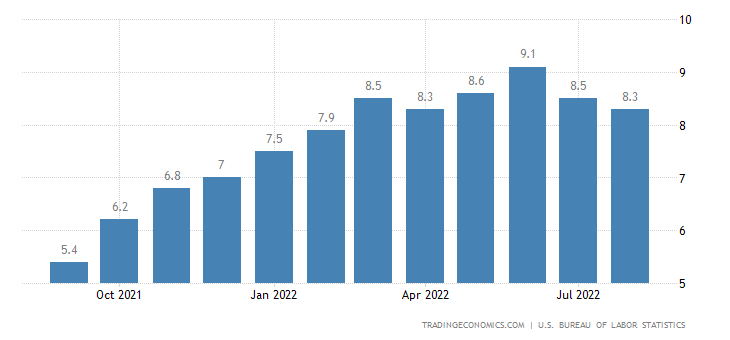

On September 21st, the Fed announced another 0.75 percent rate hike. The target is 3 percent to 3.25 percent. The annual rate of the CPI went down in July and in August, standing at 8.3 percent. If we consider the methodology used in the 1980’s, the CPI also went down in the last months, but it is still above 15 percent, according to Shadow Government Statistics.

This decrease in the CPI is due, partially, to the use of oil from the Strategic Petroleum Reserve and the fact that the monetary aggregates have stopped increasing. Since the Fed is no longer buying government bonds and mortgage-backed securities (MBSs), the monetary base (M0) and its balance sheet are not expanding. In fact, the balance sheet has been slightly contracting since April, and M0 follows the same pattern (chart 1). M1 and M2 also stopped increasing, with a slight contraction since March after a significant increase in 2020 in 2021.

Chart 1 – Fed’s Balance Sheet and M0

Fed’s Balance Sheet (Green); M0 (Red).

Source: St. Louis Fed.

This latest 0.75 percent rate hike took the IORB (Interest Rate on Reserve Balances), which is the main rate that the Fed uses to influence the FFR (Federal Funds Rate), from 2.4 percent to 3.15 percent.

Chart 2 – FFR, IOER and IORB

FFR (Red); IOER (Green); IORB (Orange).

Source: St. Louis Fed.

Jerome Powell stated in March that, if necessary (to contain the CPI), the FOMC would resort to hikes higher than 0.25 percent in future meetings. And, so far, this is what has happened.

As in Chart 1, by the end of July, the Fed’s balance sheet had barely shrunk (the Fed’s assets were down by less than 1 percent). And, between the peak reached on April 13 and September 21, it shrunk by “only” $148.7 billion. However, the Fed said it will continue to reduce its assets, as announced in May. It also stated that it is determined to bring the CPI back to the 2 percent target and it is committed to continue raising rates by 0.75 percent.

The peak of the FFR in the last rate hike cycle (2015-2018) was 2.4 percent. In December 2018, there was significant turbulence in the US stock market (and started cutting rates in 2019), and in September 2019 there was a crisis in the repurchase market and the Fed started to inject liquidity into it (doing QE and expanding its balance sheet). The FFR reached 2.4 percent again last July and now it stands at 3.15 percent. Does this mean the Fed can continue raising rates without consequences? Unlikely. In the last rate hike cycle, the Fed was not only raising rates, but also shrinking its balance sheet at a higher pace, which further limited the extent to which the Fed could raise rates (since the sale of assets held by the Fed made its prices go down and its interest go up). The Fed began to shrink its balance sheet in late 2017 (and went back to expanding it in September 2019). As for the FFR, the Fed started raising it in December 2015 (but went back to cutting it in H1 2019).

Real interest rates are still negative. Even if we consider the official CPI of 8.3 percent, the real rate is -5.15 percent. In addition, another important factor that that Fed needs to address in order to bring down the CPI is the money supply. In FY 2022, total government spending was $5.35 billion. The government is still spending money on COVID-related “stimulus”, Congress has passed yet another spending bill, and we have yet to see the impact of student debt forgiveness (as the government will have to borrow more to fund it). And let’s not forget that a higher IORB means that the Fed have to pay more interest on bank reserves, which means lower profits for the Fed, which means less of these profits will be given to the government, which means that the government will have a higher budget deficit if it doesn’t raise taxes, or it doesn’t cut spending.

All this means more indebtedness, that is, more bonds issued by the government that can eventually be purchased by the Fed (since, likely, there will not be enough demand for these bonds at the current FFR level, as expenses that the federal government is incurring with interest on debt are increasing). Even in a scenario in which the central bank does not raise rates, the increase in government indebtedness tends to increase interest expenses. But this is compounded when the central bank is raising rates. If the government continues down this path, the Fed will have to decide whether to continue to raise rates (which will increase the government’s interest expenses) and to shrink its balance sheet (which means that the Fed will be increasing the supply of bonds, further decreasing their prices and increasing their interest), or to give up on this plan and go back to cutting rates and increase its balance sheet to prevent the government from being unable to finance these expenditures. Historically, the second option is the one chosen by the Fed. It remains to be seen if the current scenario of a higher CPI will be enough for the Fed to break this tradition.

The US economy is not in a great shape and it is being questioned (here and here) whether the Fed will keep on its promise or if it will pivot.

GDP contracted 1.6 percent in Q1 and 0.6 percent in Q2, which constitutes a recession (two consecutive quarters of negative GDP), despite the fact that the government is trying to change this consensus to deny a recession. And the Atlanta Fed has lowered its Q3 GDP growth forecast to 0.3 percent (it’s still positive, but it’s common for the Atlanta Fed to lower its forecasts as new data comes in). However, it is true that, if we consider a more “official” definition of recession (from the National Bureau of Economic Research – NBER), the US was not in recession at the end of Q2. The NBER, in addition to considering the period of economic contraction that must take place to be considered a recession (more than a few months), considers the diffusion (the contraction must be spread across many sectors of the economy) and the depth of the contraction. And, from December 2021 to the end of Q2, all variables used by the NBER were positive.

Nonetheless, it is undeniable that the economy is contracting (or at least it is barely growing).

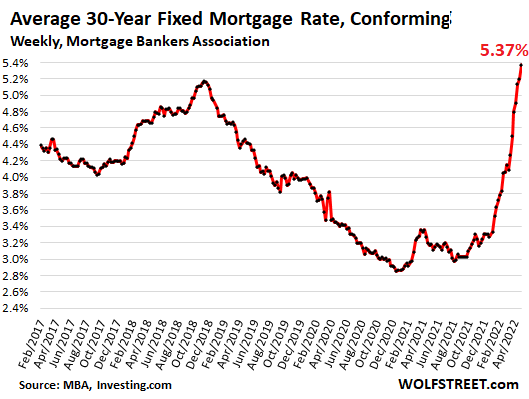

The housing market is contracting (although the Fed has not yet reduced its holdings of MBSs; the Fed has only reduced its holdings of government bonds and even slightly increased its holdings of MBSs – chart 3), as mortgage rates go up.

Chart 3 – Assets in the Fed’s Balance Sheet

Total Assets (Purple); MBSs (Red); Government Bonds (Green); Federal Agency Debt Securities (Orange*).

* It is not possible to see the line at this scale, because it is a figure of “only” US$ 2.3 billion.

Source: St. Louis Fed.

The CPI is outpacing wage raises, so real incomes are getting lower and consumer credit is going up.

Some yield curves are inverted. That is, the difference between the interest rates of bonds of longer maturity and bonds of shorter maturity is negative (usually they should be positive, since bonds of longer maturity must pay more interest as they are riskier than those of lower maturity). Historically, yield curve inversion is a leading indicator of recession (which usually occurs sometime between 6 and 24 months after the inversion). If bond investors expect a recession, they anticipate that the central bank will cut rates. This expectation causes long-term rates (10 or more years) to decrease in relation to those of shorter maturity, inverting the yield curve. Of course, this is not an accurate indicator and does not guarantee that there will be a recession.

Chart 4 – Yield Curves of US Government Bonds

30 Years-10 Years (Blue); 10 Years-5 Years (Orange); 10 Years-2 Years (Green), 10 Years-1 Year (Yellow).

Source: Trading View.

And stock indexes are trending down since last October:

Chart 5 – Stock Indexes

S&P 500 (Blue); Nasdaq (Orange); RUSSEL 2000 (Green); Dow Jones (Yellow).

Source: Trading View.

All these factors are indicators of a weakness in the US economy. The question remains: Will the Fed pivot?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}