During the most recent commercial real estate bubble, two things happened in tandem. First, due to the Federal Reserve’s zero interest rate policy, savers were unable to invest their cash at a decent rate of return. Second, prices of illiquid assets inflated in an extreme manner, riding on cheap debt and the rush of investors stretching for yield on their capital.

Such was the state of capital markets for several years, as the Obama, Trump, and Biden regimes—along with their counterparts at the Fed—pumped trillions of newly created dollars into the United States economy. Predictably, commercial real estate prices soared, rising to a crescendo in late 2021 to early 2022.

Throughout this time, the market for real estate investment trusts (REITs), companies that invest directly in commercial real estate, prospered—at least superficially. However, in 2022, the Fed began raising interest rates in response to high consumer price inflation. Commercial real estate values plunged. Publicly traded REITs, which trade on stock exchanges and must widely disclose their financial performance, have seen share prices drop 25–30 percent from their peak pricing at the end of 2021.

In spite of all this, private REITs such as Blackstone’s BREIT and Starwood Capital’s SREIT, which are not publicly traded and don’t disclose financial performance to the same degree as their public counterparts, have yet to report any meaningful price drops. Skeptical investors in those REITs are rushing for the exits, and the REITs themselves are barring the doors.

BREIT and SREIT

BREIT and SREIT began operations around 2018, focusing on investments in trendy market segments and locations like apartments and industrial property in the South and Southwest. Both REITs were marketed as accessible, safe, and secure investment products for the well-heeled but passive investor.

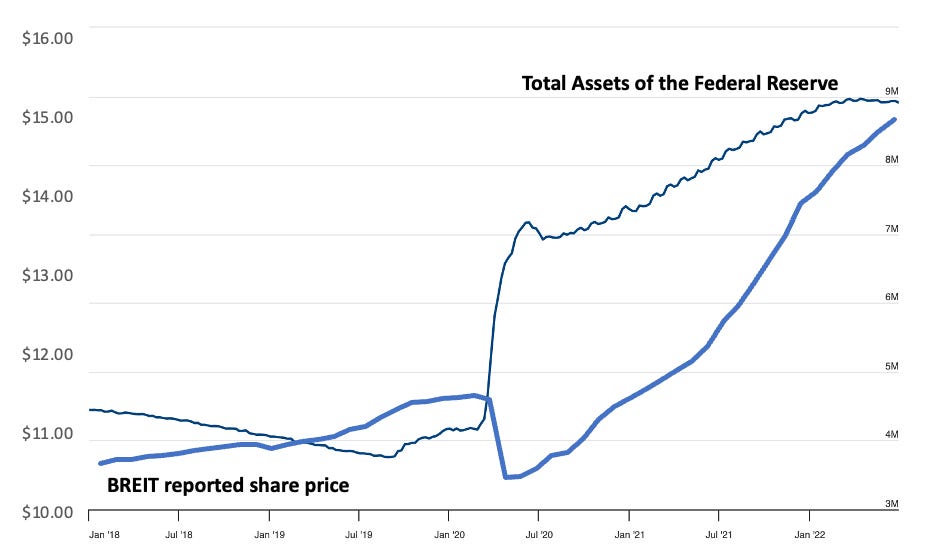

Asset prices tend to increase when the Fed prints trillions of dollars, and both REITs reported share price increases of roughly 50 percent from 2018 to early 2022.

Figure 1: BREIT share price as compared to the total assets of the Federal Reserve

Source: Data from the Board of Governors of the Federal Reserve System and Blackstone Real Estate Income Trust.

In 2022, however, the music stopped as the Federal Reserve began raising interest rates in response to high Consumer Price Index readings.

Predictably, the commercial real estate market responded with a crash. Publicly traded REITs nosedived, and cap rates—which measure the ratio of a property’s income to its market value—increased by 46 percent from Q1 2022 to Q3 2023 in prime apartment markets, an area of heavy concentration for BREIT and SREIT. That increase in cap rates implies a reduction of 31.5 percent in asset values.

Nothing to See Here

Despite the carnage in commercial real estate, BREIT and SREIT have reported share prices that have hardly budged, declining only 2 percent and 6 percent, respectively, since the end of 2021. Yet, in contrast to this sanguine picture presented by the REITs, the REIT investors have been demanding to cash out in droves.

Beginning in late 2022, BREIT began receiving large redemption requests from investors who were concerned about their exposure to commercial real estate and wished to cash out. These redemption requests peaked at $5.3 billion in January of 2023—roughly 8 percent of total assets at the time—but have not ceased, leading to a streak of monthly redemption requests that has continued through December 2023. SREIT has experienced essentially the same.

In response, BREIT and SREIT have limited redemptions to 2 percent of net asset value per month and 5 percent per quarter. This means that, each and every month, investors who wish to cash out are unable to.

It also means that the total assets under management are declining sharply. BREIT assets have dropped from over $70 billion to approximately $57 billion despite the redemption caps.

Continued investor redemptions coupled with potential negative developments in the capital markets—particularly a resurgence of consumer price inflation and a reassessment of rate cut expectations—could set off a doom loop, where investors rush to redeem their shares while prices are artificially inflated, encouraging others to do the same, ultimately resulting in a chaotic run.

REIT managers are keenly aware of this possible outcome. To combat it, they have deployed the true extent of their talents—lobbying the government and Federal Reserve for special privileges and bailouts.

Real Estate Roundtable—Won’t Someone Think of the Investment Bankers?

In March of 2023, the Real Estate Roundtable, a lobbying group based in Washington, DC, whose board prominently features leaders of both Blackstone and Starwood, sent a pathetic, mewling letter to the heads of the Federal Reserve and various other federal agencies.

The letter’s purpose was clear—to plead for an immediate bailout that would rescue imprudent institutional borrowers from the consequences of their investment decisions. The letter states:

We are writing to encourage the financial services regulatory agencies . . . to reestablish immediately a program similar to prior programs . . . to work prudently with borrowers on commercial real estate troubled debt restructurings (TDRs). This action is needed as soon as possible. . .

At this critical time, it is important that the Agencies do not engage in pro-cyclical policies such as requiring financial institutions to increase capital and liquidity levels to reflect current mark to market models. These policies would have the unintended consequence of further diminishing liquidity and creating additional downward pressure on asset values. A deflationary spiral must be avoided at all costs. . . .

. . . Immediate value adjustments to reflect the new interest rate environment would lead to potentially significant value declines, requiring unprecedented additional equity investments or capital reserves. (emphasis added)

The lobbyist-bankers are telling the government that they don’t want to accurately report asset values to their investors and shareholders, fearing the negative consequences. As such, the government must step in to eliminate that possibility and ease their discomfort. All at the cost of the American taxpayer, of course.

In Pavlovian style, the letter also references, as justification for the demand, four other commercial real estate bailout programs executed by the government in the last fifteen years (2009, 2010, 2020, and 2022).

Admit the Reality of Your Situation

In the midst of the ongoing commercial real estate crash, private REITs are suppressing price signals and hiding the extent of the damage in their portfolios on the hope, conditioned by years of similar treatment, that the Fed will soon rescue them from their failures.

However, investors trying to cash out see the writing on the wall. The gloom in commercial real estate, caused by yet another artificial boom that went bust, can’t be gainsaid by inflating share prices in quarterly reports. Begging for bailouts doesn’t foster confidence that these REITs are indeed “all-weather” investment strategies that “build long-term wealth across market cycles,” as claimed in one of their latest quarterly reports.