Earlier this month, price growth as measured by both the official federal CPI and the PPI showed that price growth is accelerating in the US. For example, year-over year price growth for May, as measured by the CPI. was at 4.2 percent, an increase over April’s print of 3.8 percent. That was the the highest in 38 months. Meanwhile, for May, core CPI growth, year-over-year, hit a nine month high. In both core and non-core, month to month CPI growth remains firmly within positive territory. PPI growth was even more substantial, rising to 6.5 percent, year over year. That was the highest growth rate in 42 months.

Thanks to rising prices, real wages are falling.

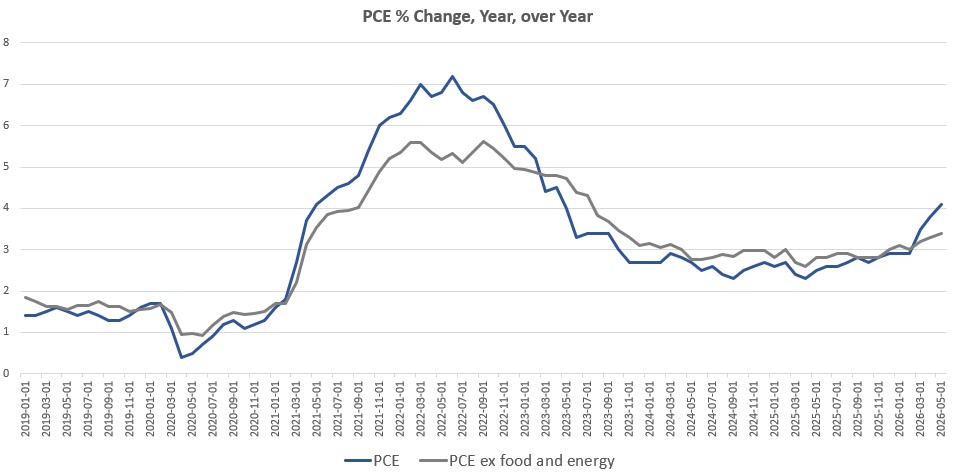

The Fed’s preferred measure for price inflation, however, is personal consumption expenditure (PCE) which is not released at the same time as the CPI or the PPI. PCE is the metric to which the Federal Reserve connects its arbitrary target of two percent for year-over-year price growth. Today, new PCE numbers for May were released and we continue to find that PCE is rising. Specifically, for May, 12-month PCE growth was 4.1 percent, a three-year (36-month) high. And for core PCE, the 12-month growth rate was up to 3.4 percent, a 32-month high.

This comes in spite of nearly two years of the Federal Reserve insisting that price inflation is rapidly returning to the Fed’s target level of two percent. Moreover, the Fed is trying to pin the Fed’s lack of progress on upward price pressure in the energy sector, thanks, in part, to the US-Israel war on Iran. This is the typical strategy of the Fed which, in recent years, has tried to pin historic levels of price inflation—reaching 40-yrear highs in 2022—any anything other than the Fed’s relentless monetary inflation.

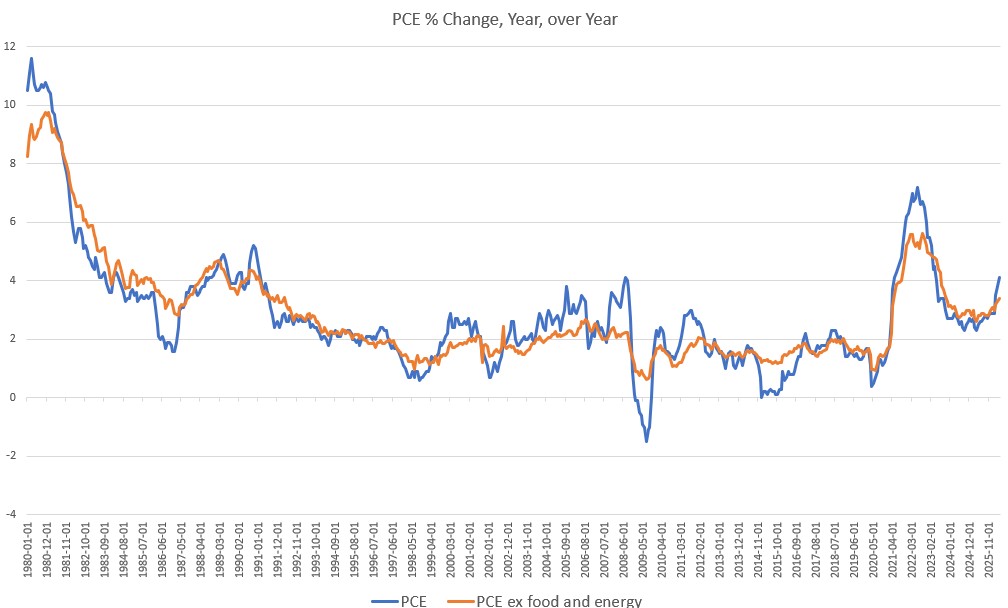

Yet, even in core PCE, with energy prices removed, we see that the PCE measure was headed up fairly consistently since late 2024. Indeed, if we take a broad view of recent decades, we find that the PCE (both core and non-core) is now higher than it was at the peak of the the housing bubble in 2006 and 2007. At that time, PCE reached four percent, still less than May’s measure of 4.1 percent.

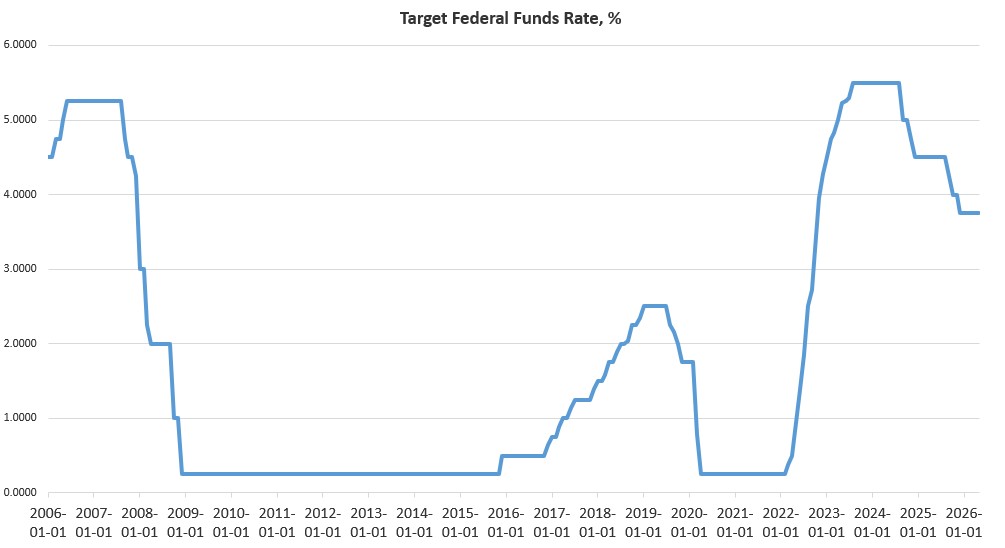

This further illustrates what I’ve pointed out since Warsh became the new chair of the Fed: his talk of big plans for reform at the Fed—and for carrying out Trump’s preferred policy of ever-lower interest rates—are politically constrained by the fact that price inflation continues to rise. The rising prices, of course, are playing out largely as we’d expect after the central bank has essentially printed more than five trillion dollars over the past six years. If anything, markets now increasingly expect an increase in the Fed’s target policy interest rate. This option may be soon forced on the Fed if it tries to avoid the political fallout of price inflation. 2026 is an election year, of course, and voters are know to respond unenthusiastically to rising energy and grocery prices.

On the other hand. Warsh could easily manufacture a reason to further force down interest rates if there is an obvious recession complete with imploding job markets. Then we’ll see endless calls for emergency measures to force down interest rates by any means deemed necessary. Of course, the administration doesn’t want a recession either since that comes with its own type of political damage for the incumbent party.

In spite of the dangers of spurring further price increases through looser monetary policy, it’s likely that Warsh really, really wants to find some way to further reduce interest rates in the face of rising price inflation. This is the baked-in preference of any central bank because loose monetary policy—a policy which includes continued artificial downward pressure on interest rates—allows the national government to borrow more cheaply while also benefiting from the inflation tax. Federal deficit spending continues at or above Biden-era and covid-era spending levels in many cases, so the need to keep interest rates low for the benefit of the federal Treasury remains politically critical. The Fed’s continued enthusiasm for “helping” the treasury access cheap credit is how we got the rising prices we now face. It’s unlikely the Fed will depart from this trajectory any time soon.