Last week, the the Federal Reserve left unchanged its benchmark federal funds rate, with Fed Chairman Jerome Powell declaring the US economy to be “on a good path.”

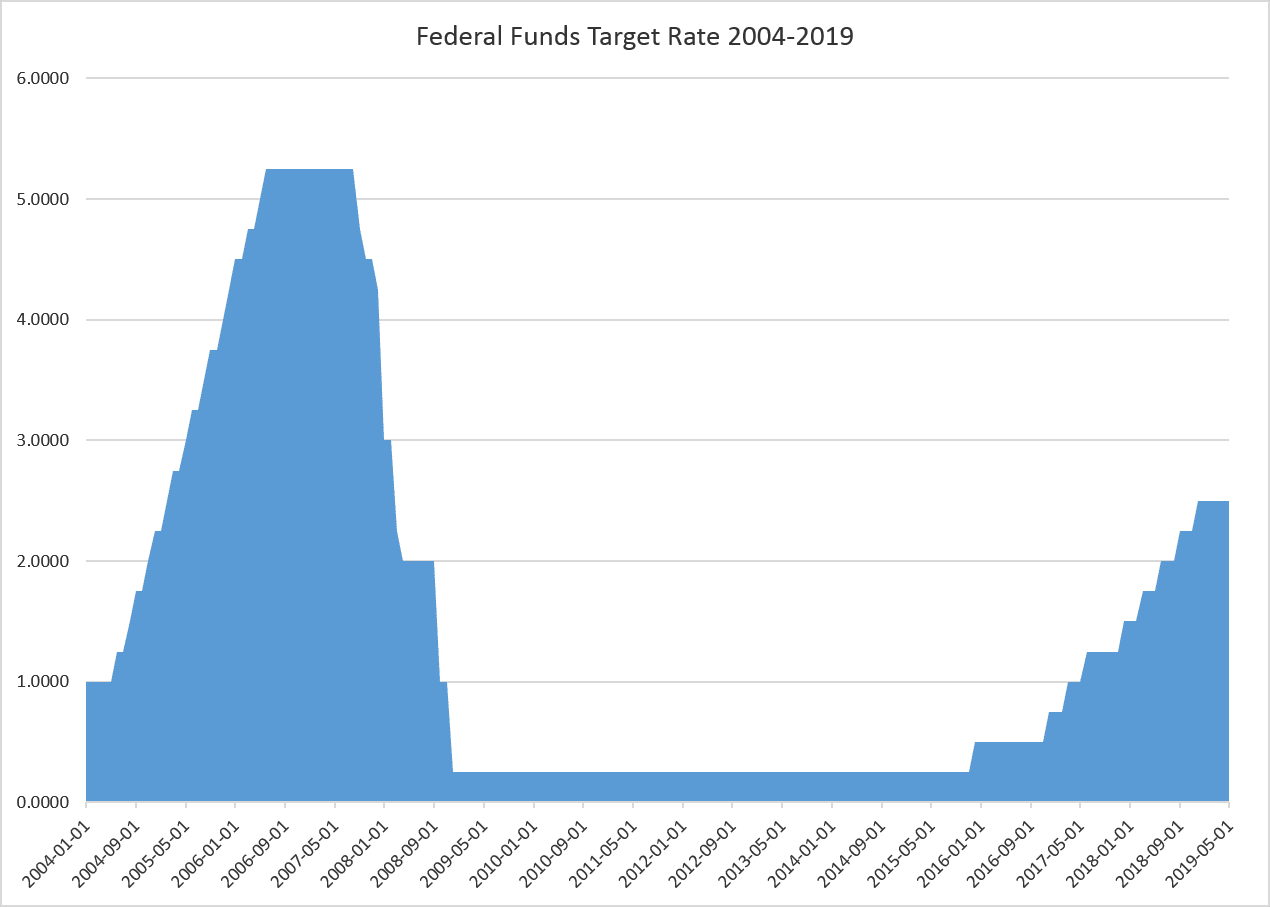

In a unanimous vote, the Fed kept the rate in a range of 2.25% to 2.5%.

The Fed’s reluctance to allow interest rates to return to what would be considered a more normal rate historically continues to spur speculation about what the Fed should do in case of a recession.

The media narratives from “experts” and policymakers we’re now hearing suggests three takeaways from last weeks’ developments from both the Fed board and at the Stanford monetary policy conference last Friday.

1. The Fed Fears the Economy Remains Fragile

For eight years, the federal funds rate remained near zero, and all the while, we were told the Fed was “cautiously optimistic” about the economy, and that economy growth was “solid” and moderately strong. Yet, the Fed could not bring itself to allow the target rate to rise above QE-level near-zero rates. Then, It wasn’t until 2017 that the rate was allowed to rise about one percent. By then, we were told that the Fed was just about to get aggressive with rates, taking the supposed strength of the economy as an opportunity to allow rates to rise to something resembling the four or five percent rate that might at least be in the same ballpark with what we saw during the past two expansions. That, however, now appears unlikely, even in the medium term. Fed policy has never approached anything we might call hawkish, and now Chairman Powell has already signaled 2.5 percent is quite high enough.

In spite of all the talk about “solid” growth, the Fed still sees the current economy as too fragile to deal with interest rates that would have been quite ordinary during the past 30 years.

The Trump administration, of course, points to the jobs data as “proof” of a strong economy, but outside that one group of data points, we find quite lackluster data otherwise, and the Fed knows it. Hence, it remains unenthusiastic about doing anything that would take it beyond its decade-long stance of embracing stimulus through low rates and a huge balance sheet.

2. Just Stay the Course

The Trump administration, of course, points to the jobs data as “proof” of a strong economy, but outside that one group of data points, we find quite lackluster data otherwise, and the Fed knows it. Hence, it remains unenthusiastic about doing anything that would take it beyond its decade-long stance of embracing stimulus through low rates and a huge balance sheet.

And this is why the Fed appears content to just stand as still as possible in hopes it won’t break any of the fragile and easily-broken stuff around it.

This is especially important when we consider the political importance of keeping interest rates low for the sake of keeping government debt payments low. If rates go up, Congress will face ever-harder choices about what spending to cut back in order to keep up with a growing debt-service load. No one in Congress wants to even think about that, and they want the Fed to keep it that way.

By adopting a policy of standing still, though, the Fed is pretty much guaranteeing that it will begin the next recession from a position in which it has already used up many of it’s stimulus tools. If interest rates are already low, and the Fed’s balance sheet is already nearly at $4 trillion. What tools are left?

3. Get Ready for Radical New Monetary Policy

Since the fed knows it will likely start from a very fragile position in the next recession, it is now “reviewing” its policy options. New York Fed President John Williams says now is the time to “rethink” how it has been doing things. But not in a good way. As Yahoo! Finance reports :

For its part, the Fed has acknowledged the concern and has launched a review of its monetary policy framework and communication practices. In focus: how it publicly explains and achieves its dual mandate of maximum employment and stable prices (through its 2% inflation target).

As part of this revising of policy, many proponents of dovish monetary policy are suggesting that much higher inflation targets should be in order, and that everyone should stop worrying about pushing prices well above the old targets.

This leads to the idea that what the fed needs is a “bazooka,” as noted by

Brian Cheung at AOL News:

“The central bank needs a ‘bazooka’ at the zero bound that makes credible its commitment to achieving its policy rule, and raising inflation if required,” Harvard economics professor Kenneth Rogoff said.

Rogoff’s recommendation : negative interest rate policy. The thesis: allowing interest rates to go negative, in which customers would be charged to keep money parked at their bank, would be a quicker way of spurring consumption and recovering jobs in a downturn.

Negative interest rates, of course, are an inflationist’s dream. Banks would penalize people for saving money (which is really just the same as investing money) so as to incentivize them to spend their money on consumer goods instead.

The idea, then, is that it would easier to hit high new inflation targets because negative-rate policy would impel people to spend as much money as possible as quickly as possible. Prices would then increase, further encouraging spending.

It’s basically just an old-fashioned inflationary spiral, but it’s all necessary, we’re told, to keep the economy going — at least until individuals want to retire or get into financial trouble. And then, suddenly, having no savings might be a problem.

But the experts at Harvard and the fed never let that sort of street-level household economics both them. What matters is macro policy, and the dream of a perfectly malleable economy that does what we tell it to do. And of course the economy will comply. We’ll have a bazooka!

{kind=link}