Jean-Luc Mélenchon—the leader of the French far-left party “La France Insoumise”—wants to minimize concerns that the French government debt is very high at more than 100 percent of GDP. Such fears undermine his calls for higher government spending and chances to win the 2027 presidential elections. He has always looked enthusiastically for ways to lower public debt, even if only by accounting gimmicks. In 2020 as member of the French Parliament, Mr. Mélenchon called for canceling part of the French public debt held by the European Central Bank (ECB). In June 2026, after renewing his presidential bid, he also asked for measuring government debt against the economic value added over the lifetime of the debt stock, and not over one year GDP. By this new indicator, France’s public debt would magically shrink to around 12 - 13 percent of GDP.

Is the Measurement of Debt an Issue?

Following the Global Financial Crisis (GFC), COVID-19 pandemic, many years of sluggish growth, and persistent budget deficits, government debt has reached record high levels in many Western economies. According to the IMF Global Debt Monitor, public debt in Western Economies has more than doubled from about 45 percent of GDP in the 1960s to around 110 percent of GDP in 2024. Among them, the French public debt has been one of the fastest growing from less than 20 percent of GDP in the 1960s to 115 percent of GDP in 2025.

Yet, Mr. Mélenchon and his party supporters believe that the French public debt is not high, because it can be financed at relatively low interest rates. In addition, the debt is allegedly cushioned from a market sell-off by the importance of the French economy and systemic banks. Implicitly, Mr. Mélenchon admits that the ECB would most certainly jump to the rescue if needed, buy French bonds and lower interest rates. This is exactly what happened in the aftermath of the GFC when the ECB Governor Mario Draghi issued the famous “whatever it takes” commitment to save the euro and the ECB expanded its balance sheet by an astronomical EUR 5 trillion or 37.5 percent of GDP. In fact the French and euro area public debt are not financed cheaply because they are low, but because they benefit from central bank support and preferential treatment.

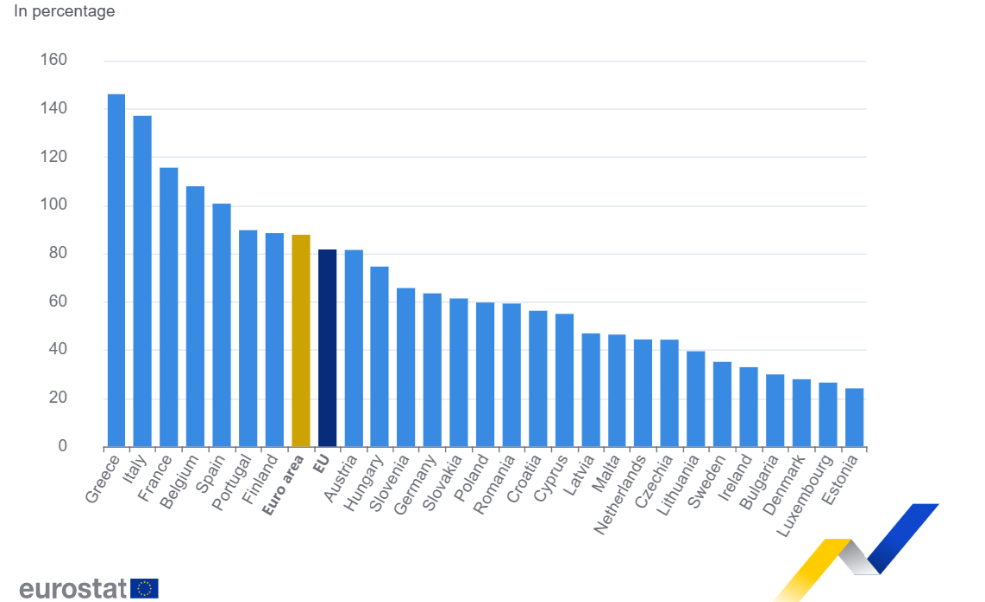

In order to avoid central bank monetization of government debt, which would be inflationary and politically divisive in a monetary union of sovereign states, the founding fathers of the euro came up with the Maastricht fiscal rules. Thereunder, member states are required to limit budget deficits below 3 percent of GDP and keep government debt below 60 percent of GDP1, or gradually reduce it toward that level. At 115 percent of GDP, the French public debt is almost double the benchmark, and France has gradually become the 3rd most indebted country in the euro area after Greece and Italy (Graph 1). Tinkering around with the definition of public debt would most likely be welcome by other highly indebted countries too and unleash a race to the bottom. Already Germany has abandoned its more frugal fiscal stance triggering a spending spree in defense and public investment in order to prop up its ailed economy.

Graph 1: General government gross debt to GDP (2025)

Source: Eurostat (link: Government debt at 87.8 percent of GDP in euro area - Euro indicators - Eurostat)

Mr. Mélenchon contends that measuring government debt (a stock variable) to GDP (a flow variable) is misleading. We disagree because measuring indebtedness relative to the debtor’s capacity to repay debt is a well-established indicator also in the private sector. Private debt stock is compared with a company’s earnings (EBITDA) during a given year too. The public debt indicator is actually more generous because, unlike with company earnings, only a relatively small part of GDP could be set aside to repay debt. It would be more telling to compare the stock of debt with the revenues that a government can extract in one year (usually only about 30 percent to 40 percent of GDP) and are not earmarked for compulsory spending items.

Most important, government debt already benefits from a preferential treatment relative to private debt. While businesses are required to generate enough profits to service and repay debt, governments are in general not expected to pay back their debt, but only to maintain a sustainable debt burden relative to the size of the economy and fiscal capacity. That is why economic growth, budget deficits and tax burden play a key role in assessing public debt solvency. There are also regulatory advantages such as very low or zero capital risk weights for bank investments in government bonds, minimum requirements for certain investment institutions like pension funds to hold government bonds and the use by central banks of government debt as collateral for monetary operations.

It is true that governments can mobilize revenues easier than companies, as they can resort to coercive non-market means such as, raising taxes and inflating away part of the debt in national currency. But, this ability is not unlimited and, the government extraction of resources from the private sector undermines growth and can easily lead the economy into a downward spiral.

Does Too Much Government Debt Stifle Growth?

In the aftermath of the GFC, Reinhart and Rogoff analyzed the impact of government debt on growth based on the experience of forty four countries spanning over two centuries. Their results famously showed that very high debt above 90 percent of GDP is associated with lower median growth rates, by one percent or more, similarly across emerging markets and advanced economies. High government debt increases risk premia and interest costs, crowding out private investment. It also raises fiscal uncertainty and expectations of tax increases, causing businesses to delay investment, hampering entrepreneurship and changing consumption patterns. In addition, the risk of debt crises is non-trivial, in particular when the fiscal burden is already too high and spending cuts are unpopular.

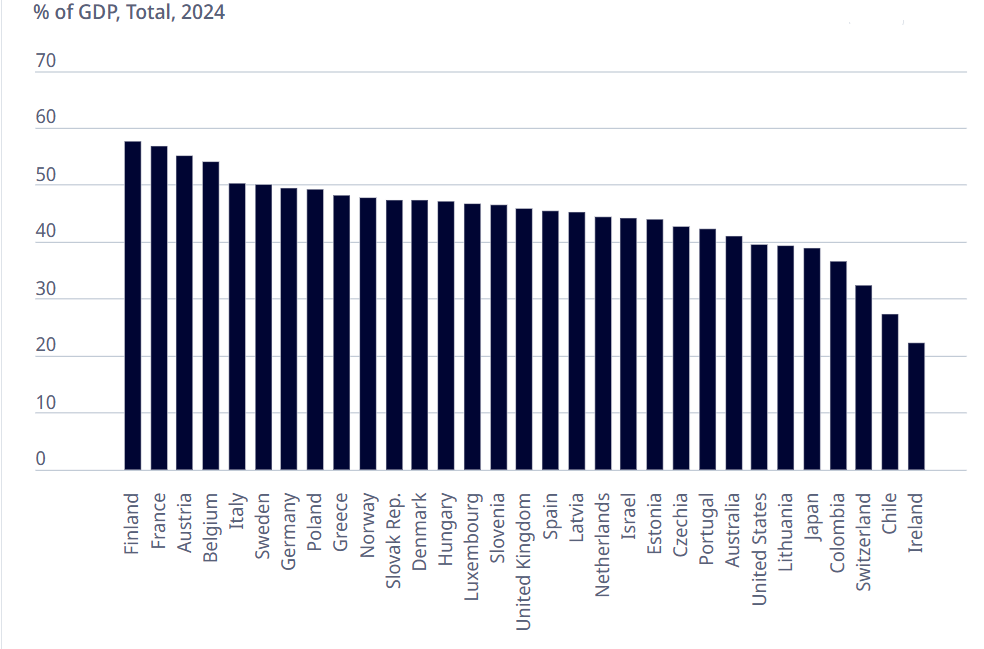

Gwartney, Holcombe and Lawson have argued that not only high debt, but also oversized government spending depresses economic dynamism. As general government spending in OECD countries has almost doubled from 1960 to 1996, their real GDP growth rates fell by almost two thirds on average. At about 44 percent of GDP, the tax burden in France is the second highest among OECD countries, almost 10 percentage points above the average. It is doubtful that taxes can be increased further without a severe economic backlash. This is coupled with a similarly very high level of public spending approaching 57 percent of GDP (Graph 2) and suggesting that the marginal return of the additional public spending planned by Mr. Mélenchon should be very low.

Graph 2: General government spending

Source: OECD ( link : General government spending | OECD )

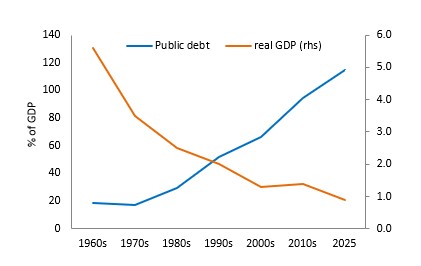

Over the past three years, the budget deficit stood at around 5 percent of GDP. France has not had a balanced budget in more than 50 years, i.e. since 1974, and budget deficits exceeded the 3 percent of GDP ceiling under the Maastricht rules in 26 years out of 34 since 1992. As a result public debt skyrocketed from less than 20 percent of GDP in the 1970s to roughly 115 percent of GDP today. This reflects also the effect of increasingly lower economic growth as government intervention stifled more and more the private sector and economic growth (Graph 3).

Graph 3: Government debt and real growth in France

Source: Own calculations with data from IMF (2025 Global Debt Monitor.pdf) and FRED (National Accounts: GDP by Expenditure: Constant Prices: Gross Domestic Product: Total for France (FRAGDPRQPSMEI) | FRED | St. Louis Fed)

A recent report of the French Court of Accounts sounded again the alarm bell over the unsustainable fiscal developments and their bleak outlook. Without additional fiscal consolidation measures, public debt is set to rise rapidly to reach 129.4 percent of GDP until 2031, while the budget deficit will be close to 6 percent of GDP. Due to rising interest rates, the annual cost of debt has also been growing rapidly from about 2 percent of GDP in 2024 to 2.5 percent of GDP in 2026, contradicting Mr. Mélenchon’s relaxed stance.

Mr. Mélenchon and his political partners in the alliance of left-wing parties “Nouveau Front Populaire” (NFP) ran in the 2024 elections with an economic program promoting more government intervention. They plan to lift annual public spending by a whooping 150 billion euros (about 5 percent of GDP) by increasing public and minimum wages, reversing Macron’s pension reform and raising other social spending. They also want to tax the economy more by introducing a tax on companies’ “super-profits,” restoring a wealth tax on the rich and increasing the progressivity of income and inheritance taxation.

Center-right critics and business groups doubt that the proposed tax measures could collect the projected amounts given France’s already oppressive tax burden. Therefore they expect the NFP program to increase budget deficits by 3 to 5 percent of GDP annually, placing government debt on an explosive trajectory. Regardless of how it is being measured, a high level of public debt is primarily a warning signal that government spending and intervention in the economy are already too high. Politicians like Mr. Mélenchon better pay attention to it or risk leaving the economy in permanent decline.

- 1

The “60% benchmark” was chosen primarily as a practical policy target to keep debt at a stable level over time, assuming a budget deficit of 3% of GDP and roughly 5% nominal GDP growth (2 - 3% real growth plus 2 - 3% inflation).