Twice a year, the Federal Reserve releases its Financial Stability Report. According to the Fed:

This report presents the Federal Reserve Board’s current assessment of the stability of the U.S. financial system.

By design, it can already be considered a lagging indicator upon publication, but it perfectly illustrates what Kevin Warsh meant when he noted that the regulators are always the last to know. However, the report is still useful, if for nothing else than to see what exactly the Fed is looking at on the horizon.

They begin with asset valuations, noting:

Asset valuations stayed at the high end of their ranges in most markets. Measures of broad equity valuations remained elevated.

With the stock market continuously printing record highs, their observation might not mean much to the average person. What might be new is that, according to the Fed’s evaluation:

U.S. farmland values remained elevated based on annual data as of December 2025.

The Fed cites limited farmland inventory as the main culprit, keeping prices propped up despite higher interest rates and soaring operating costs.

As for residential house prices, the report notes:

House price growth has continued to moderate over the past several years.

But aggregate indices rarely tell the full story. Trying to average out urban centers versus rural America, or the East versus the West Coast, is rarely informative.

Some statistics can offer food for thought at least:

Mortgage debt accounted for roughly three-fourths of total household debt.

Considering that a home is likely the most expensive asset most people will ever buy, the mortgage (French for death pledge) remains the heaviest debt load a person will carry. As the Fed continues to shrink its Mortgage-Backed Securities (MBS), the housing market remains a sector to watch.

When it comes to systemic leverage, the Fed reveals that hedge funds, which command nearly $14 trillion in assets, have pushed their gross leverage ratios to record highs.

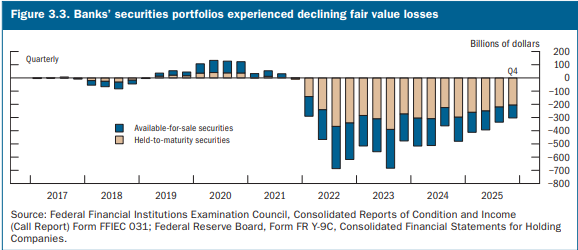

Perhaps the best diagnostic warning lies within the banking sector:

The fair values of banks’ available-for-sale (AFS) and held-to-maturity (HTM) portfolios were below their book values by a combined $300 billion at the end of 2025.

Contrary to popular belief, rapidly raising or sustaining high interest rates does not necessarily make a net-positive for commercial banks, as it makes the value of their fixed-income bonds drop significantly; in this case by $300 billion.

Should even a localized market panic arise and force banks to liquidate those assets early to meet redemptions, these paper losses instantly turn into real losses and banking failure. Yet at the same time, this is always the risk in a fractional reserve banking system.

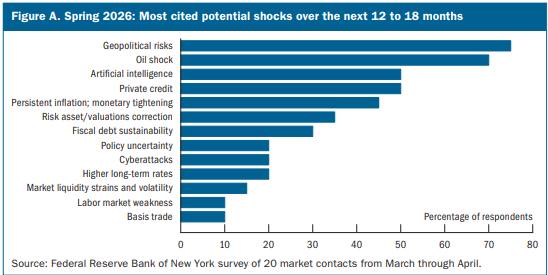

So what keeps central bankers up at night?

When the Fed surveyed its market contacts about near-term vulnerabilities, respondents didn’t actually lead with debt levels or interest rates. And while they didn’t cite the office of the president, they did note geopolitical risks and oil/energy shocks as the primary threats to financial stability.

Naturally, when the Fed’s cheap-credit-induced bubble leads to an inevitable Black Swan, I’d wager that it might not even come from the threat that central planners are anticipating the most. Sometimes it’s the risks that can’t be seen that become the riskiest of all.