The posse of fools in the Eccles Building is so petrified of a stock market hissy fit that it has more or less created a Wall Street doomsday machine.

After trolling on the zero bound for 89 straight months now, the FOMC falsely believes that it has levitated the U.S. economy to the cusp of full-employment via massive liquidity and wealth effects pumping.

As a consequence, it refuses to let the market have breathing room for even a modest correction, insisting that just a few more months of this monetary lunacy will permit a return to some semblance of normalcy.

But it never gets there. The truth is, this so-called recovery cycle is now visibly dying of old age and being crushed by the headwinds of global deflation. Rather than acknowledge that the jig is up, our feckless monetary politburo just equivocates, procrastinates and prevaricates about the monumental policy failure it has superintended.

So the casino punters just won’t go home. They hang around against all odds, failing to liquidate and thereby enabling the robo machines to engage in endless and pointless cycling between chart points. As shown in the graph below, this has been going on for nearly 600 days now.

But of late the churning has been occurring in an increasingly narrow channel. Accordingly, the spring is being coiled ever more tightly.

When this 83-month long simulacrum of a economic recovery finally rolls over into recession someday soon, therefore, the implosion will be thunderous. The robo-machines will chase the punters out the casino exits in an epic stampede of selling.

Indeed, given the headwinds emanating from all corners of the global economy and financial system it is hard to believe that any sentient carbon units actually participated in today’s 19th nervous short squeeze in as many weeks. Among other things, first quarter results have been fully posted and it turns out that the S&P 500 companies earned $87 per share during the last 12 months (LTM).

That’s down from the $99 per share LTM figure posted in Q1 last year and the peak of $106 per share recorded in the year ended in September 2014.

In short, reported GAAP earnings — the honest kind companies report to the SEC on penalty of jail — are now down 18% from their recent bubble cycle peak. But since the S&P 500 has remained within 3% of its May 2015 all-time high (2130), it means that the PE ratio has been rapidly inflating right into the teeth of falling profits and a rapidly cooling domestic and global economy.

We are in the waning days of the third bubble cycle of the 21st century, yet the casino is pricing current earnings as if recessions have been outlawed and that the long-term growth trend of earnings is in double digits..

So here’s a spoiler alert. When S&P 500 earnings peaked prior to the financial crisis in the June 2007 LTM period, they clocked in at $85 per share.

The arithmetic of the matter, therefore, is that corporate earnings have grown at a miniscule 0.2% annual rate during the last nine years. Take the inflation out of that and adjust for nearly $3 trillion of stock buybacks and shrinkage of the share count in the interim, and you have less than no growth at all.

The worse thing is that we have been here before — at this same juncture exactly eight years ago in May 2008. The just completed earnings season had generated S&P profits of about $61 per share. That was down more than 25% from the prior year peak of $85, but the casino punters ignored the warning signs. The S&P 500 index remained within 3% of its November 2007 high (1570) for a few more months.

Then the sky fell. Nine months later the market was down by 57% and the U.S. economy was in the worst recession since the 1930s.

More crucially, the sell-side assurance that the severe earnings decline then underway was just the “pause that refreshes” and that profits would rebound to $100 per share in no time, proved to be dead wrong.

By the following spring, LTM profits for the S&P 500 companies posted at just $7 per share!

Now, we have no idea how far earnings will fall this time, but we do note that on the eve of the cyclical contraction in May 2008, the S&P 500 was trading at the same drastically inflated multiple as today — 24X LTM earnings.

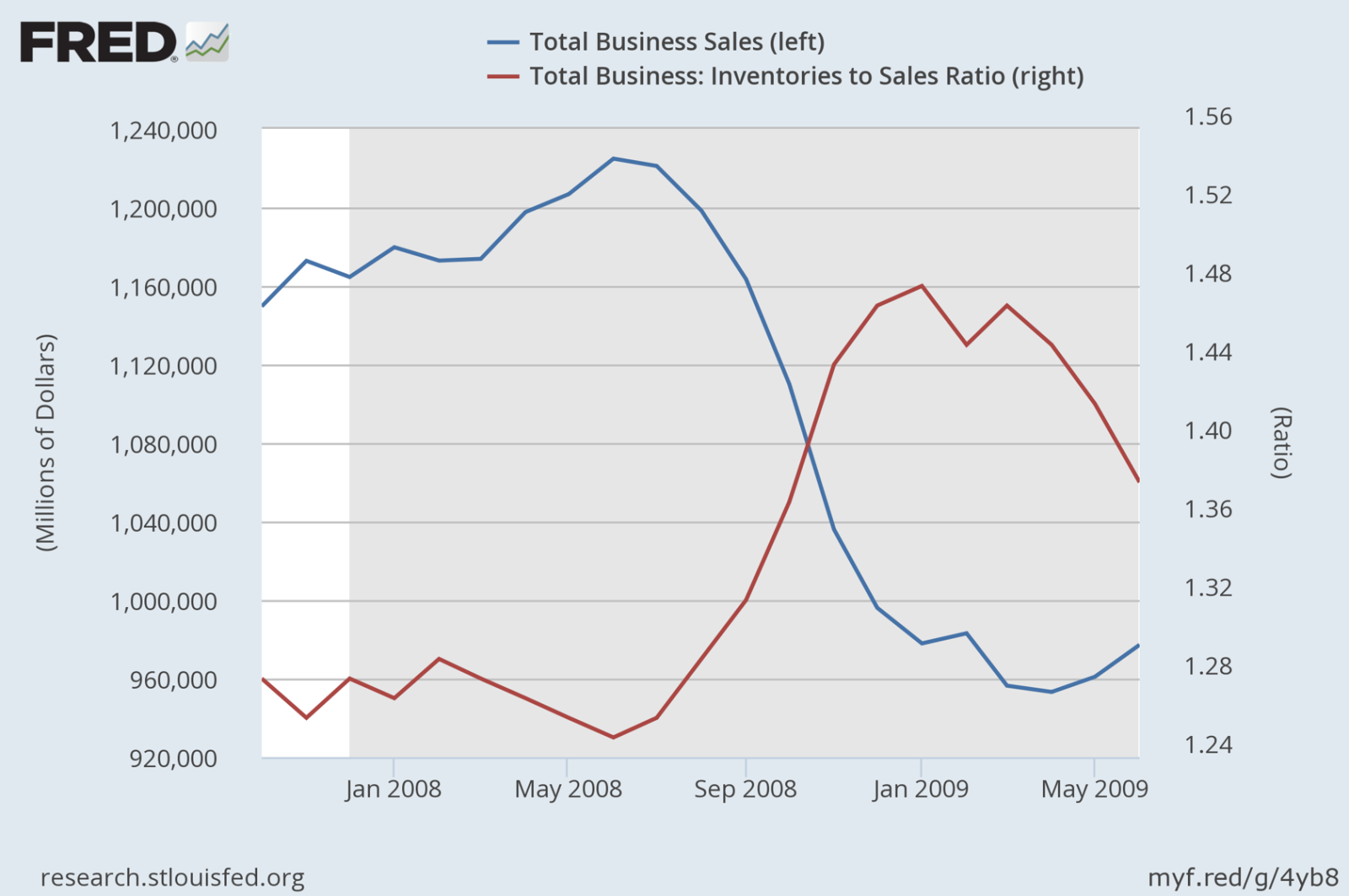

We also note that recessions are precipitated not by lagging indicators such as the dubious BLS monthly jobs surveys, but by the accumulation of excess inventories in the face of weakening sales. Here is what happened last time the punters insisted on staying in the nosebleed section of the casino when earnings were already falling rapidly.

Nor is this time any different. As of March, total business sales in the U.S. economy — manufacturing, wholesale and retail — were down 5.5% from their July 2014 peak, while the inventory ratio has soared back up into the recession zone.

That’s right. The scarlet “X” is back.

It means not merely that recession is just around the corner. That eventuality is guaranteed by the fact that this tepid recovery is already very long in the tooth by historical standards and by the reality that global trade, industrial production and PMI’s are slipping into recession mode virtually everywhere.

What is also proves is that the Fed and other central banks have absolutely destroyed the last semblance of honest price discovery. How is any other conclusion possible?

That is, with headwinds ranging from the tottering Red Ponzi of China, to the collapse in Brazil, the depression in the Baaken and Texas shale patch, the plunge in Japan’s trade accounts, the swirling liquidity crisis in the petro-states, the slump in German exports, the double digit decline of US freight volumes, the flat-lining of temp agency employment levels and much more, why would any rational investor pay 23.9X for the S&P 500 at this juncture—–and especially after nine years of no earnings growth?

Alas, they wouldn’t.

Wall Street has indeed become a doomsday machine and the Fed has zero chance of stopping its eventual implosion.

So in the interim the posse of monetary cranks in the Eccles Building ought to just stop their dangerous charade; it’s only feeding the robo-machines and putting everyone else deeper into harms’ way.

This article first appeared at David Stockman’s Contra Corner.