The current economic conditions in the U.S. compared to the conditions of the period from 1995–2000 have generated, according to Edmund Phelps (”False Hopes for the Economy and False Fears,” Wall Street Journal, June 3, 2003), two false hopes for the economy and two false fears. But is he justified in his interpretation of these false hopes and false fears?

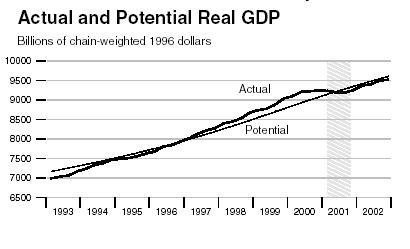

The first false hope is that we are in a recession and we can expect “recovery,” a return to the golden days of the late 1990s. Phelps asks, “But what recession?” A look at real GDP relative to the trend can be interpreted as a temporary bubble where Real GDP and growth rates were temporarily higher than the trend, but “we are more or less back to normalcy. It was the boom that was abnormal.” No harm—no foul, but do not expect a recovery, i.e., a return to the abnormal. This is one possible interpretation of the data from The Federal Reserve Bank of St. Louis. More on this interpretation later.

His second false hope is one that Austrians should applaud. The hope associated with the “aggregate demand” fallacy. The economy can be moved back to the dream levels of the late 1990s by effective “stimulus,” if the Fed gives support with low interest rates and ample liquidity or Congress does it by spending money. Such a hope is truly a false hope as explained by Phelps and Frank Shostak.

But of real concern here is his false “false fear.” Professor Phelps attempts to undermine the current resurgence of interest in the Austrian cycle. He states, “One of the most unreasoning fears, yet pervasive, is the nightmare of the interwar Austrian cycle theory: ‘overinvestment.’ But, the current boom-bust of the U.S. economy has, with good reason, led some in the business press to re-examine the Mises-Hayek theory of the business cycle. As an example, The Economist (September 28, 2002, p. 9) states:

The recent business cycle in both America and Japan displayed many “Austrian” features. Hayek argued that the natural rate of interest could rise if faster productivity growth increased expectations about profits and hence investment opportunities. This is what happened in Japan in the 1980s and in America in the 1990s. If such a shift in investment occurs, central banks need to raise interest rates. But because inflation was low (and because Austrian economics had long gone out of fashion), the Fed and the Bank of Japan failed to do so. The cost of capital fell below its expected return, fueling a surge in credit, equity prices and investment.1

A casual examination of the U.S. data from 1995 to 2000 reveals that the developments in the U.S. economy during this period certainly are consistent with the basic features of an Austrian boom-bust cycle. The Austrian boom begins when central bank activity creates credit. The actual interest rate(s) may or may not fall, but the created credit causes interest rates to be below the natural rate of interest2 .

While it is difficult to develop an exact measure of credit creation, the monetary base can provide a lower limit estimate and money zero maturity (MZM) provides a possible upper limit estimate. From late 1995 or early 1996 the monetary base growth rate accelerated from around 2% to a peak of above 15% in late 1999. MZM followed a very similar pattern with negative growth rates in 1995 to 15% growth rates per year by 1999.

Real GDP, with an appropriate, slight lag, exhibits a boom during this period as predicted by Austrian business cycle theory. By late 1996–early 1997 GDP, which had been tracking its potential growth path, begins to grow more rapidly (through 1999) than trend and actual GDP exceeds potential GDP up until 2001. GDP growth becomes flat and then negative in 2001 and GDP falls below potential GDP. This is an alternative and better interpretation of the 1990s boom and bust than Phelps’s return to normalcy.

But, in truth, what should be real is a legitimate concern about the consequences of an unsustainable boom and what is blatantly false is Phelps’s characterization of the Austrian cycle theory. The Austrian cycle theory is a theory, not of overinvestment in the sense used by Phelps, but of the misdirection of production, malinvestment, which is accompanied by overinvestment and overconsumption properly understood.3

At the heart of Phelps’s misrepresentation or misinterpretation of Austrian business cycle theory is his capital theory and a lack of an appreciation for the important role of saving in the wealth creation process. Robert D. McTeer, “The Dismal Science? Hardly!” (WSJ, June 4, 2003) makes a similar error in his defense of Keynes’s paradox of thrift, which he uses as an example of the fallacy of composition, “Individually, most consumers need to save more. But if all or many consumers start trying to save more, the economy will be in deep trouble.”

McTeer, President of the Federal Reserve Bank of Dallas, fails to recognize that the paradox of thrift is just the broken window fallacy, which he does an excellent job of explaining, in a more subtle guise.

Most “Austrians” would agree with Phelps that “world markets would react to the addition of capital with a sharp drop of interest, a skyward jump of capital goods prices, and immediate lift of real wages and jobs.” But Phelps, unlike the Austrian, fails to realize that a sudden addition of capital is not heaped on the world, it comes from increased saving. This increase in capital is Garrison’s sustainable growth. Such growth in the capital stock would not represent overinvestment.

As Phelps points out, expectations of future productivity increase investment demand and such expectations did drive the U.S. economy in the 1990s. But as pointed out in the article in The Economist, the shift of economic activity towards investment as a result of the “technology shock” by itself should not create a boom-bust pattern. Without Central Bank intervention in the credit markets, the higher demand for credit should have increased interest rates and saving. The economy should make a relatively smooth adjustment to a higher sustainable growth path.

The boom bust cycle developed, because, as happened in the U.S. economy, credit creation through central bank intervention caused markets to respond as if more “capital” was available when in fact it was not. The higher level of investment from 1996 to 2000 as estimated by Phelps as 2% of GDP per year and the associated additional economic growth was a combination of sustainable investment and growth consistent with underlying resource constraints and time preferences, malinvestments—investments in the wrong kinds of capital goods, and overinvestment and overconsumption investment and consumption generated by the use of “capital equipment and labor beyond the levels associated with full employment.4 “

The bust or crisis is just the discovery of the misdirections of production and the necessary fundamental readjustments in the economy that are necessary to make production and growth consistent with available resources, technology, and preferences.

Without the credit created malinvestments, the U.S. economy, instead of returning to Phelps’s normalcy, would potentially be on a permanently higher growth path albeit not one as high as the one generated by the credit creation. The consequences of the malinvestments should thus be a legitimate concern, and if there are significant interferences to the necessary market adjustments; bankruptcies, liquidations, declines in wages and resource prices in markets where the resources are no longer needed, and relocation of capital goods and labor to areas consistent with the pattern of demand, these concerns should turn into legitimate fears.

But, not to end on too negative a note, we must agree with Professor Phelps, “We need to guard against European corporatism and old fashion cronyism. The real hope is that the enterprising spirit is so strong here that, even if the system is not tuned up for the best, there will continue to be enough upstart entrepreneurs and established ones that will hit upon ideas for new products and methods worth developing and trying to market.”

But whereas Phelps would “look forward to normal times, with their ups and downs,” with a greater understanding of ABCT and its greater acceptance by businessmen and policy makers, we could look forward to greater prosperity without the ups and downs associated with boom and bust.

- 1For a more detailed application of Austrian business cycle theory to the case of Japan, see Powell, “Explaining Japan’s Recession,”QJAE Summer 2002 and from Mises Daily article, “Explaining Japan’s Recession.“ Mises Daily article, mises.org, Dec. 3.

- 2See Cochran, Call, and Glahe, “Austrian Business Cycle Theory: Variations on a Theme,” Quarterly Journal of Austrian Economics, 6 (1).

- 3See Roger Garrison, “Overconsumption and Forced Saving in the Mises-Hayek Theory of the Business Cycle” at http://www.auburn.edu/~garriro/strigl.htm for an excellent discussion and extension of the cycle theory.

- 4This characterization of overconsumption and overinvestment is from Roger Garrison.