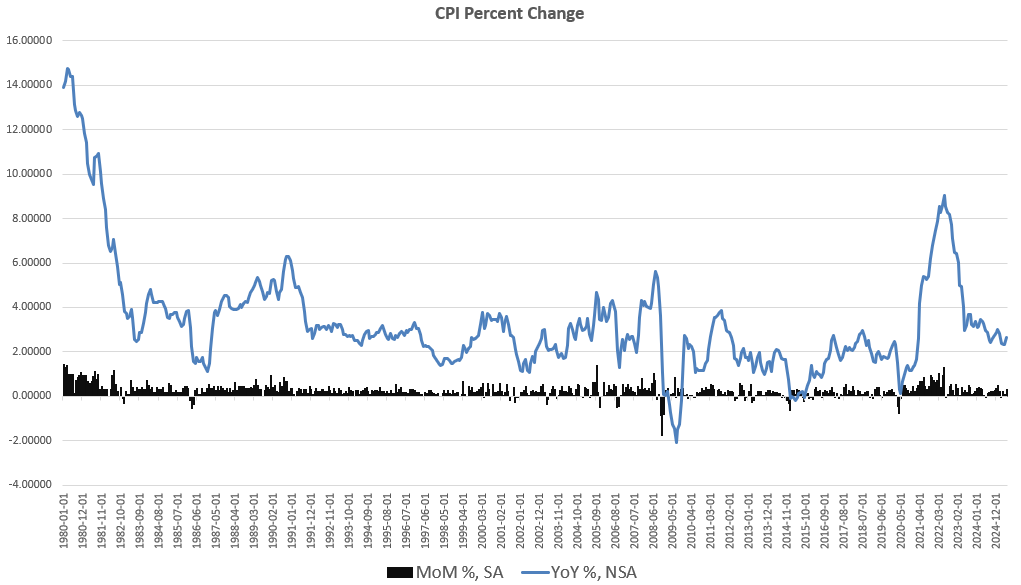

Earlier this month, we looked at June’s CPI numbers and found that, yet again, the government’s own price-inflation data shows prices continue to grow above the central bank’s two-percent inflation target. As I reported on July 15, June’s CPI growth rate was the largest year-over-year increase in four months, and the largest month-to-month increase since January 2025. June’s CPI increase also places CPI growth above of CPI growth rates experienced during September of last year. At that time, Fed Chairman Jerome Powell had declared that price inflation was rapidly moving back toward the Fed’s two-percent target. Nine months later, we can see the Fed’s forecasters were clearly wrong, as the CPI has increased by 2.1 percent in that period.

A similar trend also showed up in so-called “core CPI” which removes volatile food and energy prices. Core CPI also hit a four-month high in June, measured year-over year. Measured month-to-month, core CPI hit a five month high in June.

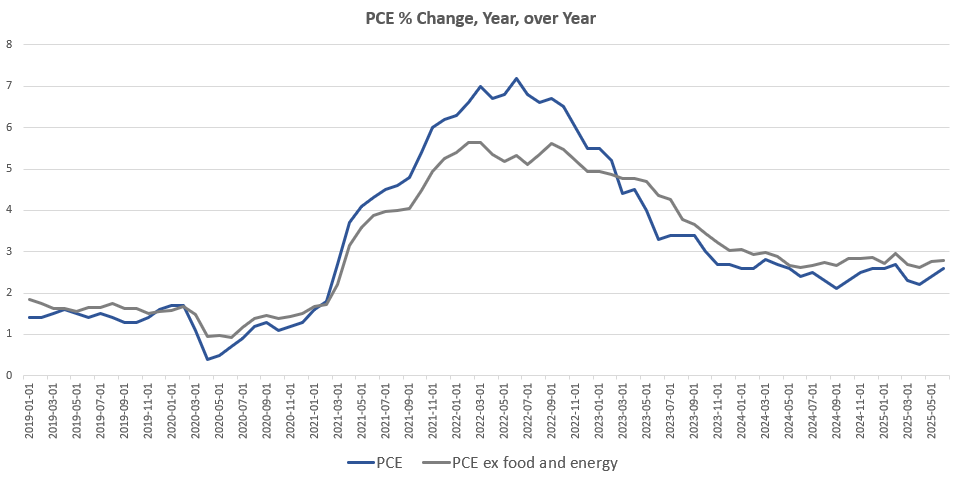

The Fed’s preferred measure of price-inflation, however, is the PCE (personal consumption expenditure) measure, and in a new data release Thursday morning, the BLS reports that PCE price inflation is heading upward, as well. In June, PCE increased by 0.3 percent, month over month, and that’s the largest monthly increase since February. In fact, the monthly PCE growth has gotten larger each month since February. The same is true of PCE excluding food and energy.

Looking at the PCE change, year over year, we find a similar trend. During June, PCE growth was up by 2.6 percent, year over year. That’s up from May’s growth rate of 2.4 percent, and June’s growth is the largest since February. PCE growth minus food and energy also came in at a four-month high, rising to 2.8 percent (or 2.79 percent), up from May’s measure of 2.75 percent. In spite of the Fed’s confident claims about price inflation falling to the two-percent target last fall, monthly PCE growth has changed little since April of 2024.

Of course, it is likely that the Fed never really believed that price inflation was decelerating at all. Rather, at that time, Powell and the Fed simply needed something to justify the Fed’s September cut to the policy interest rate. The Fed needed some way to explain away what was almost certainly a cynical effort to stimulate the economy for the benefit of the incumbent political party.

June’s troubling numbers on price inflation do help explain why Powell and the FOMC have been so reluctant to cut the policy interest rate yet again, in spite of repeated demands from the President. The FOMC again declined to lower the policy rate earlier this week at its July meeting. Powell is right to be concerned that a dovish turn from the Fed would fuel even more PCE inflation, and could also fuel rising yields in long-dated Treasurys.