In economic science, as with any science, appropriate, accurate, and precise terminology is essential, but there are often challenges to fitting real phenomena into established categories. In a previous article, “Massachusetts 1690: The First Western Fiat Experiment,” I examined the first experiment with government-issued bills of credit. This article answers the following question: according to Mises’s taxonomy of money, where do the bills of credit of colonial Massachusetts fit? This was warranted after some helpful clarifying questions about the previous article, further careful reading of Mises and examination of the event in question, and some reflection.

Massachusetts 1690: The First Western Fiat Experiment

In 1690, the Massachusetts Bay Colony issued what is widely regarded as the first government-issued paper money in the Western world. The bills of credit were introduced to pay soldiers returning from a failed expedition against Quebec, at a time when the colony lacked sufficient specie to meet its obligations. Given that these notes were not initially convertible into gold or silver, the episode is frequently cited as an early example of fiat currency and is therefore of particular relevance to debates over chartalism. If taxation alone can generate monetary value, the Massachusetts experiment should provide early historical confirmation of that claim.

Far from matching chartalism—especially strong, C-form chartalism, which claims monetary origination—the 1690 Massachusetts episode unfolded within an already-monetized economy in which gold and other commodities circulated as media of exchange. Colonial America operated in a context of multiple commodity monies that had emerged through market exchange. The paper experiment therefore did not create a monetary system; rather, it introduced paper notes into an environment already anchored by specie. Here the tension between chartalism’s role as a theory of monetary origin or as simply a description of modern monetary economies becomes evident.

The Massachusetts fiscal context is well known. After the aforementioned expedition, the colony found itself unable to pay returning soldiers. When attempts to secure a loan of £3,000–£4,000 from Boston merchants failed, the government resolved in December 1690 to issue £7,000 in bills of credit to meet its obligations. Significantly, the notes were introduced amid public skepticism about irredeemable paper. To facilitate acceptance, the government pledged that the bills would be redeemed in gold or silver out of future tax revenues and that no further emissions would occur, though these assurances proved short-lived.

Within months, the colony inflated the issue beyond the original amount, and the notes remained unredeemed for decades. By February 1691, the government declared that the initial issue had been insufficient and emitted an additional £40,000, again promising finality. Even in what is often described as an early fiat experiment, the initial circulation of the bills depended less on tax receivability alone than on assurances of future redemption and limits on quantity. As emissions expanded and redemption was deferred, confidence eroded. The public increasingly perceived the bills not as claims to future specie but as irredeemable paper whose quantity was subject to political discretion, and depreciation followed.

The episode therefore does not present an instance of money springing into existence by virtue of state decree or tax enforcement. The bills of credit were introduced into an economy whose monies and valuations were already defined by precious metals and other commodities through subjective valuations and voluntary exchanges. Their circulation rested on the expectation that they represented genuine claims on future specie and that their quantity would remain limited, framing them as circulating claims to money rather than as an independent fiat monetary standard.

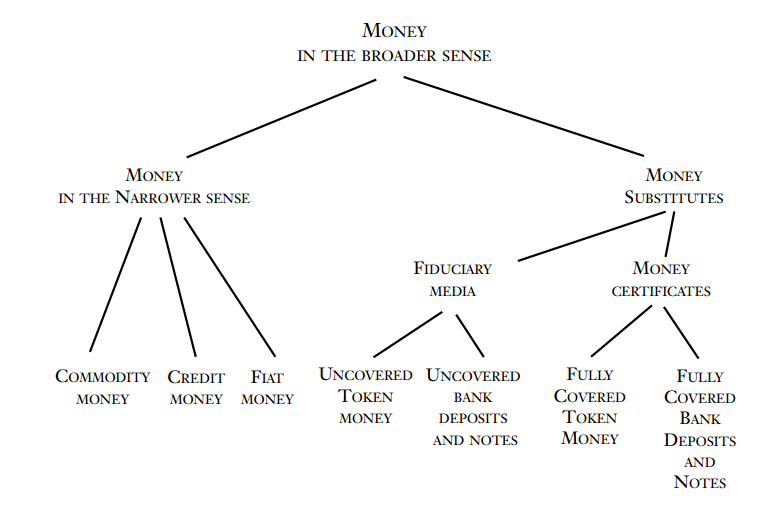

Mises’s Taxonomy of Money

In The Theory of Money and Credit (1912), Mises developed a taxonomy of money, which distinguished between different types of “money.” The question of this article is where to appropriately fit the colonial bills of credit issued by the Massachusetts government in 1690 and in the years immediately following. Thankfully, Guido Hülsmann has constructed a helpful chart, outlining Mises’s typology:

Figure 1: Mises’s Typology of Money

Using the above chart, alongside the more detailed definitions of Mises, where do the Massachusetts paper notes fit?

It is important to distinguish carefully—following Mises’s taxonomy—between money proper, money-substitutes, credit money, and fiat money. Money proper is a good that functions as the generally-accepted medium of exchange in its own right rather than as a claim to something else.

Money-substitutes are “absolutely secure and immediately payable claims to money,” that is, claims whose redemption into money proper is certain and available on demand, allowing them to circulate as if they were money proper.

Credit money, by contrast, consists of claims that circulate as media of exchange but are not necessarily redeemable on demand; as Mises explains, it is “a claim against any physical or legal person” whose payment may occur only in the future. In Hülsmann’s formulation, credit money “receives its value from an expected future redemption into some commodity” (emphasis added).

Fiat money is a medium of exchange that lacks redemption in money proper and circulates without being a claim to money proper.

Here we may notice the challenge of the case in question. Colonial bills of credit may seem to occupy a somewhat ambiguous position within this taxonomy. Because they were not immediately redeemable on demand, they did not constitute money-substitutes in the strict Misesian sense. Yet they circulated on the expectation of eventual redemption—whether through specie payments or tax retirement—and thus shared important characteristics with credit money. As redemption promises were postponed or abandoned, such bills could gradually evolve into irredeemable currency, that is, fiat money.

So where do the Massachusetts unbacked, government-issued notes fit best?

In answer to this question, it seems best to understand the notes as fiat money, with a few theoretical and contextual considerations. For one, fiat seems the most appropriate answer to what the notes, in actuality, were—unbacked paper money issued specifically because the government did not have money proper (i.e., specie) to cover its obligations.

Since these notes were not “absolutely secure and immediately payable claims to money” (emphasis added), they were not money-substitutes, however—and this is crucial—the Massachusetts notes were issued in a historical context of both money proper and genuine money-substitutes. In fact, Mises himself argues that credit money—“a claim against any physical or legal person” whose payment may occur only in the future or that which “receives its value from an expected future redemption into some commodity”—can only come into existence in a context of genuine money-substitutes,

If the State creates credit money – and this is naturally true in a still greater degree of fiat money – it can do so only by taking things that are already in circulation as money-substitutes (that is, as perfectly secure and immediately convertible claims to money) and isolating them for purposes of valuation by depriving them of their essential characteristic of permanent convertibility. (emphasis added)

What we may note here is that Mises identifies the possibility of a process by which “monies” can evolve—or rather, devolve—into other categories due to market phenomena and interventions. For example, commodity goods can become money proper by voluntary use as media of exchange. Paper notes can become money-substitutes if they are absolutely secure and immediately-redeemable claims to money proper. What were once true money-substitutes can become credit money or even fiat money by cancelling their role as immediate claims to money proper. In fact, from Mises’s analysis, it seems that certain types of “monies” are only possible given the preexistence and presupposition of other types of monies. Mises wrote further, “The attempt to put credit money into circulation has never been successful, except when the coins or notes in question have already been in circulation as money-substitutes.” Therefore, credit money and fiat money only become possible once people are accustomed to and trust genuine money-substitutes. States can, and do, take advantage of the existence of money-substitutes and—through their interventions—transmogrify them into credit money and even into fiat. Mises, again, states,

What the State can do in certain circumstances, by means of its position as the controller of the mint, by means of its power of altering the character of money-substitutes and depriving them of their standing as claims to money that are payable on demand, and above all by means of those financial resources which permit it to bear the cost of a change of currency, is to persuade commerce to abandon one sort of money and adopt another. That is all. (emphasis added)

Thus, while ultimately determining that the Massachusetts colonial bills of credit were technically fiat, it is important to note the prior monetary context that made issuing fiat possible, as well as recognizing that the notes were not presented to the public as pure fiat, but as credit money. According to the historical record, when Massachusetts issued these bills, they came with explicit promises of eventual redemption in specie (gold or silver). This promise was crucial for initial public acceptance and was only believed because money proper and genuine money-substitutes already existed. The colonial government understood that people would not readily accept mere pieces of paper without some connection—even if only promised—to real money. A more precise way to answer the question of the article is that the Massachusetts notes were fiat money that was fraudulently presented to the public as credit money.

In other words, it was a bait-and-switch where the “bait” was the announcement of credit money and future redemption promises and the “switch” was unbacked fiat currency. It is key to realize that—for bait to be tempting—it has to resemble the real thing. This explains why and how fiat monies can circulate as media of exchange since they were originally linked to preexisting money or legitimate claims to money, which gave them initial purchasing power and market demand.

It should also be noted that, even if some of these notes were eventually redeemed in specie, this would be at taxpayer expense, depend on whether the government actually had specie available, and would arguably transmute the fiat currency back into a money-substitute, usually years later and at a depreciated rate. One source reports, “An aggregate of £40,000 for this and the previous issue of Colony or Old Charter Bills was authorized by the Feb. 3, 1690/91 and May 21, 1691 Orders. These were receivable by Treasurer for taxes at 5% premium or payable at par with any specie on hand in the Treasury” (emphasis added). This meant that the government-issued notes were more valuable for paying taxes than specie and, while they could sometimes be redeemed for specie with the treasury, this was “with any specie on hand in the Treasury,” which was often none. This represented partial specie redemption through taxation rather than true specie redemption. In reality, very little actual specie redemption took place. Many of the notes were “redeemed” through taxation and then retired or burnt.

The Massachusetts bills represent a more sophisticated form of fiat money than a simple irredeemable paper currency. Through a combination of tax receivability, limited conditional specie redemption (when available), legal tender laws, and continuous reissuance, the colonial government created a monetary system that maintained the appearance of backing while operating as fiat money in practice.

The process Mises described seems more aligned with the bills of credit in the story of colonial America. Goods exchanged via barter, certain goods with money qualities began to trade and circulate as media of exchange, key goods became generally-accepted media of exchange, money-substitutes—secure and immediate claims to money proper—emerged, governments wanted to expropriate purchasing power and tax via inflation, they introduced paper notes with promises of future redemption and limits on issuance, accepted the bills in settlement of tax obligations, privileged the bills with legal tender laws and other legal interventions to compel acceptance, then Gresham’s Law encouraged the limited use of the bills instead of other monies, and the governments gradually severed the link between these notes and money proper, pushing them into the status of unbacked fiat.

What often gets overlooked is that governments can compel the acceptance of fiat money, but only gradually and with prior connection to money proper. The link is crucial in encouraging acceptance and maintaining confidence. Over time, as the connection is removed and convertibility is no longer an option, the fiat is still limitedly accepted—unless there is hyperinflation—because it already circulated as a medium of exchange. Writes Hoppe,

Yet without a doubt the coexistence of money and money substitutes and the possibility of holding money in either form and in variable combinations of such forms constitutes an added convenience to individual market participants. This is how intrinsically worthless pieces of paper can acquire purchasing power. If and insofar as they represent an unconditional claim to money and if and insofar as no doubt exists that they are valid and may indeed be redeemed at any time, paper tickets are bought and sold as if they were genuine money—they are traded against money at par. Once they have thus acquired purchasing power and are then deprived of their character as claims to money (by somehow suspending redeemability), they may continue functioning as money. As Mises writes: “Before an economic good begins to function as money it must already possess exchange-value based on some other cause than its monetary function. But money that already functions as such may remain valuable even when the original source of its exchange-value has ceased to exist [Mises, Theory of Money and Credit, p. 111]. (emphasis in original)

Conclusion

The Massachusetts case therefore does not present an instance of fiat money springing into existence by virtue of state decree or tax enforcement. The bills of credit were introduced into an economy whose monies and their respective valuations were already defined by precious metals or other commodities. The fiat paper money issued by the Massachusetts government circulated based on assurances that they would function as credit money—claims on future specie—and that their quantity would remain limited. Even if those commitments were not ultimately honored, they framed the notes as circulating claims to money rather than as an independent monetary standard. Importantly, this episode demonstrates that a currency does not necessarily remain rigidly in one monetary category but can evolve or devolve and that certain monetary categories necessarily presuppose the prior existence of others.