China has experienced one of the great economic transformations in the history of the world, owing to economic reforms that unleashed astonishing productive capacity that had been bottled up for long period of state controls. And yet this transformation has been endangered by the bane of all booms under fiat money: money and credit creation. The question is whether China’s boom will settle softly or coming crashing down.

The latest data indicates that strong economic activity remains intact. Thus the 3-month moving average of the yearly rate of growth of industrial production jumped to 20.6% in April from 16.6% in March.

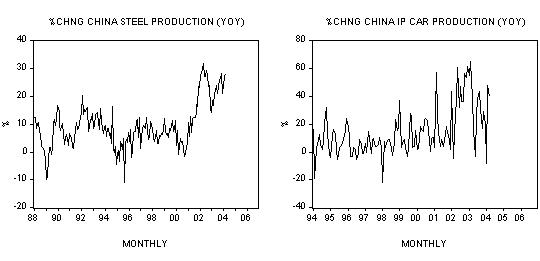

The growth momentum of the production of steel continues to display buoyancy. Year-on-year steel production stood at 28.3% in March versus 27% in February. Also, car production displays buoyancy. The yearly rate of growth of car production stood at 40% in March against 48% in the previous month.

Although the pace of investment in fixed assets eased slightly in April it nonetheless remains very strong. The yearly rate of growth of fixed asset investment stood at 42.8% in April against 47.8% in March.

Furthermore real GDP grew year-on-year in Q1 by 9.8% after expanding by 9.9% in Q4 last year. Retail sales have continued to display strength. The yearly rate of growth of retail sales jumped to 13.2% in April from 11.1% in the previous month.

Since April last year, Chinese authorities have introduced various measures to cool off economic activity. The central bank raised the amount of cash that banks must keep in reserve requirements by 0.5% to 8%. Also, China’s central bank has expanded open-market operations to twice a week from once weekly. These measures are starting to show some effect on the rate of growth of bank loans. Thus after rising to 23.9% in August 2003 the yearly rate of growth loans fell to 19.8% in April. Furthermore, after rising by 52.5% in January last year, year-on-year lending for construction activities fell by 6.6% in April.

For the time being, however, the growth momentum of money M1 continues apace. The yearly rate of growth of this monetary measure stood at 20% in April against 20.1% in the previous month.

Meanwhile the effect of strong increases in the yearly rate of growth of money M1 can be clearly seen through the growth momentum of the consumer price index (CPI). After falling to 2.1% in February the yearly rate of growth of the CPI jumped to 3.8% in April.

Should this rise in CPI growth momentum intensify further it is quite likely that the Chinese authorities will be forced to introduce much tougher measures. For instance, some Chinese officials have suggested that the central bank may lift the one-year lending rate, which is currently stands at 5.31%.

Here is where we find the most severe risk. This possible increase in interest rates runs the risk of bursting the bubble and plunging the economy into a recession.

Chinese authorities, however, believe that they can stage an orderly deflation of the bubble and thereby prevent an economic bust. However, it is questionable as to whether an orderly deflation of the bubble i.e. a soft landing, is possible. There is a high likelihood that due to the aggressive lowering of interest rates by the central bank from 11% in 1996 to 5.3% at present a severe misallocation of resources has occurred. We suggest that this makes the economy so much more vulnerable to any tight monetary policy.

Should the growth momentum of money supply contract sharply on account of a possible sharp fall in bank lending, economic activity will follow suit. For example, a fall in the yearly rate of growth of money M1 from 54% in Q2 1993 to 14% in Q2 1996 plunged the nominal GDP rate of growth from 69% in Q4 1994 to 2% in Q4 1997.

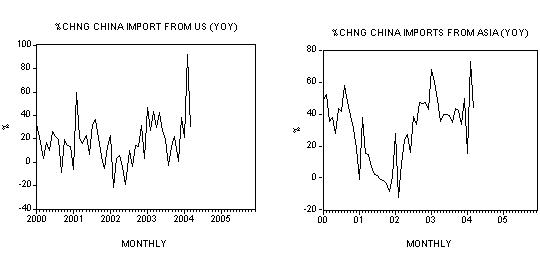

In sum, it seems that a bust is more likely than Chinese authorities are currently admitting. A possible bust of the Chinese economy is likely to be bad news for the US and other world economies. There are already indications that the rate of increase of China’s imports is slowing down. After rising to 76.7% in February the yearly rate of growth of imports fell to 42.7% in April.

In this respect, the growth momentum of imports from the US fell sharply in March. Year-on-year the rate of growth fell to 29.4% from 92.2% in February. The yearly rate of growth of China’s imports from Asia fell to 43.4% in March from 73% in the previous month.

To prepare for the possibility of a genuine bust, there is only course of action for China: it can and should be mitigated by further liberalizations of capital investment rules and even more privatization. This is the only “countercyclical” policy the government should consider, since all efforts to reflate are doomed to fail.