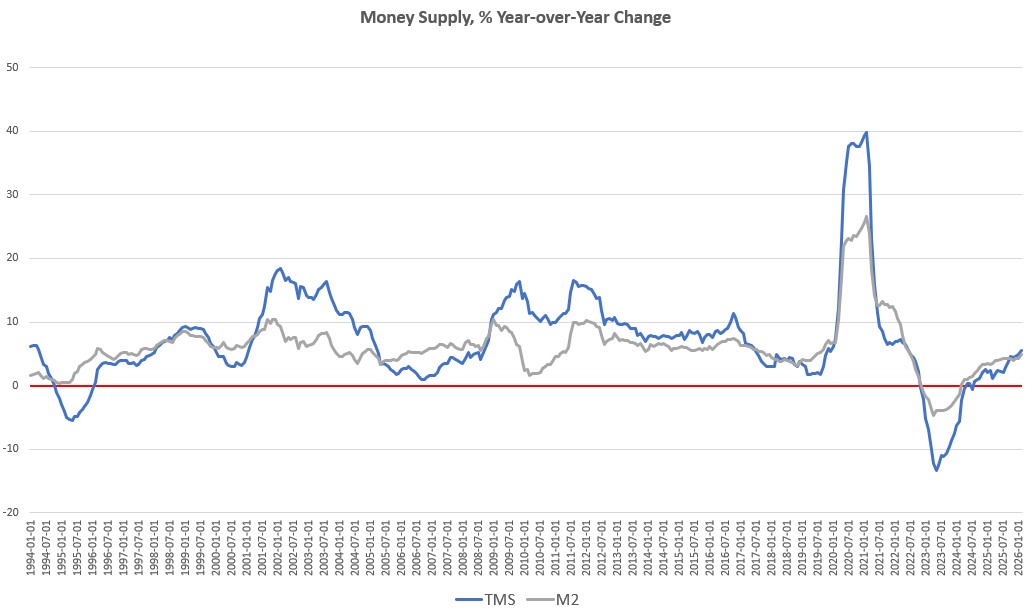

For example, the money supply has increased every month for five of the past six months. Moreover, when measured year-over-year, the money supply has accelerated over the past three months and is now at the highest rate of growth seen in 44 months—or since June of 2022.

While the money supply largely flatlined through much of the mid-2025, growth has clearly accelerated since August of last year, and has clearly been trending upward since June of 2023.

During February, year-over-year growth in the money supply was at 5.56 percent. That’s up from January’s year-over-year increase of 4.90 percent. Money supply growth is also up sizably compared to February of last year when year-over-year growth was 2.39 percent.

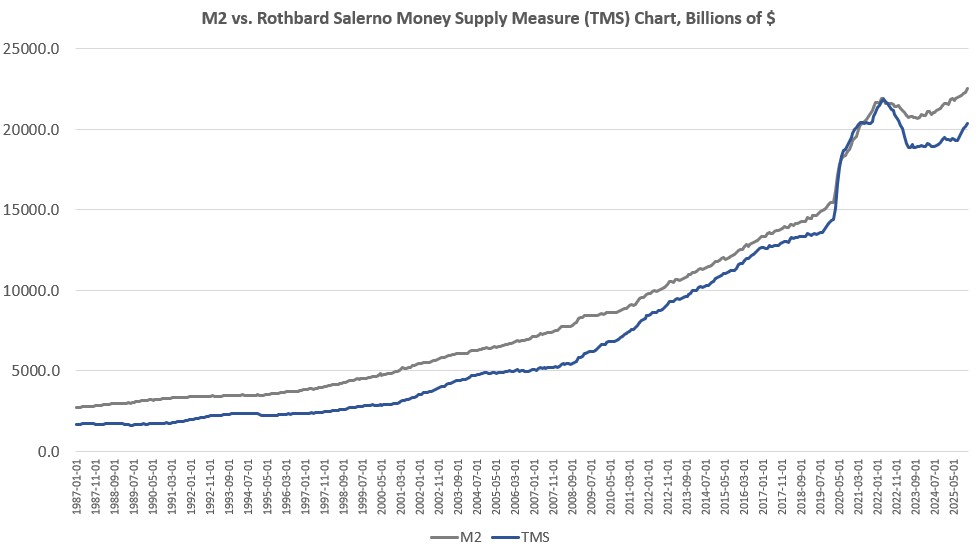

In February, the total money supply again rose, heading above $20.4 trillion and growing by a trillion dollars in seven months from July 2025 to February 2026. Although the total money supply fell throughout much of 2023 and 2024, the money supply has nonetheless increased by $1.6 trillion since that time, and is now only half a trillion below the covid-era peak.

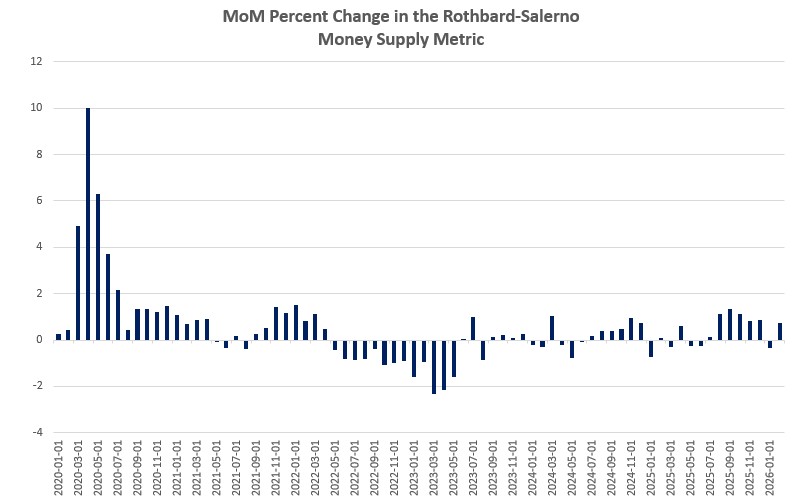

Measuring month-to-month growth, we find eight of the last twelve months with increases to the money supply, including substantial growth during November 2025, December 2025 and February of this year. August, September, and October all posted some of the largest growth rates we’ve seen since 2022.

The money supply metric used here—the “true,” or Rothbard-Salerno, money supply measure (TMS)—is the metric developed by Murray Rothbard and Joseph Salerno, and is designed to provide a better measure of money supply fluctuations than M2. (The Mises Institute now offers regular updates on this metric and its growth.)

Historically, M2 growth rates have often followed a similar course to TMS growth rates, but throughout much of 2025, M2 outpaced even TMS, and M2 money-supply totals are again rapidly heading upward. M2 is now at the highest level it’s ever been, topping $22.5 trillion. TMS has not yet returned to its 2022 peak, but is now at a 39-month high.

Since 2009, the TMS money supply is now up by more than 206 percent. (M2 has grown by more than 160 percent in that period.) Out of the current money supply of $20.4 trillion, nearly 30 percent of that has been created since January 2020. Since 2009, in the wake of the global financial crisis, more than $14 trillion of the current money supply has been created. In other words, more than two-thirds of the total existing money supply have been created since the Great Recession.

Given current weak economic conditions, it is surprising to see such robust growth in the money supply. For example, the estimate for GDP growth in the fourth quarter of 2025 was recently downgraded to 0.5 percent. And job growth since late 2025 has been either weak or negative, depending on which measure of employment we use. The Fed now concludes that job growth going into 2026 is essentially zero. This is likely reflected in the fact that consumer confidence has apparently fallen to a multi-decade low.

Given all this, we would not expect to see such robust growth in the money supply. Private commercial banks play a large role in growing the money supply in response to loose Fed policy. When economic conditions are expansive, and as employment grows, lending also grows, further loosening monetary conditions. But when economic conditions are weak, we’d expect to see less lending and bank-fueled monetary growth.

So, we should expect to see downward pressure on money supply growth given current economic conditions. However, in an effort to further pump asset prices and somehow counter our growing economic stagnation, the Fed again ratcheted up Fed Treasury purchases—paid with newly created money—and even lowered the target policy interest rate again in December.

This continuation of accommodative monetary policy—which belies Fed claims of “restrictive” policy—has surely done its part in returning the money supply to growth levels we haven’t seen in years.