A new CPI inflation report will be released tomorrow. But we won’t have to wait for that to witness the growing chorus of pundits and politicians who are already declaring that price inflation doesn’t matter anymore, and the Federal Reserve must start a new round of monetary inflation and low-interest-rate policy.

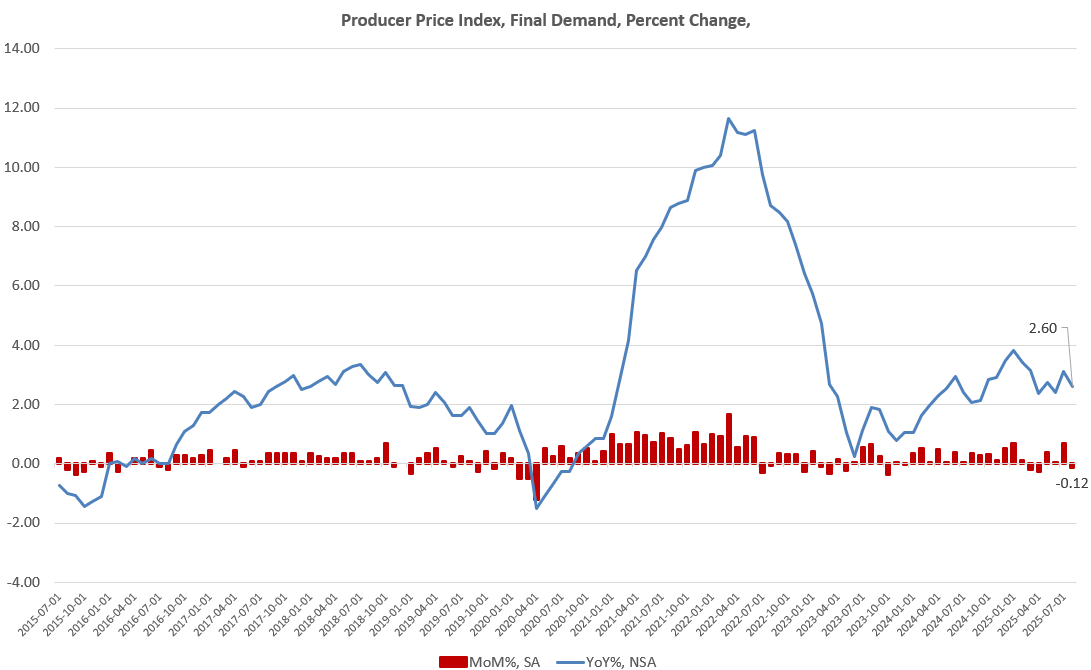

For example, the BLS released its latest Producer Price Index (PPI) report today, and prices ticked down slightly, falling by 0.1 percent, month over month. (PPI rose by 2.6 percent, year over year.) The report suggests some moderation in pries, but is hardly a sign of deflation.

Yet, the predictable response from the usual Wall Street “experts” was to use the PPI report’s lack of sizable price inflation to demand that the central bank quickly enact a large cut to the target policy interest rate. Why, well as Jeff Cox at NBC puts it: “The release provides breathing room for the Federal Reserve to approve an interest rate cut at its meeting next week.” This “breathing room” is purely political, of course. Pressure on the central bank to enact more monetary inflation has grown in recent weeks as the Trump administration has repeatedly demanded more easy money in order to provide additional short-term economic stimulus. The administration also wants lower interest rates so the federal government can borrow more money at lower costs as federal deficits continue to spiral upward under Trump.

Seizing upon this political “breathing room” Trump himself posted on Truth Social, ridiculously claiming there is “no inflation” but demanding a lower target rate from the Fed: “Just out: No Inflation!!! “Too Late” must lower the RATE, BIG, right now. Powell is a total disaster, who doesn’t have a clue!!!”

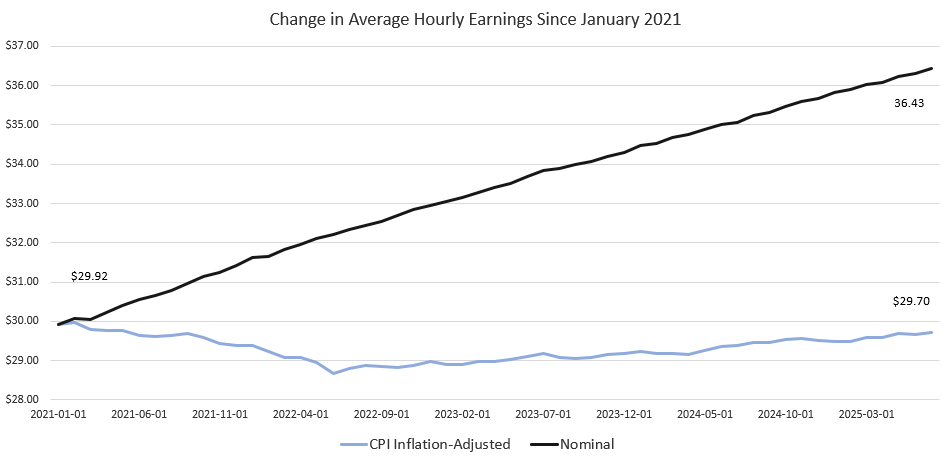

While it’s easy to see why a fabulously wealthy man like Trump might think there is “no inflation”—and he therefore wants more monetary inflation to inflate asset prices for his wealthy Wall Street friends—the reality is something else. For example, since 2021, the average hourly wage has gone down, with the most recent CPI reading showing that real wages are not keeping up with the price inflation that continues to come in well above even the Fed’s arbitrary two-percent target.

Thanks to disastrous asset-price inflation—not properly accounted for in CPI—for-sale homes are historically unaffordable as monetary inflation means more dollars chasing more real estate.

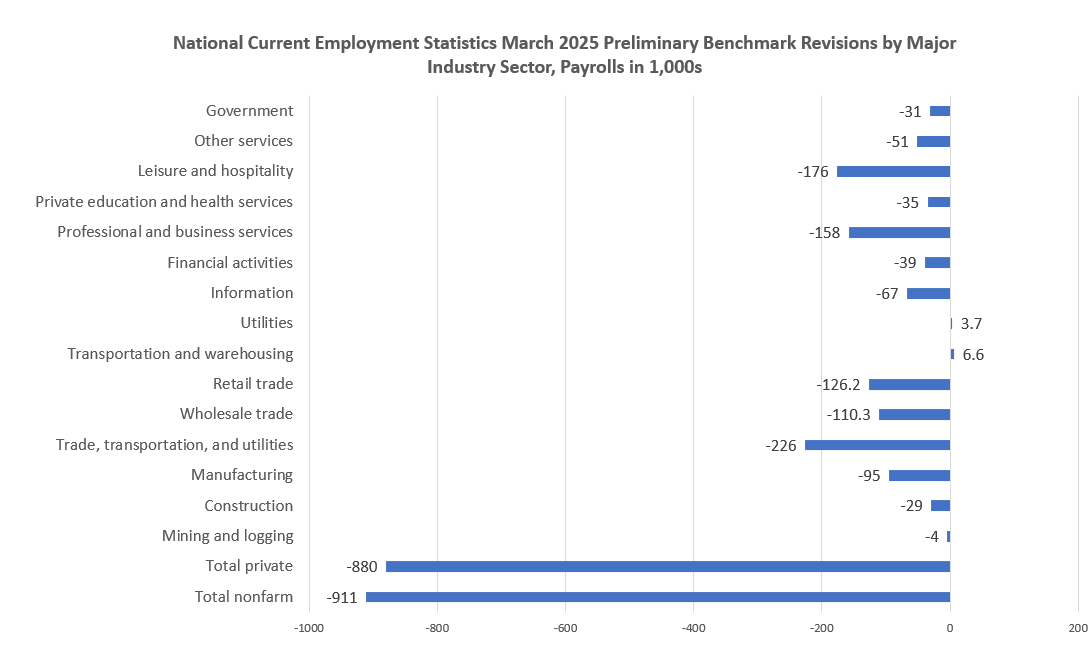

Pressure on the Fed for additional cuts to the target rate also come from yesterday’s revelation that the BLS was inflating job-growth numbers throughout 2024 and into early 2025. The BLS revised its total job creation for the year ending March 2025, lowering its estimate by more than 990,000 jobs, slicing total job creation by half for the period. In other words, the jobs economy during that period was significantly weaker than initially reported.

This has led to many calls for immediate and big cuts to the target interest rate by the Fed—perhaps even a jumbo cut of 50 basis points.

So, between some slight moderation in price growth, and the admission that job growth is much lower than previously reported, we can expect calls for a Fed rate cut to reach a fever pitch. The markets themselves appear to virtually certain that the Fed will cut the target rate at the FOMC meeting next week.

The problem with all this is the last thing ordinary people need right now yet another cut to the target rate—following last September’s premature, pre-election cut that has ensured continued price increases. A cut to the target interest rate means more monetary inflation as the Fed purchases more assets with newly created money. Even if the latest PPI and CPI data were to show a total lack of price growth, what is needed now is deflation so regular people can recover some of their lost earning power, and our bubble economy can finally revert to a normal economy built market demand rather than credit expansion. As I wrote last week:

Unfortunately, we are unlikely to see much actual deflation, although it is badly needed. Only deflation can return to consumers some of the purchasing power they lost during the covid panic and the resulting 40-year highs in CPI inflation that appeared during 2022. Deflation would also help to unravel 20-plus years of easy-money fueled malinvestment and financial bubbles. Were this to occur, the economy would then be rebuilt along more sustainable lines that conform to actual market demand, in contrast to the easy-money economy of speculative manias that enriches wealthy asset-holders at the expense of ordinary people.

It’s this last point that suggests to us what the central bank will do as employment data worsens and deflationary pressures emerge: the central bank will intervene on the side of wealthy asset owners to ensure that no sizable deflation in asset prices occurs, ensuring that consumers continue to see an evaporation of purchasing power even as their job prospects disappear. We’ll start to hear a lot in the media about how the Fed is working to increase inflation in order to get it back up to the “two-percent targe” to combat “deflationary” pressures—as if deflation were a bad thing.

This is the opposite of what the central bank should do, which is to refrain from any further intervention in the economy. The Fed should stop buying assets of any kind, and allow interest rates to be set by the marketplace instead of by central planners at the Treasury and at the Fed. As a result, asset prices would fall substantially, and the prices would rapidly become more affordable. It would also become possible again for ordinary people to earn a decent amount of interest on ordinary savings as interest rates gradually rose. In other words, the economy would—for the first time in decades—begin to swing back in favor or ordinary savers, young workers, and first-time home buyers.