Further to Nicolai’s post on Steven Cheung: The “theory of the firm” in economics is usually dated back to Coase (1937), with important later contributions by Alchian and Demsetz (1972), Jensen and Meckling (1976), and later contributions from Oliver Williamson, Oliver Hart, and others. Management scholars might describe Schumpeter (1934) or Penrose (1959) as having distinct theories of the firm, though their contributions are perhaps better described as theories about what firms do, not what firms are. I would argue that Knight (1921) also offers a theory of the firm—Nicolai’s and my 2012 book Organizing Entrepreneurial Judgment is largely a riff on Knight. All this raises the question: what do economists and management scholars mean by “firm” anyway?

Classic economic theories of the firm

I wrote a short piece on this in 2012, inspired by a presentation by Demsetz at the ISNIE (now SIOE) conference in a session honoring Yoram Barzel on his 80th birthday (I took the photo below). Demsetz pointed out that Coase (1937) defines the firm in terms of the employment relation. A one-person operation, in this definition, is not a firm, and vertical integration deals with the question of adding producers of intermediate products to the firm’s employment roll. Demsetz thinks independent contractors are firms, and hence it makes little sense to speak of “firm” and “market” as alternatives, as Coase does. (Oliver Williamson, during an earlier session, noted that Coase expressed more interest in intermediate product markets in his 1988 article than in “The Nature of the Firm.”)

For Knight, Williamson, Hart, and Foss and Klein, in contrast, the firm is defined not by the employment relationship, but by the ownership of alienable assets. In this approach, the question is who owns what, not who is employed by whom. Of course, even in the Knightian approach, to get from the one-person firm to the multi-person firm requires some theory about the relative transaction costs of employment versus independent contracting, a theory Nicolai and I try to provide in chapter 8 of our 2012 book, focusing on the conditions under which the entrepreneur can delegate judgment to subordinates.

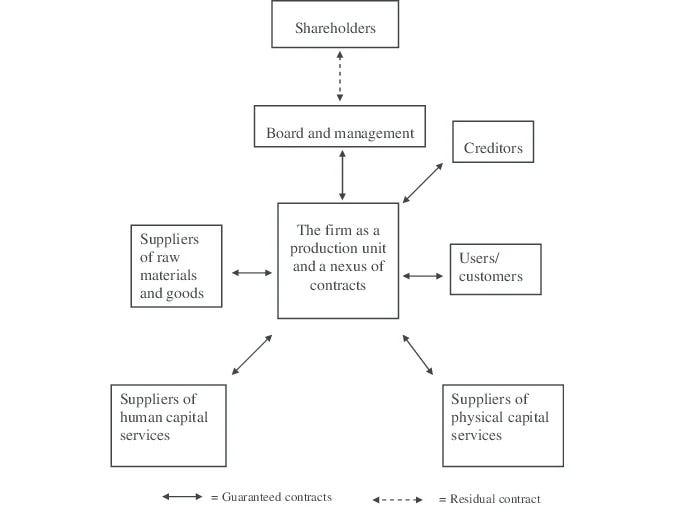

The firm as a nexus of contracts

Cheung, as Nicolai points out, holds a position closer to what we now call the nexus-of-contracts approach. For Alchian and Demsetz and (even more so) for Jensen and Meckling, the “firm” is a label we assign to a set of individuals creating joint value via team production. The team includes people legally classified as employees and owners, but also suppliers, distributers, and collaborators who are independent contractors or employees of other firms. (In a famous rhetorical flourish, Jensen and Meckling—ironically, the bêtes noires of many contemporary stakeholder theorists—write that “most organizations are simply legal fictions which serve as a nexus for a set of contracting relationships among individuals.”) In this approach, questions of firm boundaries—who is “inside” or “outside” the firm—are largely irrelevant. The interesting issues involve the nature of the relationships among team members, whatever the formal legal status of those relationships.

A feature of Alchian and Demsetz’s (1972) approach is that owners (as residual claimants) are simply part of the team, with no special status other than their role as monitors who identify and limit shirking on the part of other team members. One notable implication is that bosses don’t necessarily hire workers; workers may just as easily hire bosses. Recall Cheung’s (1983, p. 8) famous illustration: “My own favorite example is riverboat pulling in China before the communist regime, when a large group of workers marched along the shore towing a good-sized wooden boat. The unique interest of this example is that the collaborators actually agreed to the hiring of a monitor to whip them.” In Alchian and Demsetz’s example, the employee can “fire” his employer by quitting, just as I can “fire” my grocer by shopping at a different store.

Ownership, authority, and residual control

A problem with the nexus-of-contracts approach is that, as Nicolai and I have argued in various works, ownership is in fact a distinct economic function, the key element of which is not residual claims (which can be assigned to non-owners) but residual control. Ownership is the right to decide what to do in conditions not specified by prior agreement. Loosely speaking, ownership is not just another factor of production, but the “controlling factor” that designs and implements the procedures and practices—the organizational “rule of the game”—within which the other team members operate. The ownership function can also be exercised with greater or lesser capability or ownership competence. As Ludwig Lachmann (1956) put it, in the context of owners and hired managers, even those with substantial day-to-day decision rights: “We might . . . distinguish between the [owner] and the [manager]. The only significant difference between the two lies in that the specifying and modifying decisions of the manager presuppose and are consequent upon the decisions of the [owner]. If we like, we may say that the latter’s decisions are of a ‘higher order.’”

These ideas are rooted in Knight (1921) who foregrounds the idea of resource or asset ownership as the defining characteristic of a firm: the firm is defined as an entrepreneur plus the alienable assets she owns and controls. The entrepreneur may or may not have employees—the key is ownership, not the nature of the contractual relationship with other stakeholders. The Grossman and Hart property rights view comes out of this tradition as well.

Williamson also distinguishes sharply between employees and non-employees (or intra-firm and inter-firm transactions). He invokes the notion of “forbearance,” the idea that the law treats the firm itself as the arbiter of intra-firm disputes, while the courts are more likely to intervene in disputes between firms. (See the discussion in his 1991 article, especially pp. 98-100 of the version that appears in The Mechanisms of Governance.)

The firm as a reference point

Hart’s more recent work takes a different tack, treating the firm as a “reference point” for organizing interactions among stakeholders (see here and here). Drawing on concepts from behavioral economics, Hart argues that parties enter transactions with some notion of fairness, and renege on commitments or shirk on performance to the extent that they feel aggrieved, or shortchanged relative to this reference point. This explains why contracts are incomplete (a response to criticisms from Eric Maskin and Jean Tirole of the standard explanations for incompleteness)—incomplete contracts leave room for the ex post renegotiation that is needed as new circumstances arise. In other words, the contracts that constitute the firm are written not to specify future interactions, but to provide a general framework within which bargaining and negotiation can take place.

The bottom line

So, what is a firm? The answer probably depends on the problem one wants to solve. In other words, perhaps the better question is, What are the important research questions that can be answered when the firm is defined as X?