Gold has nearly doubled in two years. Silver has outpaced it. For the commodity that backed money for most of human history and that central banks still treat as the final settlement asset, these moves should represent a clean signal about physical scarcity and monetary demand. Western gold prices no longer carry that information cleanly.

The prices quoted in London and New York are increasingly detached from the physical reality of who owns what gold, where it sits, and whether it can be delivered on demand. What looks like a bull market is the early indication of a pricing system failure.

Context

Western bullion markets operate on a credit model. The London Bullion Market Association (LBMA) runs the largest gold market in the world, but most of the gold traded there is held in what the industry calls “unallocated” accounts. This means the customer holds a paper claim on a clearing bank rather than title to a specific bar in a vault.

When an investor buys an ounce through an LBMA member bank, the bank records a liability on its balance sheet and does not transfer ownership of any particular piece of metal. The Commodity Exchange in New York (COMEX) works on similar principles for futures contracts. Historically, fewer than one percent of COMEX contracts ever resulted in physical delivery. The rest were closed out or rolled forward as bookkeeping entries.

Eastern bullion markets operate on a property model. The Shanghai Gold Exchange (SGE)—the largest Asian gold venue and the operational arm of China’s central bank for physical gold—requires sellers to deposit physical metal before trading and buyers to pay in full upfront. More than 90 percent of SGE spot contracts result in actual delivery of actual bars.

The Shanghai Futures Exchange—the second major Chinese precious metals venue—operates on similar physical-first principles for its gold and silver futures. India’s retail and institutional buyers import and hold physical metal directly. Dubai’s trading hub treats allocated, segregated storage as the default condition rather than the premium option.

This difference reflects a philosophical choice about what gold is. Western markets have built their infrastructure around credit claims on pooled metal. Eastern markets have built theirs around title transfer of specific bars. The size of the gap between those two systems’ prices is now the most important indicator in the global bullion market.

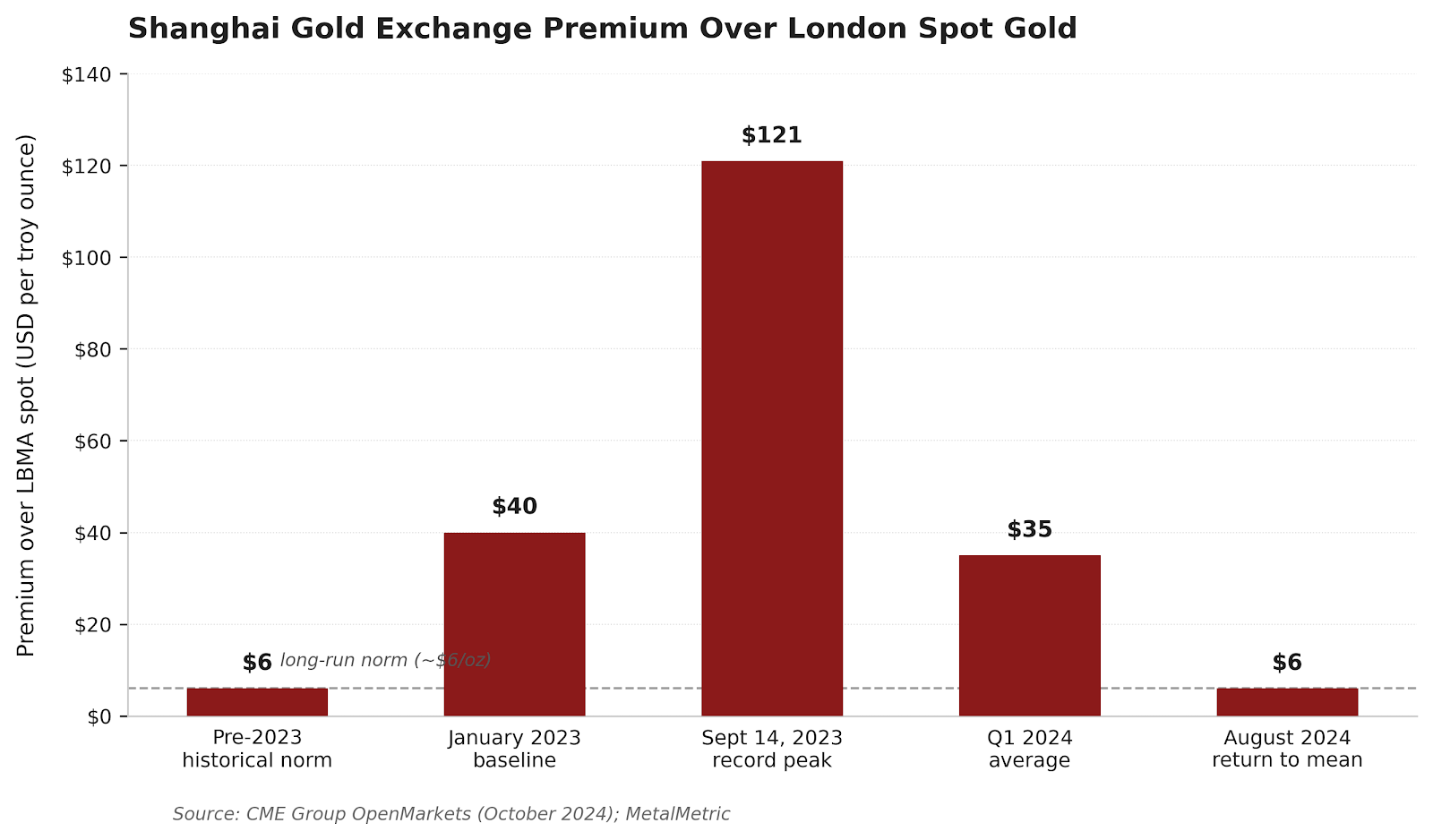

Figure 1: Shanghai Gold Exchange premium over London spot gold at selected moments, 2023-2024.

Sources: CME Group OpenMarkets and MetalMetric.

Geo-Economic Implications

When two systems price the same asset on different principles, the weaker system loses credibility first. That process is underway in Western paper markets, and the mechanism is straightforward. If a clearing bank owes ten customers an ounce each but holds only two ounces in the vault, the bank is solvent so long as the customers never ask for delivery.

When they do ask, the bank either delivers to the first two and defaults on the other eight, or it rushes to the physical market to buy metal at whatever price it takes. That forced bid is what produced the 70-dollar premium of New York futures over London spot during the March 2020 delivery crunch and the 40-to-60-dollar spreads that opened again in January 2025.

The deeper economic problem goes beyond the stress episodes themselves. What matters is what those episodes reveal about the reliability of Western gold prices as information. Investors hold gold as a hedge against inflation, currency debasement, and monetary policy errors. That function depends on a credible, deliverable price.

When the quoted price represents a paper claim that might or might not be convertible into metal under pressure, the signal stops working. Portfolio managers begin to discount the LBMA benchmark. Physical buyers ignore it. Central banks ignore it, which is exactly what their recent accumulation behavior suggests. A financial system that cannot produce a reliable price for its oldest asset has quietly lost control of one of its most important instruments.

The economic cost of this failure falls on savers. Anyone holding gold as insurance against currency risk faces a second, unacknowledged risk: that the reference price used to value their holdings does not correspond to metal that can actually be delivered.

Geopolitical Implications

Reserve currency status depends on trust in the financial architecture behind the currency. The United States dollar remains the dominant global reserve asset because sovereign holders believe American institutions will honor their claims.

That belief was shaken in February 2022 when Western allies froze approximately three hundred billion dollars in Russian central bank reserves. It is being shaken further by the growing suspicion that Western bullion markets may not be able to physically deliver the gold they say they hold.

Sovereign gold accumulation by China, India, Poland, Turkey, and others functions primarily as a risk management response to a technical problem rather than a political statement. If the LBMA commercial float cannot reliably meet demand from its own customers, then a foreign central bank with tonnes held in London custody must ask what happens to its claim during a stress episode.

The answer explains the repatriation programs now underway in Germany, the Netherlands, Hungary, Austria, Romania, and India. These decisions are prudential. The same logic drives sovereign wealth funds and ultra-high-net-worth investors toward direct physical custody in Singapore and Dubai, where allocated storage is contractually enforceable and the jurisdictional risk is lower.

The longer Western regulators tolerate this paper-to-physical mismatch, the faster marginal reserve decisions move eastward. Each stress episode that forces clearing banks to scramble for metal is watched by finance ministries worldwide as evidence that the Western system cannot honor its own contracts under pressure.

The dollar’s reserve status rests on the premise that American-backed financial promises are the most reliable claims on earth. That premise is being tested by a market the Treasury does not regulate and cannot easily reform.

The Reforms

Three reforms would address the core problem without requiring new bureaucracy or expanded regulatory authority.

First, restore traditional bailment law to unallocated bullion accounts. Under Anglo-American common law, a custodian holding property on behalf of a client cannot pledge or sell that property without explicit authorization. Bullion banking has been allowed to operate as an exception to this rule, treating customer gold as a bank asset that can be lent, leased, and rehypothecated at the bank’s discretion. Ending the exception would require any account marketed as gold ownership to correspond to a specific, identifiable bar held on the customer’s behalf.

Second, prohibit the rehypothecation of client bullion. When a bank holds a customer’s gold and simultaneously pledges that same gold as collateral on its own borrowings, the customer’s ownership is compromised without their knowledge or consent.

Calling the practice financial innovation does not change its underlying character. A straightforward prohibition would eliminate the legal foundation for the synthetic gold claims that now dominate Western markets.

Third, pass the Gold Reserve Transparency Act of 2025—House Resolution 3795—introduced by Representative Thomas Massie. The bill would require a Government Accountability Office physical assay of all United States gold reserves and full disclosure of every sovereign gold transaction over the past fifty years.

If the Treasury holds the metal it claims, an audit costs almost nothing and settles a question open since the early 1960s. If it does not, the public has a right to know before the answer becomes a crisis.

These three reforms share a common principle. They ask Western bullion markets to honor the property rights that the rest of the financial system takes for granted.

Forecast and Conclusion

Gold is supposed to be the simplest asset class on earth. It produces no cash flows, carries no counterparty risk by its physical nature, and derives its value from supply and demand for a physically finite element.

The difficulty now facing anyone trying to interpret its price comes entirely from the inflationary credit structures that Western markets have built around it.

Over the next several years, the divergence between Western paper prices and Eastern physical prices will widen. Western financial media will describe the resulting spreads as volatility. Eastern buyers will treat them as discounts on real metal and accumulate accordingly.

Central banks will bypass Western benchmarks because they no longer trust those benchmarks to reflect the underlying asset. As this continues, the basic question of what gold is actually worth at any given moment becomes harder to answer with confidence.

The correction is fundamentally about restoring property rights in a market that quietly abandoned them. New regulators, committees, and Basel frameworks are not the answer. Western bullion markets can fix themselves by admitting that a bar of gold is not a credit instrument, that a customer’s deposit is not a bank’s asset, and that the price of the oldest store of value on earth should reflect the metal itself, not the paper claims stacked on top of it.