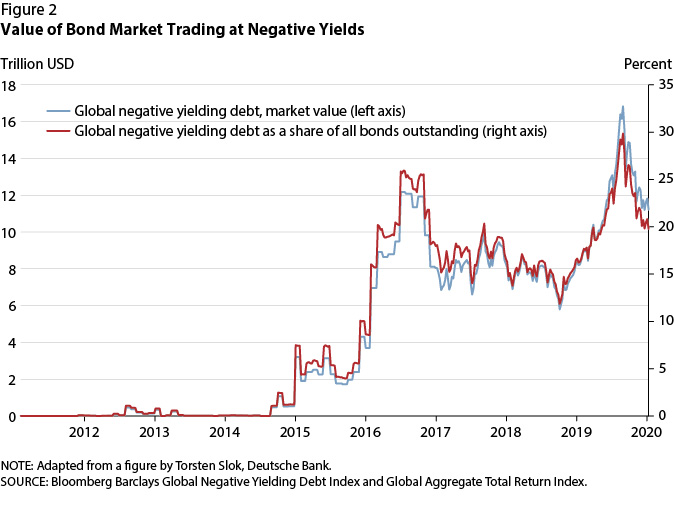

With over $12 trillion in negative-yielding debt and the yield on the ten-year Treasury bond falling below 1 percent for the first time, the days in which people could reliably count on a steady stream of income from their assets seem to be a thing of the past. And although most people would have a hard time finding anything positive about this state of affairs, it is actually a part of the grand vision set forth by the father of modern macroeconomics, John Maynard Keynes.

In the last chapter of his influential 1936 book The General Theory of Employment, Interest, and Money, Keynes concludes by inferring a number of lessons from his previous discussions. One of those lessons became famous for the phrase it contains, “the euthanasia of the rentier”: the notion that once high interest rates become history due to expansionary monetary policy, the class of people who live off their savings will gradually and silently disappear. But why did Keynes advocate low interest rates in the first place, and embrace the annihilation of the rentier class which it would bring?

Keynes’s Theory of Interest

For Keynes, interest is a purely monetary phenomenon, determined on the market by the demand for, and the supply of, money. As such, it is divorced from people’s ability to save and thus accumulate capital. Instead, interest is “the reward for parting with liquidity,” equilibrating individuals’ liquidity preference with the supply of money.

If this is true, it is quite easy to see why Keynes favored low interest rates. Whenever the economy falls below full employment, the monetary authority could simply increase the supply of money, and given that liquidity preferences stay constant, the interest rate would fall, thus stimulating private investment and bringing the economy back to full employment.1

What justification, then, could there be for people who live off high interest payments? None, according to Keynes. There should be no reason to tolerate the existence of people who contribute nothing to society and only “exploit the scarcity-value of capital.” Armed with Keynes’s theory, governments could lower the interest rate to zero, thus increasing “the volume of capital until it ceases to be scarce, so that the functionless investor will no longer receive a bonus.”

It is safe to say that today no serious economist subscribes to this theory of interest. In fact, this part of Keynes’s General Theory was one of the first to be abandoned by his followers. However, in practice things are not much better. Mainstream economists and bureaucrats still view the interest rate as a policy tool that can be manipulated ad libitum. And as short-term interest rates around the world are either negative or barely above zero, we are coming ever closer to Keynes’s vision of a world without the rentier.

The Austrian View

The Austrian view of the nature and function of interest couldn’t be any more different. First, for Austrians, interest is a real phenomenon that precedes the use of money and would even exist in a Robinson Crusoe economy. It a result of the universal fact of time preference—the premium on present satisfaction over future satisfaction—and is thus embodied in the prices of all durable goods, not just those of financial assets. Yet it is only in the market economy, where economic calculation in money prices is possible, that the interest rate receives its starkest manifestation in the loan market. In sum, interest is determined by individuals exchanging future money against present money at a discount, this discount being governed by their time preference.

Second, interest preforms an allocating and equilibrating function. If people’s time preference increases and consequently interest rates rise, it means that people are more present-oriented and would like to consume a greater part of their income in the near future. Profit-seeking entrepreneurs must then shift resources from the production of producer goods to that of consumer goods, thereby adjusting the structure of production to the preferences of consumers. By manipulating interest rates, governments can only interfere in the natural adjusting process that occurs on the market. And since this interference necessarily disrupts the economic calculation of entrepreneurs, it may also lead to the construction of malinvestments and, ultimately, the business cycle.

With this in mind, what is the “Austrian” view of the rentier? First, it should be pointed out that the rentier participates in voluntary exchange, thereby benefiting not only himself but also others. Second, due to his relatively low time preference, the rentier can amass a large amount of capital. This capital is then invested and used to increase the productivity of workers, thus contributing to higher wages and a higher standard of living. Contrary to Keynes, then, the rentier, far from being a villain, is actually (in the spirit of Walter Block) a hero.

Conclusion

Over eighty years ago, Keynes condemned the rentier and welcomed his disappearance. Following in his footsteps, politicians and central bankers today are ever closer to effectively bringing this about. Austrian economics teaches us that this view is not only wrong but also potentially dangerous. Let us, then, celebrate the rentier and wish him many more years to come.

- 1It is worthwhile to note that Keynes doubted the effectiveness of this mechanism due to (1) the reluctance or inability of the central bank to lower long-term interest rates, (2) rising liquidity preferences in the face of general uncertainty, and (3) the hypothetical case of a liquidity trap.

{kind=link}