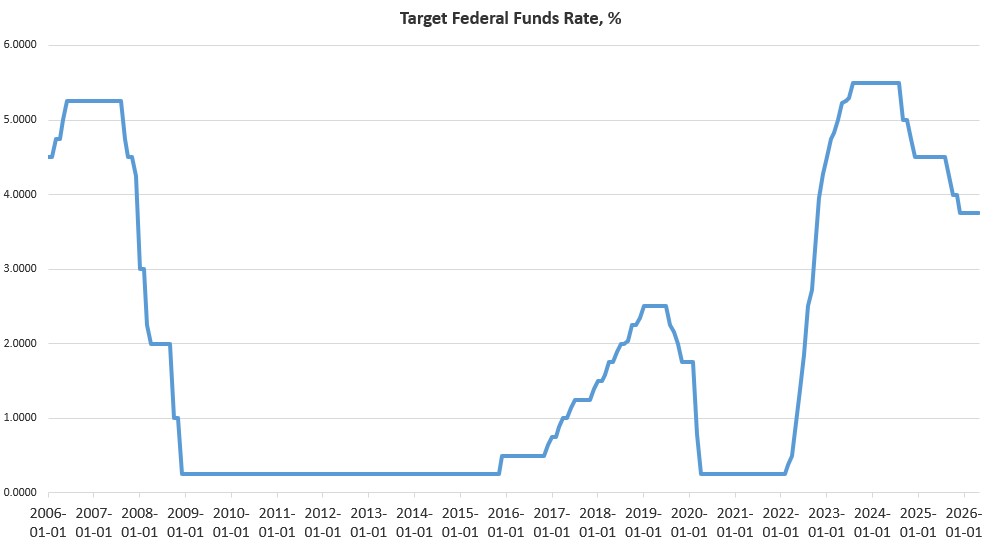

The Federal Reserve’s Federal Open Market Committee Today announced that it will keep its target policy interest rate at 3.75 percent. The FOMC has held to this target now for seven months, but has reduced the target rate by 175 basis points since August 2024. The committee’s statement, released this afternoon, is considerably shorter than those released by former chairman Jerome Powell, coming in at only 125 words. The statement reads:

The Federal Open Market Committee approved the following statement for release by a 12 – 0 vote:

The Committee decided to maintain the target range for the federal funds rate at 3-1/2 to 3-3/4 percent, in support of the Federal Reserve’s dual mandate. The Committee reaffirmed its policy of maintaining ample reserves in the banking system.

Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little.

Inflation remains elevated relative to the Committee’s 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability.

FOMC press releases are not neutral factual statements, but are political communications, designed to send a political message. I suspect the most important part of this particular press release is the first sentence indicating that the policy was decided unanimously. It was likely very important to both Warsh and Fed that the Fed be seen as a “serene” institution with few internal conflicts. The announcement of unanimity was key to this. The fact that former chairman Jerome Powell still sits on the FOMC as a member of the Fed’s Board of Governors, offered some potential for conflict, although few anticipated Powell would actually do anything to try to question Warsh’s policies at this point.

Not surprisingly, the FOMC does include text claiming that the state of the economy is good, in this case, stating again—as with other recent committee statements—that economic growth is “solid.”

On the other hand, the new press release does not include the text from April’s statement saying that the FOMC “is strongly committed to supporting maximum employment.” Some observers have suggested this points toward a more hawkish Fed. This notion is supported by the fact that the FOMC release concludes with the statement “The Committee will deliver price stability.” Indeed, during the press conference following the FOMC meeting, new chairman Warsh emphasized at least twice that “the committee will deliver price stability,” while also noting that the Fed under Powell, for the past five years, has never managed to get the official price inflation measure down to the Fed’s target of two percent.

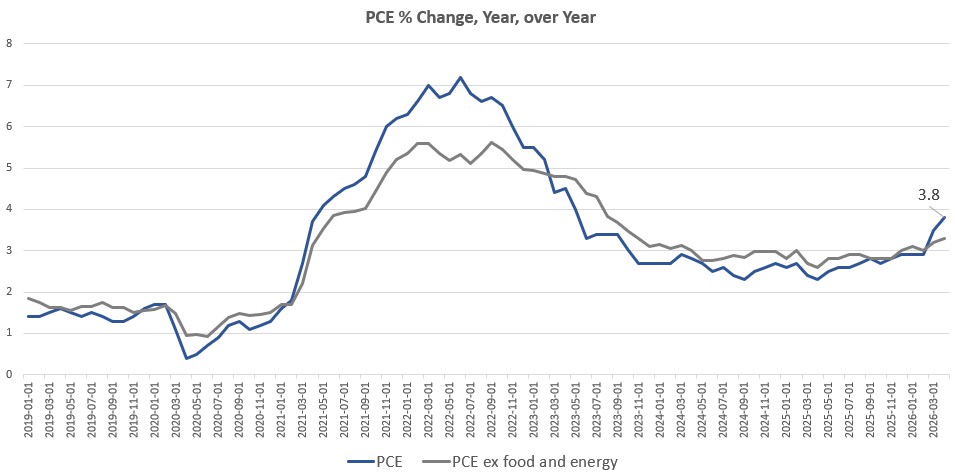

It is unclear if this (very mild) turn toward slightly more hawkish rhetoric comes from a difference in policy between Warsh and Powell. It could be that this emphasis on “price stability” has been forced on Warsh and the committee by accelerating inflation growth which is increasingly apparent in recent price-inflation reports from the BLS. In May, for example, 12-month growth in the CPI hit a 38-month high, while the producer price index hit a 42-month high. The most recent PCE reading (from April) shows that the PCE remains well above the Fed’s target rate of 2 percent. In fact, the PCE has been moving up, and rose in April to 3.8 percent, a 30-month high.

This continued movement in price inflation away from the Fed’s target has prompted markets to assume that the Fed may actually turn to a hike in the target policy interest rate before the end of the year. This idea was reinforced by the most recent Statement of Economic Projections—also released today by the FOMC—which suggests that FOMC members plan an increase to the target rate. CNBC put it this way:

Based on the 18 of 19 possible responses, the median estimate for the fed funds rate at the end 2026 is now 3.8%, up from 3.4% in the prior projections from March and signaling the committee sees at least one rate hike as necessary this year.

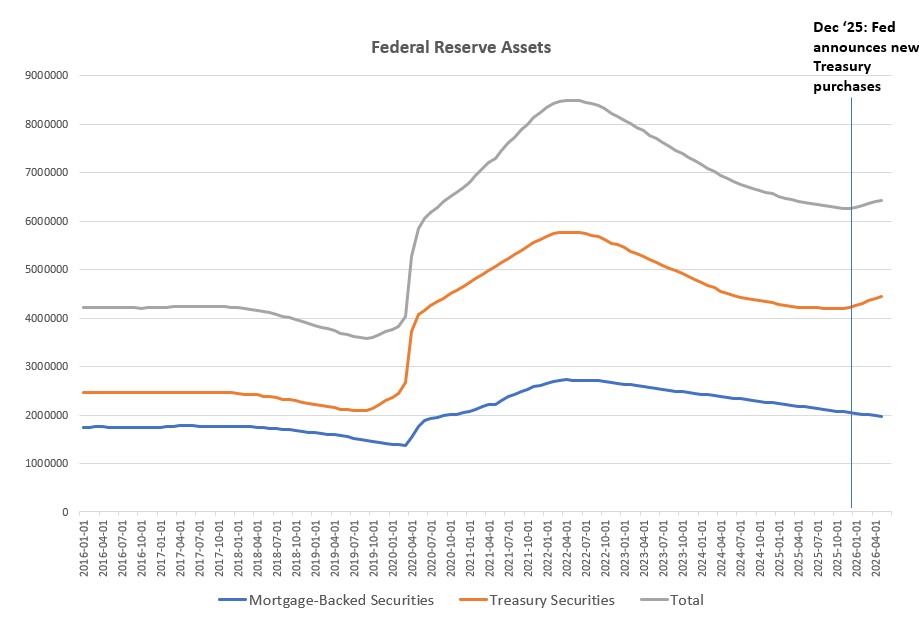

Just how “hawkish” the committee plans to be will depend a lot on the FOMC’s policy toward the Fed’s huge $6.7 trillion balance sheet. Since December, the Fed has been engaged in easy-money policy in the form of new additions to the balance sheet. These purchases are carried out with newly created money and have the effect of adding new money to the economy and thus are a type of dovish monetary policy. The Fed’s balance sheet is now higher than where it was a year ago in spite of repeated claims from the Powell Fed that monetary policy was restrictive.

Indeed, over the past six months, the Fed’s purchases have, in part, helped push the money supply growth rates to a 48-month high, as of April. The Fed has added more than $160 billion to its assets in 2026. There was little mention of the balance sheet during the FOMC press conference, however, except a statement from Warsh that he plans to create a task force that will review the Fed’s policy on the balance sheet.

Whatever this “task force” may decide, the Fed will be greatly constrained by economic realities. Whatever the Fed may say about the economy being “solid,” the more on-the-ground reality for many Americans is one of stagnant job growth and declining real wages. Given that the Fed tends to always view monetary inflation as the solution to lackluster economic growth, it will surprising if the Fed engages in any serious or rapid reductions to the balance sheet. Were the Fed to pull money out of the economy via asset sales, this could upset the Fed’s efforts to maintain the current effort to inject economic stimulus in the face of what the Fed knows is is a fragile economy heavily dependent on the maintenance of easy-money-fueled bubbles.

Warsh has nonetheless managed to buy some time with the creation of his new “task force” plan which he says will result in reports from “experts” around the end of the year. This will allow Warsh to basically point to November or December as the expected time for any actual policy changes. Until then, the reality of the FOMC and the Fed overall appears to be what we got from Powell during his tenure: with each new month, simply state that the Fed is “concerned” about inflation and that the Fed is “data driven,” decide policy as new realities require.

In other words, once we look beyond a small shift in rhetoric and emphasis, there is, so far, no reason to believe that the Fed is headed toward anything other than business as usual.

Image Credit: Federal Reserve