Politicians of both parties constantly say and do things that make no sense in terms of the goals they publicly claim to be pursuing. This illogical dimension of political bloviation supports Ludwig von Mises’s contention that, even if one sets aside ethical arguments about ultimate goals, a value-free understanding of the logic of purposeful human action—economics—is often sufficient to refute whatever public justifications politicians offer for their policies, as such policies simply don’t lead to the results they claim to want.

Of course, the actual goals that politicians and their sponsors really have in mind often diverge radically from what they tell the public. One always has to make a generous allowance for how democracy incentivizes hypocrisy by sophisticated politicians in spite of them often having a pretty good idea what their policies really entail.

However, some politicians are just so devoid of common sense that one is forced to conclude that they are not merely deceivers, but are also grotesquely ignorant. Even at the risk of becoming infected with a “Derangement Syndrome,” I can’t help but get into a high dudgeon about some of the inane things President Donald J. Trump has been saying about the economy. The latest examples involve the soaring cost of living (which even the official Consumer Price Index can’t hide now in spite of the CPI’s biases) and Federal Reserve interest rate policy.

When asked at a June 10 press conference about the CPI’s annual rate of increase reaching 4.2 percent, Trump declared, “I love the inflation.” Trump tried rationalizing this love by boasting that the US Navy has been sneaking tankers past Iran’s Hormuz blockade and boasting about stock markets hitting record highs in early February.

That wasn’t a misquote; Trump actually said I love the inflation—do take a moment to let that sink in.

Trump also weighed in on Federal Reserve policy in a contentious interview by Kristen Welker for NBC’s Meet the Press on June 7. Welker noted that, given the latest jobs reports, economists were saying that the Fed might have to raise interest rates. Trump responded:

We’re doing great, and it’s unfair that whenever you do great, they want to raise interest rates. It should be the opposite way. You know, if you go back 15 or 20 years, when you had good reports, the market went up. Nowadays when you have good reports, the market goes down because they think they’re going to raise interest rates. There’s no reason to raise interest rates. The country becomes great. We built the country by doing great and having rates low. What they do is when they raise interest rates, they try and kill success. I don’t want to kill success. We should actually lower interest rates. Now, if inflation comes, and, you know, people live with inflation, but if inflation comes what happens is you stamp it out. But success can kill inflation just like higher interest rates. What they do now is, like, we had great job numbers. You agree, right?

A follow-up question prompted further agitation for faster Fed money-creation:

I would like to see rates get lower because we could build this into the greatest machine that the world has ever seen, but you can’t do that when everybody immediately raises interest rates. So we had great job numbers. We’re doing great. You know, we’re building more factories. We have more money coming into our country right now from other countries and people than ever before. Wait a minute. What happens? I don’t want to just kill it with high interest rates. Growth is the greatest thing you can have, and growth does not cause inflation.

Jobs are doing great? Really? Most Americans—even those completely ignorant of economics—know all too well from personal experience that there is nothing to love about rising consumer prices, especially when they are rising faster than their wages are. Official reports (especially when corrected for CPI biases) confirm that living is becoming less affordable for many workers, with hopes of building careers, buying homes, and starting families being crushed. Trump’s newfound love violates all common sense.

Understanding a little economic theory further exposes Trump’s economic incoherence, which menaces even those whose stock portfolios are currently thriving.

First, consider Trump’s unconstitutional aggression against Iran. In spite of claimed successes in sneaking oil past the Iranians, global supplies of oil and other vital inputs have been sharply curtailed and prices raised significantly above prewar levels. Waging war also compels the Pentagon to consume more goods at the expense of civilian goods. Warfare also damages industries that have the misfortune of being located in the war zone, further diminishing future global production. The Producer Price Index is soaring even faster than the CPI, which is very bad news for future price trends. More severe input scarcity translates into lower earnings and living standards for everybody.

There will be enormous pressure on politicians to provide additional bailouts and handouts to mitigate such suffering, which, in turn, only further sabotages production and prolongs the time needed for recovery even if Hormuz were to fully reopen tomorrow. Just as we haven’t entirely recovered from the negative impacts of Trump/Biden COVID lockdowns or from Trump’s tariffs yet, we won’t recover from the Trump/Netanyahu war any time soon either.

Second, consider the recent stock market rally. Growth-oriented shareholders (and others counting on capital gains like real estate speculators) must beware of a looming economic downturn as the present bank credit-fueled boom runs its course. Permabull biases of financial media outlets make them reluctant to warn investors about the risks of AI stocks crashing hard or of Wall Street needing another gigantic bailout as the rest of the economy gets mired in another years-long depression, but that is precisely what investors ought to be worrying about right now. 401(k) accounts stuffed with volatile boom sector stocks can go down even faster than they have gone up.

Third, consider the Federal Reserve’s interference with interest rates. What the Fed does with the help of commercial banks is to push interest rates below their laissez-faire free market levels via money creation, thus generating temporary booms in interest-sensitive parts of the economy. Such booms aren’t sustainable because non-boom sectors are starved of inputs, driving up input prices relative to output prices, eventually making boom sectors unprofitable. Continually driving down interest rates even after a bust sets in only prolongs the squeeze on operating margins needlessly and thwarts a recovery, much like what Americans experienced from the 2008 financial crisis until 2014 when the Fed’s “Quantitative Easing” finally ended.

What Trump fails to grasp is that growth requires an increased supply of labor and natural resource inputs shifted towards the more interest-sensitive, earlier stages of production, not just increased demand for such inputs at these earlier stages via low-interest rate credit financing. Voluntary restraint of present consumption—that is, thrift—is what makes possible sustainable shifts of inputs from later to earlier stages of production. Thrift boosts productivity by furnishing more time for transforming inputs into outputs.

It is a blunder to think that mere financing without thrift, as is the case with bank credit expansions fueled by money creation, grows the supply of capital goods. Instead, boosting demand for inputs without higher supplies of inputs at the earlier stages merely makes capital goods more expensive relative to non-durable consumer goods. Money-creation drives prices upwards, inhibits thrift, and promotes boom sector waste, not growth.

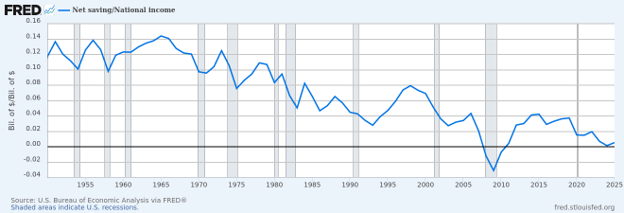

Thrift-financed investment is precisely what has been vanishing from the American economy, which explains why otherwise-sensible Republican attempts to stimulate growth by cutting taxes and regulations routinely fail. Since the mid-1960s, the fraction of income devoted to net savings has declined from double digit percentages to nearly 0 percent today (figure 1), the combined effect of soaring deficits and thrift-deterrence by escalating promises of future Social Security/Medicare benefits. I’ve been warning about this trend since the 1990s, a decade when Trump began plundering multiple failing businesses and was partying with Jeffrey Epstein (a “terrific guy” according to Trump back then) while conning the public into believing that he was a brilliant businessman and negotiator. Decades later, nothing seems to have changed.

Figure 1: Net Savings as fraction of National Income

Source: BEA via FRED®

Ordinarily, my rock-bottom expectations of politicians inhibits me from emphasizing any particular politician’s personal shortcomings, but Trump’s nutty declarations cross a red line. Sure, Trump says outrageous things just to trigger opponents, but please don’t look past these stark examples of Trump’s intellectual malfeasance. We urgently need to grow America’s economy, starting with bending the curve in figure 1. Anyone still an enabler of this ignorant, corrupt con-man after he expresses such a twisted, fact-evading “love” is part of the problem, not part of the solution.

Call me a deranged grandstander if you must; there is still no denying the well-known rule of American politics that brought victory to Trump in 2024: “It’s the economy, stupid.”