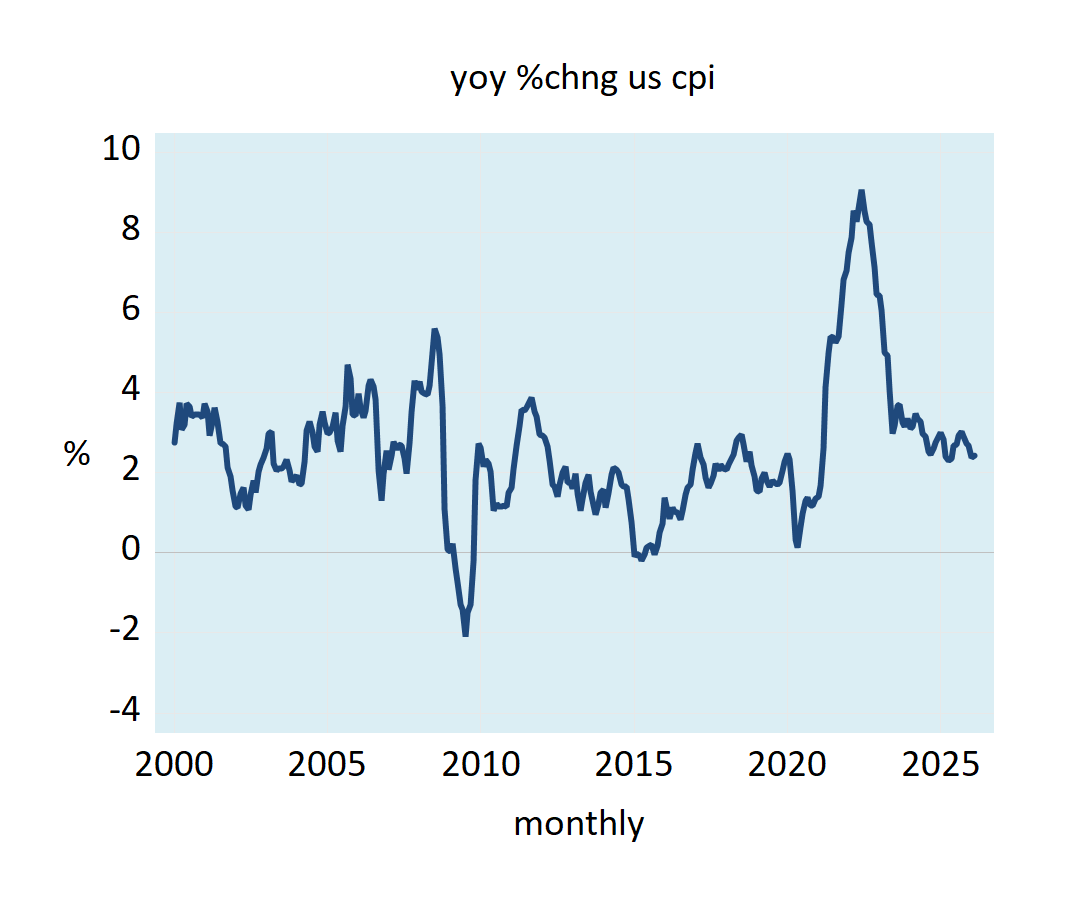

The yearly growth rate of the consumer price index (CPI) closed at 2.4 percent in February against a similar figure in January. In February 2025, the yearly growth rate stood at 2.8 percent. Note that, in June 2022, the yearly growth rate was 9.1 percent.

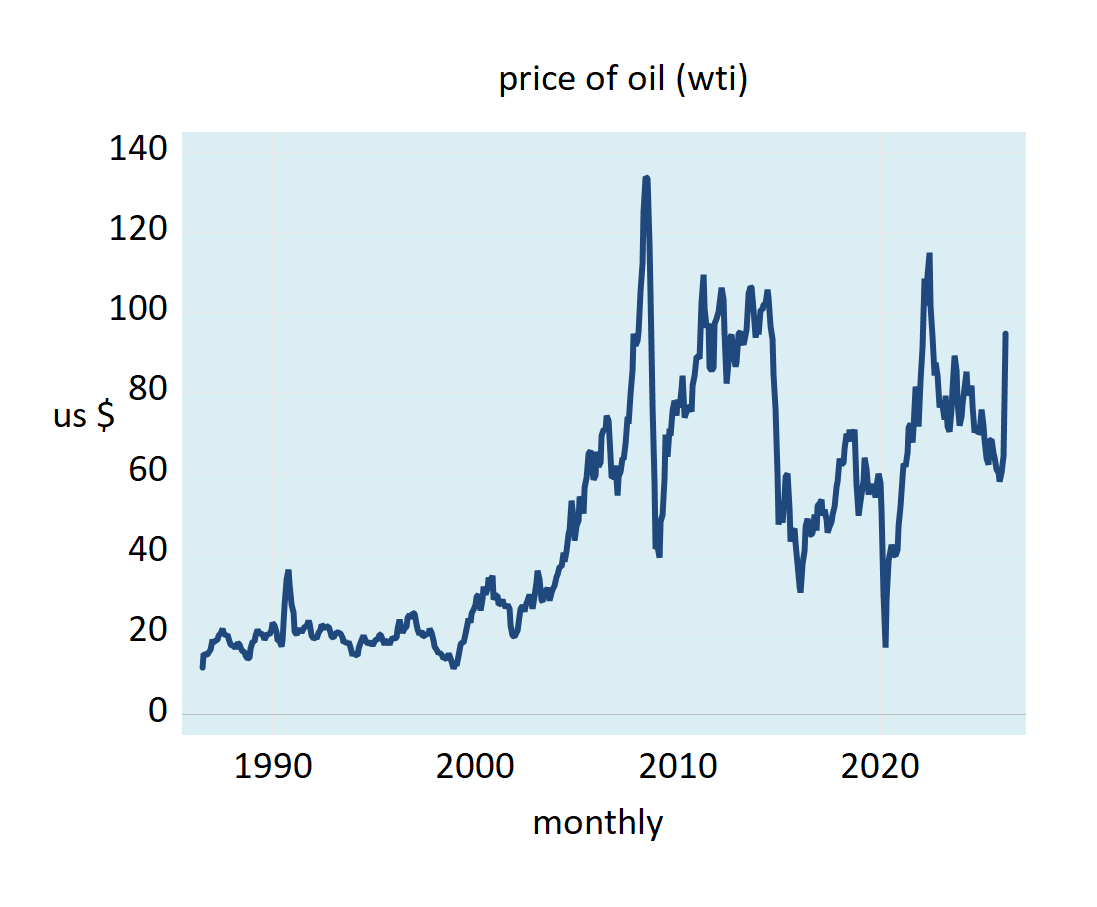

Most analysts are of the view that the sharp increase in the price of oil to around $95 per barrel (from around $64 at the end of February) is likely to lift the rate of inflation as depicted by the yearly growth rate in the CPI.

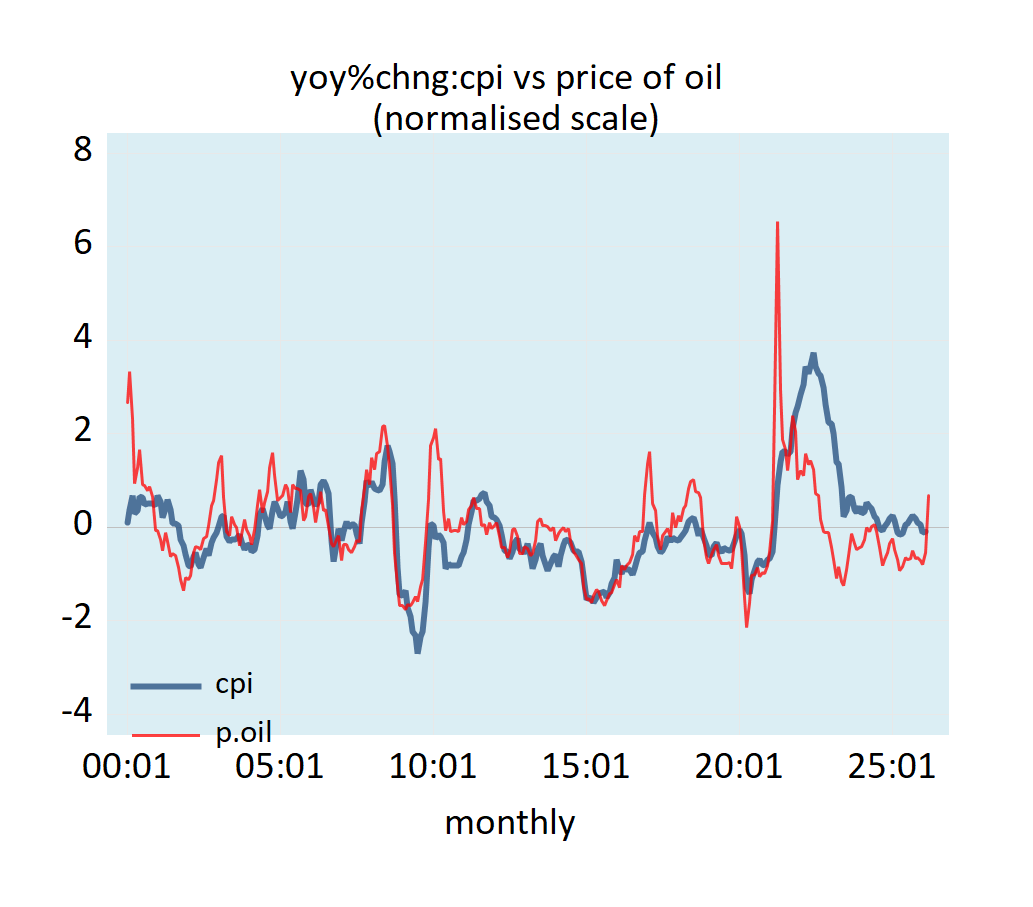

A very good visual correlation between the yearly percentage change in the consumer price index (CPI) and the yearly percentage change in the price of oil seems to provide support to the common idea that future changes in price inflation in the US are likely to be set by the yearly growth rate in the price of oil (see chart).

But, is it valid to suggest that the price of oil could be a key determinant of the prices of goods and services? Producers of goods and services set asking prices. It is also true that producers, while setting prices take into account various production costs, including the cost of energy. Whether the asking price offered by producers will be realized in the market place hinges on consumers’ acceptance or rejection of the asking price. Consumers dictate whether the price set by producers is “right.” On this Mises wrote,

The consumers patronize those shops in which they can buy what they want at the cheapest price. Their buying and their abstention from buying decides who should own and run the plants and the farms. They determine precisely what should be produced, in what quality, and in what quantities.

If consumers don’t have the money or do not value the goods at the prices asked by producers, then the prices asked will not be realized.

What is a price? It is the rate of exchange between goods established in a transaction. The price—or the rate of exchange of one good in terms of another—is the amount of the other good divided by the amount of the first good.

In a monetary economy, prices are usually the amount of money exchanged for other goods and services. A price is the sum of money paid for a unit of a good. If the stock of money rises while all other things remain intact obviously this must lead to more money being spent on the unchanged stock of goods—an uneven increase in prices of goods.

If the price of oil goes up, and if people continue to use the same amount of oil as before, then this means that people would now be forced to allocate more money for oil. If people’s money stock remains unchanged, then this means that less money is available for other goods and services, all other things being equal.

The overall money spent on goods does not necessarily change, only the composition of spending has altered here, with more on oil and less on other goods. Hence, the prices of goods or money per unit of goods remains unchanged. From this we can infer that the rate of increase in the prices of goods and services in general will be constrained by the growth rate of money supply, all other things being equal, and not by the growth rate of the price of oil. It is not possible for increases in the price of oil to set in motion a general increase in the prices of goods and services without corresponding support from money supply. Furthermore, the reliance on correlations to establish causality is likely to produce misleading results. All that correlation does is to describe, it doesn’t explain.

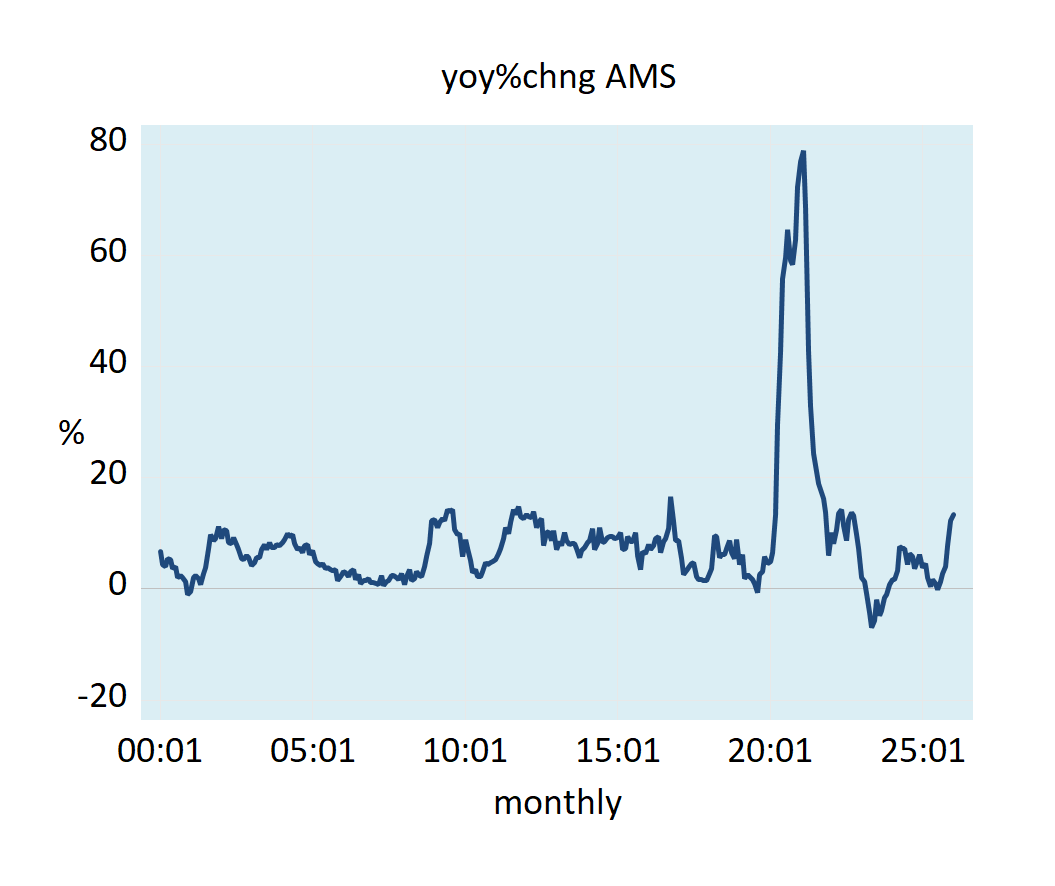

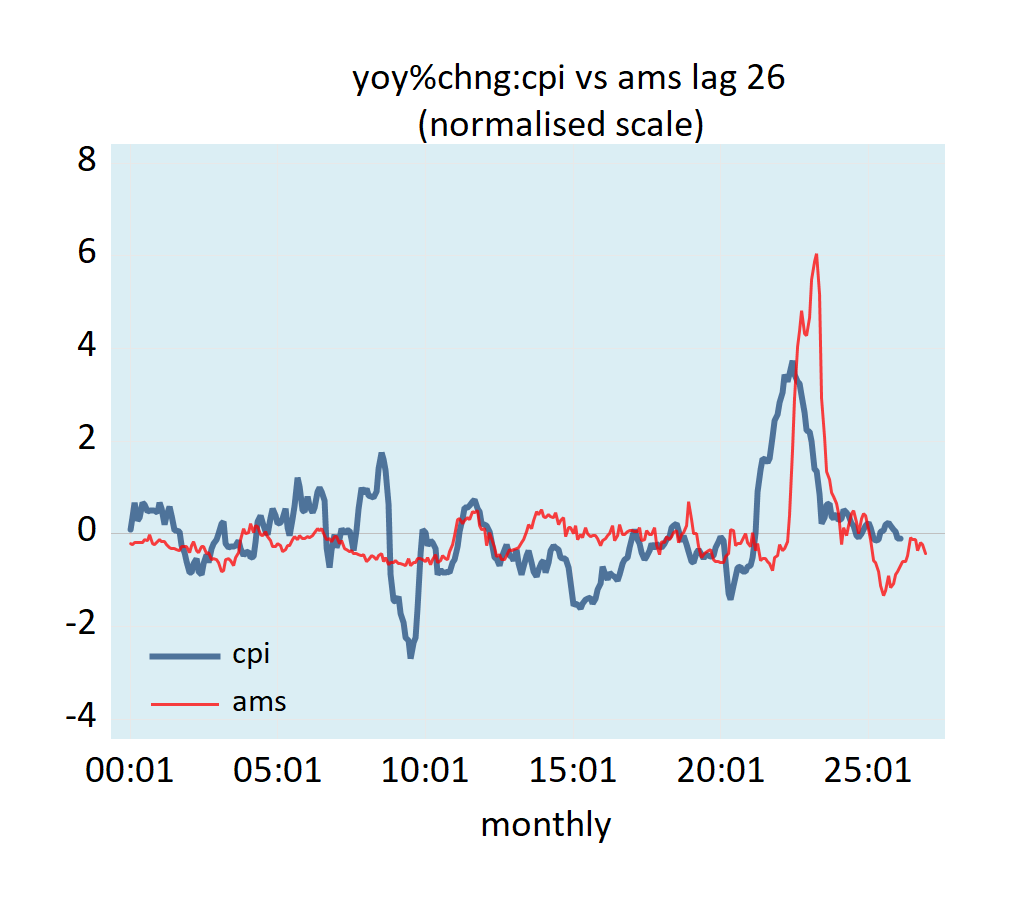

After rising to 79 percent in February 2021, the yearly growth rate of US money supply AMS followed a visible downtrend until mid-2023, before strengthening until mid-2024 before a renewed softening emerged. Given the long time lag from changes in money supply and its effect on the momentum of the CPI, the yearly growth rate in the CPI is likely to be strongly influenced by the lagged momentum of the AMS in the months ahead, which suggests may remain elevated in the short term before a softening emerges towards the end of the year. Note that changes in money supply do not affect prices instantly. When money is injected, it moves from one market to another market.

Notwithstanding the popular thinking that, by itself, an increase in the price of oil cannot cause general increase in the prices of goods and services, misleadingly labeled “inflation.” Without the increase in the growth rate of money supply, which is what inflation really is, no general increase in prices will occur.