The Iran war and its consequences dominate the headlines in the press and financial media: oil and energy price shock, inflation, recessionary effect on the world economy, new potential for conflict between states. Above all, the uncertainty about what happens next is high: When can the final end of the war be expected? And how long will it take until the energy markets normalize?

However, one factor that is of absolutely central importance for investors is usually not discussed in detail: liquidity in the financial markets. What is meant by the word “liquidity”? Traders typically speak of high liquidity in the financial markets when everyone seeking money or credit can readily find sufficient supply: that is, when stocks, bonds, derivatives, and commodities can be exchanged for money without problems; and when banks and investors willingly and abundantly grant credit.

One can define the term liquidity more precisely: liquidity is high when large volumes of securities can be bought and sold at any time without triggering noticeable changes in market prices. Or, viewed differently: liquidity is high when the spreads between bid and ask prices for stocks, bonds, derivatives, and commodities are relatively narrow, and do not widen even with large transaction amounts, so that securities positions can be built up and reduced again in a short time without any substantial costs.

In financial markets, liquidity is usually not a constant. Rather, it is subject to changes. In fact, liquidity can decrease from one day to the next, and in extreme cases it can even dry up temporarily. An example of this was the financial and economic crisis of 2008/2009, in which there were moments when no selling prices could be obtained for various government, mortgage, and corporate bonds.

If liquidity in the markets dries up—because suddenly fewer investors appear on the buying and selling side, banks reduce their trading activities, etc.—price fluctuations increase. In other words, volatility goes up. Sellers may suffer unexpected (high) losses when they liquidate their positions, or securities become de facto economically unsellable.

Liquidity is of great importance for credit and bond markets, in fact, for the smooth functioning of today’s fiat money system, which is literally built on debt. The truth is: high liquidity is actually the lifeblood of the fiat money system. Because in the fiat money system, the indebtedness of the economies increases relentlessly over time. And the rising indebtedness is accompanied by a deterioration in the debt sustainability of the economy: debt burdens rise faster than incomes.

What is more, in the fiat money system, debtors not only continually expand their liabilities. Due debts are also replaced by new debts that (ideally) carry (still) lower interest rates—and so the debt burden remains (initially) bearable for the borrowers. Liquid markets are necessary to handle the refinancing of maturing debts smoothly and without problems. But not only borrowers appreciate high market liquidity for bonds and loans, the same holders for lenders.

Because it allows them to exit their engagements at any time quite easily, and without great costs (if, for example, fear of defaults grips them). Above all, however, high liquidity ensures that investors are willing to lend their money at relatively low interest rates. Just consider, currently, the 30-year French government bond carries a yield of 4.38 per cent per year. Would investors buy the bond at this yield if they could not sell it at any time during the remaining term, but had to hold it until final maturity? Probably not. So one sees high market liquidity lowers the interest costs for the debtor.

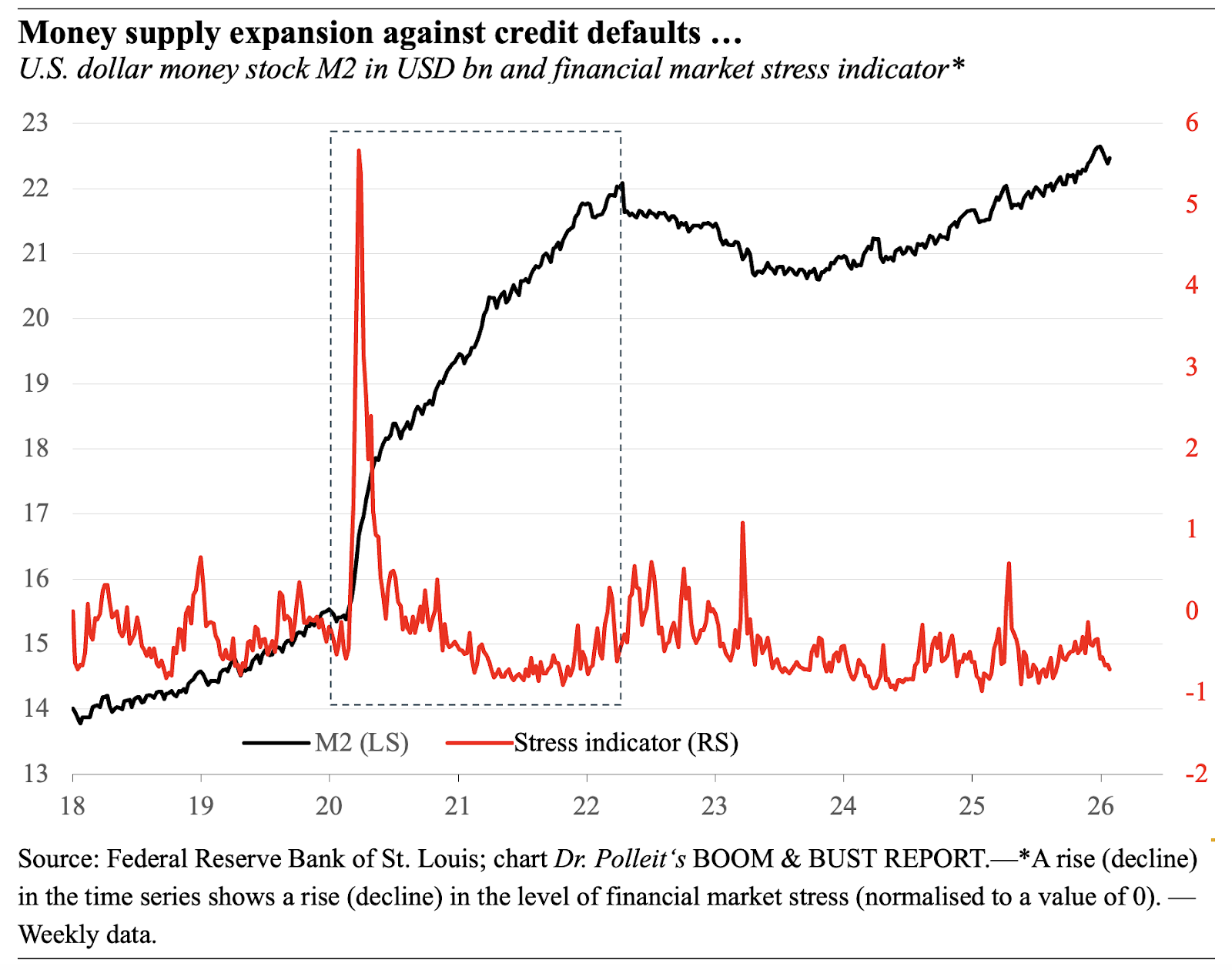

One can guess that a sudden drying up of liquidity in the credit markets throws the fiat money system into turmoil, and can even cause it to collapse. Just think of the politically-dictated lockdown crisis in spring 2020: The mega-recession associated with it caused credit default fears to skyrocket, liquidity in the credit market dried up, and a credit crisis was about to unfold. The collapse of the credit markets was only averted because the US Fed immediately announced to buy any kind of debt paper and pay for it with newly-created US dollars.

And, since all other major central banks followed the Fed, the credit default fears in the markets vanished: Investors quickly realized that they would be “saved”—that there would be no systemically-relevant defaults, let alone a liquidity shortfall in markets. Reassured, they returned to the market, willing to invest in bonds at artificially-suppressed interest rates, and with unusually-compressed credit spreads.

It is fair to assume that, to this very day, stock, bond, and housing prices benefit from the safety net that central banks have (in an almost invisible way) put under financial markets—i.e., from the artificial liquidity thereby created. From this insight we can conclude that, in the next crisis that hits the financial markets, the central banks will again open the money floodgates, very likely even more than ever before—because the debt levels have continued to rise in recent years, the dependence especially of the credit markets on support from the central banks has become even greater.

The figure above shows how the looming credit crisis in 2020/21 was “inflated away”: When the economy collapsed at the beginning of 2020 and credit default fears skyrocketed, the US central bank increased the money supply. The investor community immediately understood the message: here is the bail-out. The credit default fears subsided, market liquidity returned, the situation normalized. The money supply expansion remained, and the purchasing power of money was permanently reduced. In all likelihood, something very similar will happen in the next credit crisis.

With this consideration we make the case that artificial liquidity, as orchestrated by central banks, are a recipe for inflation shocks. In this sense, inflation, the devaluation of the purchasing power of money, remains one of the central challenges for savers and investor—inflation in the form of a gradual, step-by-step reduction of the purchasing power of money over time or in the form of a heavy, sudden devaluation in a short period of time, an “inflation shock”—as could be observed from 2020/2021, driven by the massive money supply expansion.