Fears over price inflation returned in a big way this week as bond yields rose in the wake of recent government reports on consumer and producer prices. The US-Israel war on Iran continues to take a toll on global supply chains, and related price hikes appear to be partly driving growth in long term yields for both US, British, and Japanese debt.

This week’s CPI and PPI reports both showed price inflation surging to multi-year highs, and not just on oil prices. This, combined with new increases in oil prices, appears to have spooked investors who are now, in the face of rising prices, are demanding higher yields for long-term debt.

Yahoo!Finance reports:

The 30-year Treasury yield rose 12 basis points to reach 5.13%, its highest closing level since June 2007. The 10-year benchmark yield, meanwhile, climbed 13 basis points to 4.59%, its highest level since May 2025.

Nor are US bonds the only casualties here:

The yield on 30-year UK government bonds reached 5.869 percent, surpassing Tuesday’s mark to hit its highest level since 1998, as investors demanded higher returns to reflect growing inflation risks.

In Japan, the 30-year bond rate hit four percent for the first time since 1999.

Meanwhile, the Trump summit with China’s premier has done little to cap global fears over oil prices. Rather, oil prices gained another two percent on Friday with Brent crude futures rising over $108 per barrel.

Indeed, Trump’s failure to secure any significant cooperation from Beijing in pushing Tehran to open the Strait of Hormuz ensures that restricted global supply—combined with central banks’ continued monetary inflation—will lead to more price increases. The US initiated its new war on Iran on February 28, and the resulting decline in oil and oil-related production is now showing up in US price-inflation statistics.

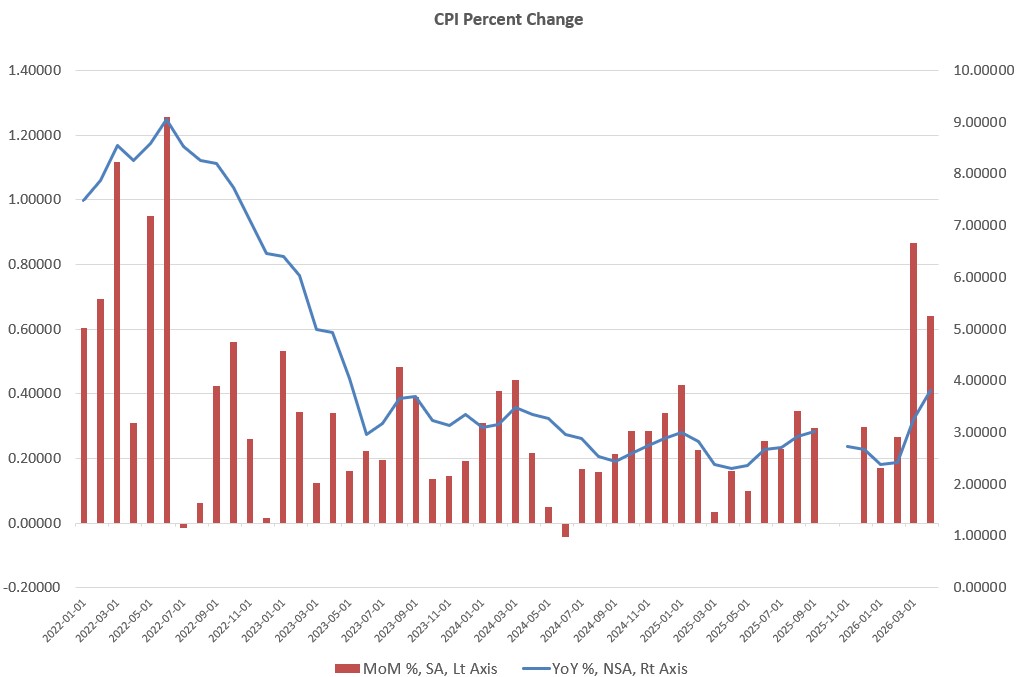

On Tuesday, the US Bureau of Labor Statistics released new CPI data showing substantial increases in prices inflation for the Month of April. According to the report, the index was up by 3.8 percent, year over year, for April. That’s the largest year-over-year increase in 36 months. Month over month, the CPI was up by 0.64 percent. That was down from the month-over-month increase for March, but was the second largest monthly jump since June of 2022.

Part of these sizable increases were due to a jump in energy prices, largely stemming from the US war on Iran. Year over year, the CPI for energy rose in April by 17.9 percent, with gasoline up by 28.4 percent for the period. Moreover, nearly all major categories of the CPI showed increases in excess of the Fed’s two-percent target. The index for food was up in April, year over year, by 3.2 percent, and shelter was up by 3.3 percent over the same period.

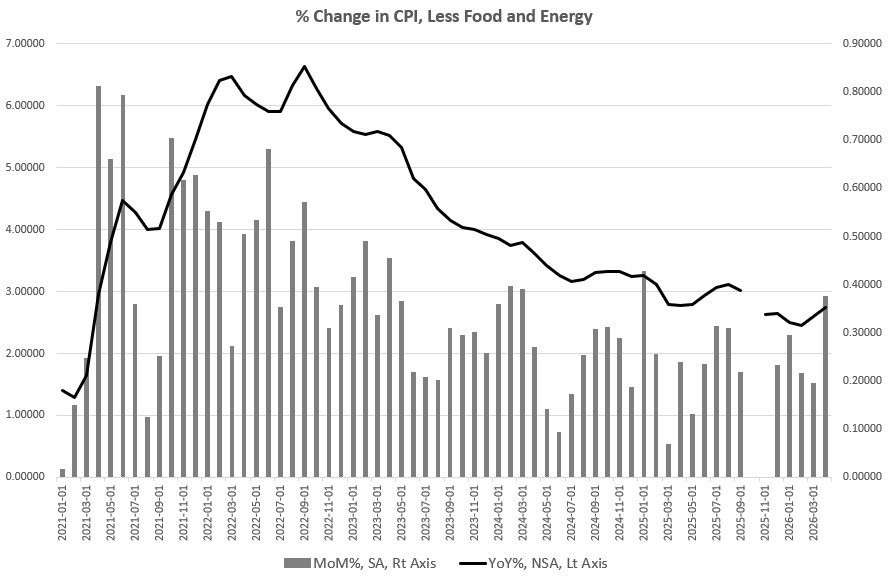

Even if we look to core CPI (and thus remove food and energy from the index) we still find an upward trend. Year over year for April, the index was up by 2.7 percent, the largest increase in seven months. The month-to-month increase for April was 0.37 percent, a sixteen-month high.

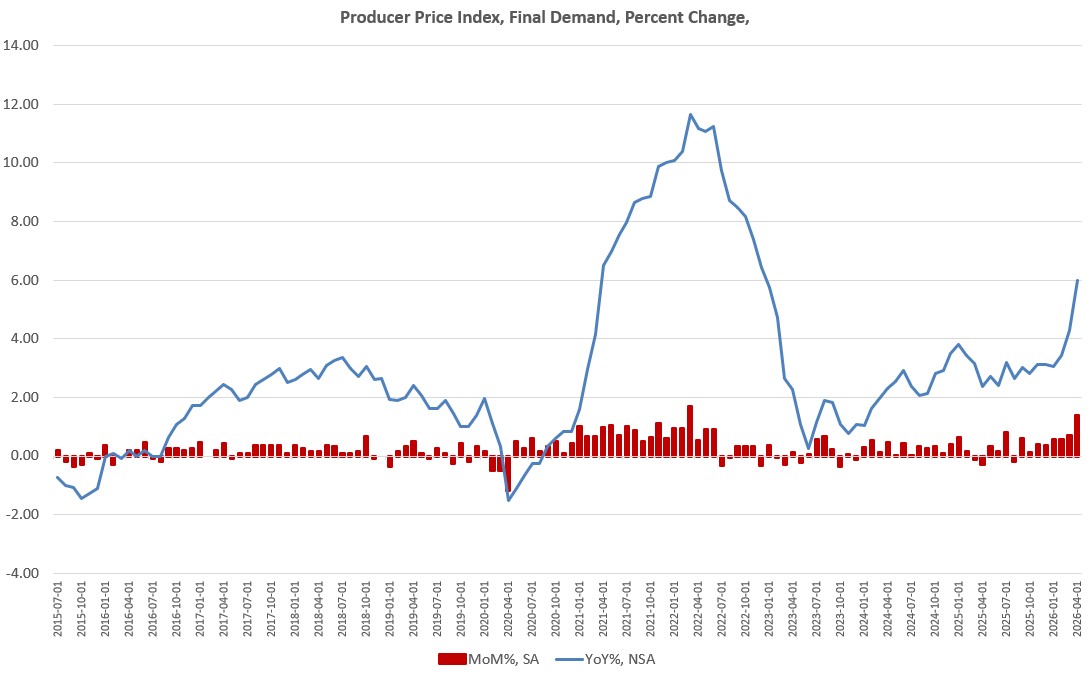

The upward trend in prices was further confirmed by the release of the new producer price index (PPI) data on Wednesday. The PPI showed a year-over-year increase of 5.9 percent for April. That’s the largest jump in 39 months—since February of 2023. Month-over-month, the PPI was up by 1.37 percent for April, the largest increase in 50 months.

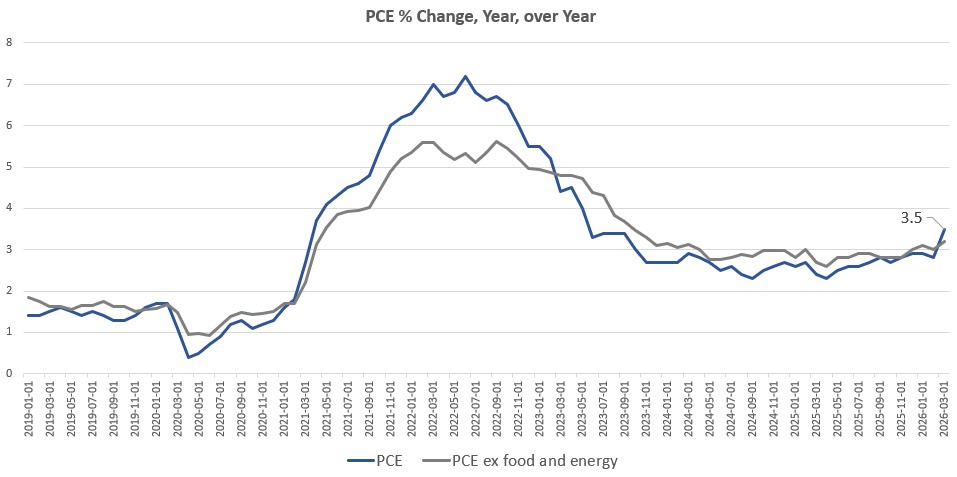

We might also add that the Fed’s favored measure of price inflation, the personal consumption expenditure (PCE) index, also appears to be accelerating. We don’t have the April measure yet for PCE, but March’s year-over-year increase was 3.5 percent. The current trend in CPI suggests that April’s increase will be even larger than March’s.

Not only is the Iran war causing a decline in global output, but the world’s central banks continue to embrace easy-money policies. This will result in more dollars (or sterling, euros, or yen, etc.) chasing fewer goods. This will further fuel rising prices. This is why we continue to see a general rise on prices. If rising prices were merely a result of falling output in Persian Gulf related goods, then we’d see rising prices in some areas result in falling prices in other areas. In other words, if the money supply were reasonably stable, consumers would respond to rising prices in some areas by cutting spending in other areas. But the CPI suggests that’s not happening. Thanks to continual infusions of new money through loose monetary policy, consumers are able to continue bidding up prices in all areas, even as price increases in the energy sector rise to multi-year highs.

Given all this sobering news about price increases, it’s not difficult to see why many bond investors have lost their appetite for long-term debt at low yields. As a result, prices are falling for long-term bonds, driving up yields. To this uncertainty over inflation, we can further add ongoing large infusions of new government bonds to finance ever larger deficits. Thanks to the US war on Iran, we can expect even larger deficits throughout this year. After all, even before the US launched the war in late February, the US was headed toward one of the largest annual deficits ever. These additional war costs will also further inflate deficits. These deficits will have to be financed by new debt, which will put downward pressure on bond prices.

This will ultimately be a problem for zombie companies and highly indebted enterprises that have long relied on constantly falling interest rates to keep up with debt service. Moreover, unless something changes soon, the housing sector will have to start planning for a significant period of higher mortgage rates.