11. Money and Its Purchasing Power

11. Money and Its Purchasing Power

1. Introduction

1. Introduction

MONEY HAS ENTERED INTO ALMOST all our discussion so far. In chapter 3 we saw how the economy evolved from barter to indirect exchange. We saw the patterns of indirect exchange and the types of allocations of income and expenditure that are made in a monetary economy. In chapter 4 we discussed money prices and their formation, analyzed the marginal utility of money, and demonstrated how monetary theory can be subsumed under utility theory by means of the money regression theorem. In chapter 6 we saw how monetary calculation in markets is essential to a complex, developed economy, and we analyzed the structure of post-income and pre-income demands for and supplies of money on the time market. And from chapter 2 on, all our discussion has dealt with a monetary-exchange economy.

The time has come to draw the threads of our analysis of the market together by completing our study of money and of the effects of changes in monetary relations on the economic system. In this chapter we shall continue to conduct the analysis within the framework of the free-market economy.

2. The Money Relation: The Demand for and the Supply of Money

2. The Money Relation: The Demand for and the Supply of Money

Money is a commodity that serves as a general medium of exchange; its exchanges therefore permeate the economic system. Like all commodities, it has a market demand and a market supply, although its special situation lends it many unique features. We saw in chapter 4 that its “price” has no unique expression on the market. Other commodities are all expressible in terms of units of money and therefore have uniquely identifiable prices. The money commodity, however, can be expressed only by an array of all the other commodities, i.e., all the goods and services that money can buy on the market. This array has no uniquely expressible unit, and, as we shall see, changes in the array cannot be measured. Yet the concept of the “price” or the “value” of money, or the “purchasing power of the monetary unit,” is no less real and important for all that. It simply must be borne in mind that, as we saw in chapter 4, there is no single “price level” or measurable unit by which the value-array of money can be expressed. This exchange-value of money also takes on peculiar importance because, unlike other commodities, the prime purpose of the money commodity is to be exchanged, now or in the future, for directly consumable or productive commodities.

The total demand for money on the market consists of two parts: the exchange demand for money (by sellers of all other goods that wish to purchase money) and the reservation demand for money (the demand for money to hold by those who already hold it). Because money is a commodity that permeates the market and is continually being supplied and demanded by everyone, and because the proportion which the existing stock of money bears to new production is high, it will be convenient to analyze the supply of and the demand for money in terms of the total demand-stock analysis set forth in chapter 2.1

In contrast to other commodities, everyone on the market has both an exchange demand and a reservation demand for money. The exchange demand is his pre-income demand (see chapter 6, above). As a seller of labor, land, capital goods, or consumers’ goods, he must supply these goods and demand money in exchange to obtain a money income. Aside from speculative considerations, the seller of ready-made goods will tend, as we have seen, to have a perfectly inelastic (vertical) supply curve, since he has no reservation uses for the good. But the supply curve of a good for money is equivalent to a (partial) demand curve for money in terms of the good to be supplied. Therefore, the (exchange) demand curves for money in terms of land, capital goods, and consumers’ goods will tend to be perfectly inelastic.

For labor services, the situation is more complicated. Labor, as we have seen, does have a reserved use—satisfying leisure. We have seen that the general supply curve of a labor factor can be either “forward-sloping” or “backward-sloping,” depending upon the individuals’ marginal utility of money and marginal disutility of leisure forgone. In determining labor’s demand curve for money, however, we can be far more certain. To understand why, let us take a hypothetical example of a supply curve of a labor factor (in general use). At a wage rate of five gold grains an hour, 40 hours per week of labor service will be sold. Now suppose that the wage rate is raised to eight gold grains an hour. Some people might work a greater number of hours because they have a greater monetary inducement to sacrifice leisure for labor. They might work 50 hours per week. Others may decide that the increased income permits them to sacrifice some money and take some of the increased earnings in greater leisure. They might work 30 hours. The first would represent a “forward-sloping,” the latter a “backward-sloping,” supply curve of labor in this price range. But both would have one thing in common. Let us multiply hours by wage rate in each case, to arrive at the total money income of the laborers in the various situations. In the original case, a laborer earned 40 times 5 or 200 gold grains per week. The man with a backward-sloping supply curve will earn 30 times 8 or 240 gold grains a week. The one with a forward-sloping supply curve will earn 50 times 8 or 400 gold grains per week. In both cases, the man earns more money at the higher wage rate.

This will always be true. In the first case, it is obvious, for the higher wage rate induces the man to sell more labor. But it is true in the latter case as well. For the higher money income permits a man to gratify his desires for more leisure as well, precisely because he is getting an increased money income. Therefore, a man’s backward-sloping supply curve will never be “backward” enough to make him earn less money at higher wage rates.

Thus, a man will always earn more money at a higher wage rate, less money at a lower. But what is earning money but another name for buying money? And that is precisely what is done. People buy money by selling goods and services that they possess or can create. We are now attempting to arrive at the demand schedule for money in relation to various alternative purchasing powers or “exchange-values” of money. A lower exchange-value of money is equivalent to higher goods-prices in terms of money. Conversely, a higher exchange-value of money is equivalent to lower prices of goods. In the labor market, a higher exchange-value of money is translated into lower wage rates, and a lower exchange-value of money into higher wage rates.

Hence, on the labor market, our law may be translated into the following terms: The higher the exchange-value of money, the lower the quantity of money demanded; the lower the exchange-value of money, the higher the quantity of money demanded (i.e., the lower the wage rate, the less money earned; the higher the wage rate, the more money earned). Therefore, on the labor market, the demand-for-money schedule is not vertical, but falling, when the exchange-value of money increases, as in the case of any demand curve.

Adding the vertical demand curves for money in the other exchange markets to the falling demand curve in the labor market, we arrive at a falling exchange-demand curve for money.

More important, because more volatile, in the total demand for money on the market is the reservation demand to hold money. This is everyone’s post-income demand. After everyone has acquired his income, he must decide, as we have seen, between the allocation of his money assets in three directions: consumption spending, investment spending, and addition to his cash balance (“net hoarding”). Furthermore, he has the additional choice of subtraction from his cash balance (“net dishoarding”). How much he decides to retain in his cash balance is uniquely determined by the marginal utility of money in his cash balance on his value scale. Until now we have discussed at length the sources of the utilities and demands for consumers’ goods and for producers’ goods. We have now to look at the remaining good: money in the cash balance, its utility and demand.

Before discussing the sources of the demand for a cash balance, however, we may determine the shape of the reservation (or “cash balance”) demand curve for money. Let us suppose that a man’s marginal utilities are such that he wishes to have 10 ounces of money held in his cash balance over a certain period. Suppose now that the exchange-value of money, i.e., the purchasing power of a monetary unit, increases, other things being equal. This means that his 10 gold ounces accomplish more work than they did before the change in the PPM (purchasing power of the monetary unit). As a consequence, he will tend to remove part of the 10 ounces from his cash balance and spend it on goods, the prices of which have now fallen. Therefore, the higher the PPM (the exchange-value of money), the lower the quantity of money demanded in the cash balance. Conversely, a lower PPM will mean that the previous cash balance is worth less in real terms than it was before, while the higher prices of goods discourage their purchase. As a result, the lower the PPM, the higher the quantity of money demanded in the cash balance.

As a result, the reservation demand curve for money in the cash balance falls as the exchange-value of money increases. This falling demand curve, added to the falling exchange-demand curve for money, yields the market’s total demand curve for money—also falling in the familiar fashion for every commodity.

There is a third demand curve for the money commodity that deserves mention. This is the demand for nonmonetary uses of the monetary metal. This will be relatively unimportant in the advanced monetary economy, but it will exist nevertheless. In the case of gold, this will mean either uses in consumption, as for ornaments, or productive uses, as for industrial purposes. At any rate, this demand curve also falls as the PPM increases. As the “price” of money (PPM) increases, more goods can be obtained through expenditure of a unit of money; as a result, the opportunity-cost in using gold for nonmonetary purposes increases, and less is demanded for that purpose. Conversely, as the PPM falls, there is more incentive to use gold for its direct use. This demand curve is added to the total demand curve for money, to obtain the total demand curve for the money commodity.2

At any one time there is a given total stock of the money commodity. This stock will, at any time, be owned by someone. It is therefore dangerously misleading to adopt the custom of American economists since Irving Fisher’s day of treating money as somehow “circulating,” or worse still, as divided into “circulating money” and “idle money.”3 This concept conjures up the image of the former as moving somewhere at all times, while the latter sits idly in “hoards.” This is a grave error. There is, actually, no such thing as “circulation,” and there is no mysterious arena where money “moves.” At any one time all the money is owned by someone, i.e., rests in someone’s cash balance. Whatever the stock of money, therefore, people’s actions must bring it into accord with the total demand for money to hold, i.e., the total demand for money that we have just discussed. For even pre-income money acquired in exchange must be held at least momentarily in one’s cash balance before being transferred to someone else’s balance. All total demand is therefore to hold, and this is in accord with our analysis of total demand in chapter 2.

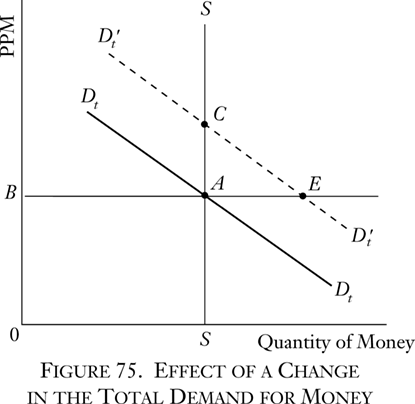

Total stock must therefore be brought into agreement, on the market, with the total quantity of money demanded. The diagram of this situation is shown in Figure 74.

On the vertical axis is the PPM, increasing upward. On the horizontal axis is the quantity of money, increasing rightwards. De is the aggregate exchange-demand curve for money, falling and inelastic.

Dr is the reservation or cash-balance demand for money. Dt is the total demand for money to hold (the demand for nonmonetary gold being omitted for purposes of convenience). Somewhere intersecting the Dt curve is the SS vertical line—the total stock of money in the community—given at quantity 0S.

The intersection of the latter two curves determines the equilibrium point, A, for the exchange-value of money in the community. The exchange-value, or PPM, will be set at 0B.

Suppose now that the PPM is slightly higher than 0B. The demand for money at that point will be less than the stock. People will become unwilling to hold money at that exchange-value and will be anxious to sell it for other goods. These sales will raise the prices of goods and lower the PPM, until the equilibrium point is reached. On the other hand, suppose that the PPM is lower than 0B. In that case, more people will demand money, in exchange or in reservation, than there is money stock available. The consequent excess of demand over supply will raise the PPM again to 0B.

- 1Cf. Edwin Cannan, “The Application of the Theoretical Analysis of Supply and Demand to Units of Currency” in F.A. Lutz and L.W. Mints, eds., Readings in Monetary Theory (Philadelphia: Blakiston, 1951), pp. 3–12, and Cannan, Money (6th ed.; London: Staples Press, 1929), pp. 10–19, 65–78.

- 2From this point on, this nonmonetary demand is included, for convenience, in the “total demand for money.”

- 3Cf. Irving Fisher, The Purchasing Power of Money (2nd ed.; New York: Macmillan & Co., 1913).

3. Changes in the Money Relation

3. Changes in the Money Relation

The purchasing power of money is therefore determined by two factors: the total demand schedule for money to hold and the stock of money in existence. It is easy to see on a diagram what happens when either of these determining elements changes. Thus, suppose that the schedule of total demand increases (shifts to the right). Then (see Figure 75) the total-demand-for-money curve has shifted from DtDt to Dt′Dt′. At the previous equilibrium PPM point, A, the demand for money now exceeds the stock available by AE. The bids push the PPM upwards until it reaches the equilibrium point C. The converse will be true for a shift of the total demand curve leftward—a decline in the total demand schedule. Then, the PPM will fall accordingly.

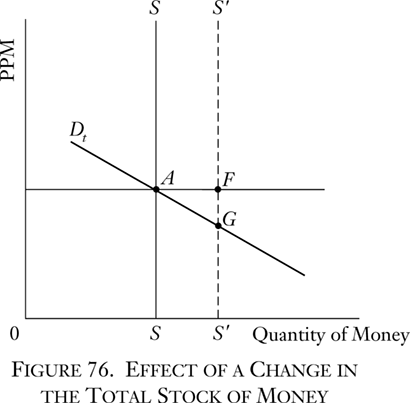

The effect of a change in the total stock, the demand curve remaining constant, is shown in Figure 76. Total quantity of stock increases from 0S to 0S′. At the new stock level there is an excess of stock, AF, over the total demand for money. Money will be sold at a lower PPM to induce people to hold it, and the PPM will fall until it reaches a new equilibrium point G. Conversely, if the stock of money is decreased, there will be an excess of demand for money at the existing PPM, and the PPM will rise until the new equilibrium point is reached.

The effect of the quantity of money on its exchange-value is thus simply set forth in our analysis and diagrams.

The absurdity of classifying monetary theories into mutually exclusive divisions (such as “supply and demand theory,” “quantity theory,” “cash balance theory,” “commodity theory,” “income and expenditure theory”) should now be evident.4 For all these elements are found in this analysis. Money is a commodity; its supply or quantity is important in determining its exchange-value; demand for money for the cash balance is also important for this purpose; and the analysis can be applied to income and expenditure situations.

- 4A typical such classification can be found in Lester V. Chandler, An Introduction to Monetary Theory (New York: Harper & Bros., 1940).

4. Utility of the Stock of Money

4. Utility of the Stock of Money

In the case of consumers’ goods, we do not go behind their subjective utilities on people’s value scales to investigate why they were preferred; economics must stop once the ranking has been made. In the case of money, however, we are confronted with a different problem. For the utility of money (setting aside the nonmonetary use of the money commodity) depends solely on its prospective use as the general medium of exchange. Hence the subjective utility of money is dependent on the objective exchange-value of money, and we must pursue our analysis of the demand for money further than would otherwise be required.5 The diagrams above in which we connected the demand for money and its PPM are therefore particularly appropriate. For other goods, demand in the market is a means of routing commodities into the hands of their consumers. For money, on the other hand, the “price” of money is precisely the variable on which the demand schedule depends and to which almost the whole of the demand for money is keyed. To put it in another way: without a price, or an objective exchange-value, any other good would be snapped up as a welcome free gift; but money, without a price, would not be used at all, since its entire use consists in its command of other goods on the market. The sole use of money is to be exchanged for goods, and if it had no price and therefore no exchange-value, it could not be exchanged and would no longer be used.

We are now on the threshold of a great economic law, a truth that can hardly be overemphasized, considering the harm its neglect has caused throughout history. An increase in the supply of a producers’ good increases, ceteris paribus, the supply of a consumers’ good. An increase in the supply of a consumers’ good (when there has been no decrease in the supply of another good) is demonstrably a clear social benefit; for someone’s “real income” has increased and no one’s has decreased.6

Money, on the contrary, is solely useful for exchange purposes. Money, per se, cannot be consumed and cannot be used directly as a producers’ good in the productive process. Money per se is therefore unproductive; it is dead stock and produces nothing. Land or capital is always in the form of some specific good, some specific productive instrument. Money always remains in someone’s cash balance.

Goods are useful and scarce, and any increment in goods is a social benefit. But money is useful not directly, but only in exchanges. And we have just seen that as the stock of money in society changes, the objective exchange-value of money changes inversely (though not necessarily proportionally) until the money relation is again in equilibrium. When there is less money, the exchange-value of the monetary unit rises; when there is more money, the exchange-value of the monetary unit falls. We conclude that there is no such thing as “too little” or “too much” money, that, whatever the social money stock, the benefits of money are always utilized to the maximum extent. An increase in the supply of money confers no social benefit whatever; it simply benefits some at the expense of others, as will be detailed further below. Similarly, a decrease in the money stock involves no social loss. For money is used only for its purchasing power in exchange, and an increase in the money stock simply dilutes the purchasing power of each monetary unit. Conversely, a fall in the money stock increases the purchasing power of each unit.

David Hume’s famous example provides a highly oversimplified view of the effect of changes in the stock of money, but in the present context it is a valid illustration of the absurdity of the belief that an increased money supply can confer a social benefit or relieve any economic scarcity. Consider the magical situation where every man awakens one morning to find that his monetary assets have doubled. Has the wealth, or the real income, of society doubled? Certainly not. In fact, the real income—the actual goods and services supplied—remains unchanged. What has changed is simply the monetary unit, which has been diluted, and the purchasing power of the monetary unit will fall enough (i.e., prices of goods will rise) to bring the new money relation into equilibrium.

One of the most important economic laws, therefore, is: Every supply of money is always utilized to its maximum extent, and hence no social utility can be conferred by increasing the supply of money.

Some writers have inferred from this law that any factors devoted to gold mining are being used unproductively, because an increased supply of money does not confer a social benefit. They deduce from this that the government should restrict the amount of gold mining. These critics fail to realize, however, that gold, the money-commodity, is used not only as money but also for nonmonetary purposes, either in consumption or in production. Hence, an increase in the supply of gold, although conferring no monetary benefit, does confer a social benefit by increasing the supply of gold for direct use.

5. The Demand for Money

5. The Demand for Money

A. Money in the ERE and in the Market

A. Money in the ERE and in the Market

It is true, as we have said, that the only use for money is in exchange. From this, however, it must not be inferred, as some writers have done, that this exchange must be immediate. Indeed, the reason that a reservation demand for money exists and cash balances are kept is that the individual is keeping his money in reserve for future exchanges. That is the function of a cash balance—to wait for a propitious time to make an exchange.

Suppose the ERE has been established. In such a world of certainty, there would be no risk of loss in investment and no need to keep cash balances on hand in case an emergency for consumer spending should arise. Everyone would therefore allocate his money stock fully, to the purchase of either present goods or future goods, in accordance with his time preferences. No one would keep his money idle in a cash balance. Knowing that he will want to spend a certain amount of money on consumption in six months’ time, a man will lend his money out for that period to be returned at precisely the time it is to be spent. But if no one is willing to keep a cash balance longer than instantaneously, there will be no money held and no use for a money stock. Money, in short, would either be useless or very nearly so in the world of certainty.

In the real world of uncertainty, as contrasted to the ERE, even “idle” money kept in a cash balance performs a use for its owner. Indeed, if it did not perform such a use, it would not be kept in his cash balance. Its uses are based precisely on the fact that the individual is not certain on what he will spend his money or of the precise time that he will spend it in the future.

Economists have attempted mechanically to reduce the demand for money to various sources.7 There is no such mechanical determination, however. Each individual decides for himself by his own standards his whole demand for cash balances, and we can only trace various influences which different catallactic events may have had on demand.

- 7J.M. Keynes’ Treatise on Money (New York: Harcourt, Brace, 1930) is a classic example of this type of analysis.

B. Speculative Demand

B. Speculative Demand

One of the most obvious influences on the demand for money is expectation of future changes in the exchange-value of money. Thus, suppose that, at a certain point in the future, the PPM of money is expected to drop rapidly. How the demand-for-money schedule now reacts depends on the number of people who hold this expectation and the strength with which they hold it. It also depends on the distance in the future at which the change is expected to take place. The further away in time any economic event, the more its impact will be discounted in the present by the interest rate. Whatever the degree of impact, however, an expected future fall in the PPM will tend to lower the PPM now. For an expected fall in the PPM means that present units of money are worth more than they will be in the future, in which case there will be a fall in the demand-for-money schedule as people tend to spend more money now than at the future date. A general expectation of an imminent fall in the PPM will lower the demand schedule for money now and thus tend to bring about the fall at the present moment.

Conversely, an expectation of a rise in the PPM in the near future will tend to raise the demand-for-money schedule as people decide to “hoard” (add money to their cash balance) in expectation of a future rise in the exchange-value of a unit of their money. The result will be a present rise in the PPM.

An expected fall in the PPM in the future will therefore lower the PPM now, and an expected rise will lead to a rise now. The speculative demand for money functions in the same manner as the speculative demand for any good. An anticipation of a future point speeds the adjustment of the economy toward that future point. Just as the speculative demand for a good speeded adjustment to an equilibrium position, so the anticipation of a change in the PPM speeds the market adjustment toward that position. Just as in the case of any good, furthermore, errors in this speculative anticipation are “self-correcting.” Many writers believe that in the case of money there is no such self-correction. They assert that while there may be a “real” or underlying demand for goods, money is not consumed and therefore has no such underlying demand. The PPM and the demand for money, they declare, can be explained only as a perpetual and rather meaningless cat-and-mouse race in which everyone is simply trying to anticipate everyone else’s anticipations.

There is, however, a “real” or underlying demand for money. Money may not be physically consumed, but it is used, and therefore it has utility in a cash balance. Such utility amounts to more than speculation on a rise in the PPM. This is demonstrated by the fact that people do hold cash even when they anticipate a fall in the PPM. Such holdings may be reduced, but they still exist, and as we have seen, this must be so in an uncertain world. In fact, without willingness to hold cash, there could be no monetary-exchange economy whatever.

The speculative demand therefore anticipates the underlying nonspeculative demands, whatever their source or inspiration. Suppose, then, that there is a general anticipation of a rise in the PPM (a fall in prices) not reflected in underlying supply and demand. It is true that, at first, this general anticipation raises, ceteris paribus, the demand for money and the PPM. But this situation does not last. For now that a pseudo “equilibrium” has been reached, the speculative anticipators, who did not “really” have an increased demand for money, sell their money (buy goods) to reap their gains. But this means that the underlying demand comes to the fore, and this is less than the money stock at that PPM. The pressure of spending then lowers the PPM again to the true equilibrium point. This may be diagramed as in Figure 77.

Money stock is 0S; the true or underlying money demand is DD, with true equilibrium point at A. Now suppose that the people on the market erroneously anticipate that true demand will be such in the near future that the PPM will be raised to 0E. The total demand curve for money then shifts to DsDs, the new total demand curve including the speculative demand. The PPM does shift to 0E as predicted. But now the speculators move to cash in their gain, since their true demand for money really reflects DD rather than DsDs. At the new price 0E, there is in fact an excess of money stock over quantity demanded, amounting to CF. Sellers rush to sell their stock of money and buy goods, and the PPM falls again to equilibrium. Hence, in the field of money as well as in that of specific goods, speculative anticipations are self-correcting, not “self-fulfilling.” They speed the market process of adjustment.

C. Secular Influences on the Demand for Money

C. Secular Influences on the Demand for Money

Long-run influences on the demand for money in a progressing economy will tend to be manifold, and in both directions. On the one hand, an advancing economy provides ever more occasions for new exchanges as more and more commodities are offered on the market and as the number of stages of production increases. These greater opportunities tend greatly to increase the demand-for-money schedule. If an economy deteriorates, fewer opportunities for exchange exist, and the demand for money from this source will fall.

The major long-run factor counteracting this tendency and tending toward a fall in the demand for money is the growth of the clearing system.8 Clearing is a device by which money is economized and performs the function of a medium of exchange without being physically present in the exchange.

A simplified form of clearing may occur between two people. For example, A may buy a watch from B for three gold ounces; at the same time, B buys a pair of shoes from A for one gold ounce. Instead of two transfers of money being made, and a total of four gold ounces changing hands, they decide to perform a clearing operation. A pays B two ounces of money, and they exchange the watch and the shoes. Thus, when a clearing is made, and only the net amount of money is actually transferred, all parties can engage in the same transactions at the same prices, but using far less cash. Their demand for cash tends to fall.

There is obviously little scope for clearing, however, as long as all transactions are cash transactions. For then people have to exchange one another’s goods at the same time. But the scope for clearing is vastly increased when credit transactions come into play. These credits may be quite short-term. Thus, suppose that A and B deal with each other quite frequently during a year or a month. Suppose they agree not to pay each other immediately in cash, but to give each other credit until the end of each month. Then B may buy shoes from A on one day, and A may buy a watch from B on another. At the end of the period, the debts are canceled and cleared, and the net debtor pays one lump sum to the net creditor.

Once credit enters the picture, the clearing system can be extended to as many individuals as find it convenient. The more people engage in clearing operations (often in places called “clearinghouses”) the more cancellations there will be, and the more money will be economized. At the end of the week, for example, there may be five people engaged in clearing, and A may owe B ten ounces, B owe C ten ounces, C owe D, etc., and finally E may owe A ten ounces. In such a case, 50 ounces’ worth of debt transactions and potential cash transactions are settled without a single ounce of cash being used.

Clearing, then, is a process of reciprocal cancellations of money debts. It permits a huge quantity of monetary exchanges without actual possession and transfer of money, thereby greatly reducing the demand for money. Clearing, however, cannot be all-encompassing, for there must be some physical money which could be used to settle the transaction, and there must be physical money to settle when there is no 100-percent cancellation (which rarely occurs).

- 8On the clearing system, see Mises, Theory of Money and Credit, pp. 281–86.

D. Demand for Money Unlimited?

D. Demand for Money Unlimited?

A popular fallacy rejects the concept of “demand for money” because it is allegedly always unlimited. This idea misconceives the very nature of demand and confuses money with wealth or income. It is based on the notion that “people want as much money as they can get.” In the first place, this is true for all goods. People would like to have far more goods than they can procure now. But demand on the market does not refer to all possible entries on people’s value scales; it refers to effective demand, to desires made effective by being “demanded,” i.e., by the fact that something else is “supplied” for it. Or else it is reservation demand, which takes the form of holding back the good from being sold. Clearly, effective demand for money is not and cannot be unlimited; it is limited by the appraised value of the goods a person can sell in exchange and by the amount of that money which the individual wants to spend on goods rather than keep in his cash balance.

Furthermore, it is, of course, not “money” per se that he wants and demands, but money for its purchasing power, or “real” money, money in some way expressed in terms of what it will purchase. (This purchasing power of money, as we shall see below, cannot be measured.) More money does him no good if its purchasing power for goods is correspondingly diluted.

E. The PPM and the Rate of Interest

E. The PPM and the Rate of Interest

We have been discussing money, and shall continue to do so in the current section, by comparing equilibrium positions, and not yet by tracing step by step how the change from one position to another comes about. We shall soon see that in the case of the price of money, as contrasted with all other prices, the very path toward equilibrium necessarily introduces changes that will change the equilibrium point. This will have important theoretical consequences. We may still talk, however, as if money is “neutral,” i.e., does not lead to such changes, because this assumption is perfectly competent to deal with the problems analyzed so far. This is true, in essence, because we are able to use a general concept of the “purchasing power of money” without trying to define it concretely in terms of specific arrays of goods. Since the concept of the PPM is relevant and important even though its specific content changes and cannot be measured, we are justified in assuming that money is neutral as long as we do not need a more precise concept of the PPM.

We have seen how changes in the money relation change the PPM. In the determination of the interest rate, we must now modify our earlier discussion in chapter 6 to take account of allocating one’s money stock by adding to or subtracting from one’s cash balance. A man may allocate his money to consumption, investment, or addition to his cash balance. His time preferences govern the proportion which an individual devotes to present and to future goods, i.e., to consumption and to investment. Now suppose a man’s demand-for-money schedule increases, and he therefore decides to allocate a proportion of his money income to increasing his cash balance. There is no reason to suppose that this increase affects the consumption/investment proportion at all. It could, but if so, it would mean a change in his time preference schedule as well as in his demand for money.

If the demand for money increases, there is no reason why a change in the demand for money should affect the interest rate one iota. There is no necessity at all for an increase in the demand for money to raise the interest rate, or a decline to lower it—no more than the opposite. In fact, there is no causal connection between the two; one is determined by the valuations for money, and the other by valuations for time preference.

Let us return to the section in chapter 6 on Time Preference and the Individual’s Money Stock. Did we not see there that an increase in an individual’s money stock lowers the effective time-preference rate along the time-preference schedule, and conversely that a decrease raises the time-preference rate? Why does this not apply here? Simply because we were dealing with each individual’s money stock and assuming that the “real” exchange-value of each unit of money remained the same. His time-preference schedule relates to “real” monetary units, not simply to money itself. If the social stock of money changes or if the demand for money changes, the objective exchange-value of a monetary unit (the PPM) will change also. If the PPM falls, then more money in the hands of an individual may not necessarily lower the time-preference rate on his schedule, for the more money may only just compensate him for the fall in the PPM, and his “real money stock” may therefore be the same as before. This again demonstrates that the money relation is neutral to time preference and the pure rate of interest.

An increased demand for money, then, tends to lower prices all around without changing time preference or the pure rate of interest Thus, suppose total social income is 100, with 70 allocated to investment and 30 to consumption. The demand for money increases, so that people decide to hoard a total of 20. Expenditure will now be 80 instead of 100, 20 being added to cash balances. Income in the next period will be only 80, since expenditures in one period result in the identical income to be allocated to the next period.9 If time preferences remain the same, then the proportion of investment to consumption in the society will remain roughly the same, i.e., 56 invested and 24 consumed. Prices and nominal money values and incomes fall all along the line, and we are left with the same capital structure, the same real income, the same interest rate, etc. The only things that have changed are nominal prices, which have fallen, and the proportion of total cash balances to money income, which has increased.

A decreased demand for money will have the reverse effect. Dishoarding will raise expenditure, raise prices, and, ceteris paribus, maintain the real income and capital structure intact. The only other change is a lower proportion of cash balances to money income.

The only necessary result, then, of a change in the demand-for-money schedule is precisely a change in the same direction of the proportion of total cash balances to total money income and in the real value of cash balances. Given the stock of money, an increased scramble for cash will simply lower money incomes until the desired increase in real cash balances has been attained.

If the demand for money falls, the reverse movement occurs. The desire to reduce cash balances causes an increase in money income. Total cash remains the same, but its proportion to incomes, as well as its real value, declines.10

- 9Since no one can receive a money income unless someone else makes a money expenditure on his services. (See chapter 3 above.)

- 10Strictly, the ceteris paribus condition will tend to be violated. An increased demand for money tends to lower money prices and will therefore lower money costs of gold mining. This will stimulate gold mining production until the interest return on mining is again the same as in other industries. Thus, the increased demand for money will also call forth new money to meet the demand. A decreased demand for money will raise money costs of gold mining and at least lower the rate of new production. It will not actually decrease the total money stock unless the new production rate falls below the wear-and-tear rate. Cf. Jacques Rueff, “The Fallacies of Lord Keynes’ General Theory” in Henry Hazlitt, ed., The Critics of Keynesian Economics (Princeton, N.J.: D. Van Nostrand, 1960), pp. 238–63.

F. Hoarding and the Keynesian System

F. Hoarding and the Keynesian System

(1) Social Income, Expenditures, and Unemployment

(1) Social Income, Expenditures, and Unemployment

To the great bulk of writers “hoarding”—an increase in the demand for money—has appeared an unmitigated catastrophe. The very word “hoarding” is a most inappropriate one to use in economics, since it is laden with connotations of vicious antisocial action. But there is nothing at all antisocial about either “hoarding” or “dishoarding.” “Hoarding” is simply an increase in the demand for money, and the result of this change in valuations is that people get what they desire, i.e., an increase in the real value of their cash balances and of the monetary unit.11 Conversely, if the people desire a lowering of their real cash balances or in the value of the monetary unit, they may accomplish this through “dishoarding.” No other significant economic relation—real income, capital structure, etc.—need be changed at all. The process of hoarding and dishoarding, then, simply means that people want something, either an increase or a decrease in their real cash balances or in the real value of the monetary unit, and that they are able to obtain this result. What is wrong with that? We see here simply another manifestation of consumers’ or individuals’ “sovereignty” on the free market.

Furthermore, there is no theoretical way of defining “hoarding” beyond a simple addition to one’s cash balance in a certain period of time. Yet most writers use the term in a normative fashion, implying that there is some vague standard below which a cash balance is legitimate and above which it is antisocial and vicious. But any quantitative limit set on the demand-for-money schedule would be completely arbitrary and unwarranted.

One of the two major pillars of the Keynesian system (now happily beginning to wane after sweeping the economic world in the 1930’s and 1940’s) is the proclamation that savings become equal to investment only through the terrible route of a decline in social income. The (implicit) foundation of Keynesianism is the assertion that at a certain level of total social income, total social expenditures out of this income will be lower than income, the remainder going into hoards. This will lower total social income in the next period of time, since, as we have seen, total income in one “day” equals, and is determined by, total expenditures in the previous “day.”

The Keynesian “consumption function” plays its part in establishing an alleged law that there exists a certain level of total income, say A, above which expenditures will be less than income (net hoarding), and below which expenditures will be greater than income (net dishoarding). But the basic Keynesian worry is hoarding, when total income must decline. This situation may be diagramed as in Figure 78.

In this graph, money income is plotted on both the horizontal and the vertical axes. Hence, a 45-degree straight line between the axes is equal to social income.12 To illustrate: A social income of 100 on the horizontal axis will correspond to, and equal, a social income of 100 on the vertical axis.

The coordinates of these figures will meet at a point equidistant between the two axes. The Keynesian law asserts social expenditures to be lower than social income above point A, and higher than social income below point A, so that A will be the equilibrium point for social income to equal expenditure. For if social income is higher than A, social expenditures will be lower than income, and income will therefore tend to decline from one day to the next until the equilibrium point A is reached. If social income is lower than A, dishoarding will occur, expenditures will be higher than income, until finally A is reached again.

Below, we shall investigate the validity of this alleged law and the “consumption function” on which it rests. But suppose that we now grant the validity of such a law; the only comment can be an impertinent: So what? What if there is a fall in the national income? Since the fall need only be in money terms, and real income, real capital, etc., may remain the same, why any alarm? The only change is that the hoarders have accomplished their objective of increasing their real cash balances and increasing the real value of the monetary unit. It is true that the picture is rather more complex for the transition process until equilibrium is reached, and this will be treated further below (although our final conclusion will be the same). But the Keynesian system attempts to establish the perniciousness of the equilibrium position, and this it cannot do.

Therefore, the elaborate attempts of the Keynesians to demonstrate that free-market expenditures will be limited—that consumption is limited by the “function,” and investment by stagnation of opportunities and “liquidity preference”—are futile. For even if they were correct (which they are not), the result would be pointless. There is nothing wrong with hoarding or dishoarding, or with “low” or “high” levels (whatever that may mean) of social money income.

The Keynesian attempt to salvage meaning for their doctrine rests on one point and one point alone—the second major pillar of their system. This is the thesis that money social income and level of employment are correlated, and that the latter is a function of the former. This assumes that a certain “full employment” level of social income exists below which there is correspondingly greater unemployment. This can be diagramed as in Figure 79.

On the previous diagram is superimposed a vertical FF line, which represents the point of alleged “full-employment” social income. If the intersection A is below (to the left of) the FF line, then there is permanent unemployment corresponding to the distance by which A falls short of that line.

Keynesians have also attempted, with little success, to give meaning to an equilibrium position where A falls to the right of the FF line, identifying this with inflation. Inflation, as we shall see below, is a dynamic process, the essence of which is change. The Keynesian system centers around the equilibrium position and therefore is hardly well equipped to analyze an inflationary situation.

The nub of the Keynesian critique of the free market economy, then, rests on the involuntary unemployment allegedly caused by too low a level of social expenditures and income. But how can this be, since we have previously explained that there can be no involuntary unemployment in a free market? The answer has become evident (and is admitted in the most intelligent of the Keynesian writings): The Keynesian “underemployment equilibrium” occurs only if money wage rates are rigid downward, i.e., if the supply curve of labor below “full employment” is infinitely elastic.13 Thus, suppose there is a “hoarding” (an increased demand for money), and social income falls. The result is a fall in the monetary demand curves for labor factors, as well as in all other monetary demand curves. We would expect the general supply curve of labor factors to be vertical. Since only money wage rates are being changed while real wage rates (in terms of purchasing power) remain the same, there will be no shift in labor/leisure preferences, and the total stock of labor offered on the market will remain constant. At any rate, certainly no involuntary unemployment will arise.

How then can the Keynesian case arise? How can the supply of labor remain horizontal at the old money wage rate? In only two ways: (1) if people voluntarily agree with the unions, which insist that no one be employed at lower than the old money wage rate. Since selling prices are falling, maintaining the old money wage rate is equivalent to demanding a higher real wage rate. We have seen above that the unions’ raising of real wage rates causes unemployment. But this unemployment is voluntary, since the workers acquiesce in the imposition of a higher minimum real wage rate, below which they will not undercut the union and accept employment. Or (2) unions or government coercively impose the minimum wage rate. But this is an example of a hampered market, not the free market to which we are confining our analysis here.

Situation (1) or (2) may be diagramed as in Figure 80.

The original demand curve for labor is DD (for simplicity of exposition we assume as meaningful the concept of “demand for labor” in general). Total stock of labor in the society is 0F, or at least that is the stock put forward upon the market. Now an increase in the demand for money shifts all demand curves downward as all money prices fall. If wage rates are free to fall, the intersection point will move from H to C and nominal wage rates reduced accordingly, from FH to FC.

There is still “full employment” at level 0F. Now suppose however, that a union sets a minimum money wage rate of 0B (or FH). Then the supply-of-labor curve becomes BHG; horizontal up to FG and vertical from there on. The new demand curve D′D′ will now intersect the supply of labor at point E instead of point C. Total amount of labor now employed is reduced to BE, and EH are now unemployed as a result of the union action.

Keynes’ own exposition tended to run in terms of real rather than money magnitudes—real social income, real expenditures, etc.14 Such an analysis obscures dynamic considerations, since transactions take place at least superficially in monetary terms on the market. However, the essential conclusion of our analysis remains unchanged if we pursue it directly in real terms. Instead of falling, demand curves in real terms will now remain the same. This is true for the labor market as well. Instead of being depicted on a diagram as a horizontal line at existing wage rates, the effect of union action would have to be shown as a horizontally imposed increase in real wage rates (the result of keeping money wage rates constant while selling prices fall). The relevant diagram is shown in Figure 81. The facts depicted in this diagram are the same as in the previous diagram: unions causing unemployment (EH) by insisting on an excessively high money (and therefore real) wage (0B).

The sum and substance of the “Keynesian Revolution” was the thesis that there can be an unemployment equilibrium on the free market. As we have seen, the only sense in which this is true was known years before Keynes: that widespread union maintenance of excessively high wage rates will cause unemployment.

Keynes believed that while other elements of the economic system, including prices, were set basically in real terms, workers bargained even ultimately only in terms of money wages—that unions insisted on minimum money wage rates downward, but would passively accept falling real wages in the form of rising prices, money wage rates remaining the same. The Keynesian prescription for eliminating unemployment therefore rests specifically on the “money illusion”—that unions will impose minimum money wage rates, but are too stupid to impose minimum real wage rates per se. Unions, however, have learned about purchasing-power problems and the distinction between money and real rates; indeed, it hardly requires much reasoning ability to grasp this distinction.15 Ironically, Keynes’ advocacy of inflation based on the “money illusion” rested on the historical experience (which we shall treat more fully below) that, during an inflation, selling prices rise faster than wage rates. Yet an economy in which unions impose minimum wage rates is precisely an economy in which unions will be alive to any losses in their real, as well as their money, wages. Inflation, therefore, cannot be used as a means of duping unions into relieving unemployment.16 Keynesianism has been touted as at least a “practical” system. Whatever its theoretical defects, it is alleged to be fit for the modern world of unionism. Yet it is precisely in the modern world that Keynes’ doctrine is least appropriate or practical.17

The Keynesians object that to allow rigid money wage rates to become flexible downward would further lower monetary demand for goods, and therefore monetary income. But this completely confuses wage rates with aggregate payroll, or total income going to wages.18 That the former falls does not mean that the latter falls. On the contrary, total income is, as we have seen, determined by total expenditures in the previous period of time. Lower wage rates will cause the hiring of those made unemployed by the old excessively high wage rates. The fact that labor is now cheaper relatively to land factors will cause investors to expend a greater proportion on labor visà-vis land than before. And the employment of unemployed labor increases production and therefore aggregate real income. Furthermore, even if payrolls also decline, prices and wage rates can adjust—but this will be taken up in the next section on liquidity preference.

- 11See the excellent article by W.H. Hutt, “The Significance of Price Flexibility” in Hazlitt, Critics of Keynseian Economics, pp. 383–406.

- 12The term generally used is “national” income. However, in a free-market economy the nation will no more be an important economic boundary than the village or region. It is more convenient, then, to set aside regional problems for other analysis and to concentrate on aggregate social income; this is especially true since regions do not present a problem to economic theory until their governments begin intervening in the free market.

- 13Thus, see the revealing article by Franco Modigliani, “Liquidity Preference and the Theory of Interest and Money” in Hazlitt, Critics of Keynesian Economics, pp. 156–69. Also see the articles by Erik Lindahl, “On Keynes’ Economic System—Part I,” The Economic Record, May, 1954, pp. 19–32; November, 1954, pp. 159–71; and Wassily W. Leontief, “Postulates: Keynes’ General Theory and the Classicists” in S. Harris, ed., The New Economics (New York: Knopf, 1952), pp. 232–42. For an empirical critique of the assumed Keynesian correspondence between aggregate output and employment, see George W. Wilson, “The Relationship between Output and Employment,” Review of Economics and Statistics, February, 1960, pp. 37–43.

- 14This is what Keynes’ discussion of “wage units” amounted to. Cf. Lindahl, “On Keynes’ Economic System—Part I,” p. 20.

- 15Cf. Lindahl, “On Keynes’ Economic System—Part I,” pp. 25, 159ff. Lindahl’s articles provide a good summary as well as a critique of the Keynesian system.

- 16Furthermore, inflation is, at best, an inefficient and distortive substitute for flexible wage rates. For inflation affects the entire economy and its prices, while particular wage rates will fall only to the extent necessary to “clear” the market for the particular labor factor. Thus, freely flexible wage rates will fall only in those fields necessary to eliminate unemployment in those particular areas. Cf. Henry Hazlitt, The Failure of the “New Economics” (Princeton, N.J.: D. Van Nostrand, 1959), pp. 278 ff.

- 17Cf. L. Albert Hahn, The Economics of Illusion (New York: Squier Publishing Co., 1949), pp. 50 ff., 166 ff., and passim.

(2) “Liquidity Preference”

(2) “Liquidity Preference”

Those Keynesians who recognize the grave difficulties of their system fall back on one last string in their bow—”liquidity preference.” Intelligent Keynesians will concede that involuntary unemployment is a “special” or rare case, and Lindahl goes even further to say that it could be only a short-run and not a long-run equilibrium phenomenon.19 Neither Modigliani nor Lindahl, however, is thoroughgoing enough in his critique of the Keynesian system, particularly of the “liquidity preference” doctrine.

The Keynesian system, as is quite clear from the mathematical portrayals of it given by its followers, suffers grievously from the mathematical-economic sin of “mutual determination.” The use of mathematical functions, which are reversible at will, is appropriate in physics, where we do not know the causes of the observed movements. Since we do not know the causes, any mathematical law explaining or describing movements will be reversible, and, as far as we are concerned, any of the variables in the function is just as much “cause” as another. In praxeology, the science of human action, however, we know the original cause—motivated action by individuals. This knowledge provides us with true axioms. From these axioms, true laws are deduced. They are deduced step by step in a logical, cause-and-effect relationship. Since first causes are known, their consequent effects are also known. Economics therefore traces unilinear cause-and-effect relations, not vague “mutually determining” relations.

This methodological reminder is singularly applicable to the Keynesian theory of interest. For the Keynesians consider the rate of interest (a) as determining investment and (b) as being determined by the demand for money to hold “for speculative purposes” (liquidity preference). In practice, however, they treat the latter not as determining the rate of interest, but as being determined by it. The methodology of “mutual determination” has completely obscured this sleight of hand. Keynesians might object that all demand and supply curves are “mutually determining” in their relation to price. But this facile assertion is not correct. Demand curves are determined by utility scales, and supply curves by speculation and the stock produced by given labor and land factors, which is ultimately governed by time preferences.

The Keynesians therefore treat the rate of interest, not as they believe they do—as determined by liquidity preference—but rather as some sort of mysterious and unexplained force imposing itself on the other elements of the economic system. Thus, Keynesian discussion of liquidity preference centers around “inducement to hold cash” as the rate of interest rises or falls. According to the theory of liquidity preference, a fall in the rate of interest increases the quantity of cash demanded for “speculative purposes” (liquidity preferences), and a rise in the rate of interest lowers liquidity preference.

The first error in this concept is the arbitrary separation of the demand for money into two separate parts: a “transactions demand,” supposedly determined by the size of social income, and a “speculative demand,” determined by the rate of interest. We have seen that all sorts of influences impinge themselves on the demand for money. But they are only influences working through the value scales of individuals. And there is only one final demand for money, because each individual has only one value scale. There is no way by which we can split the demand up into two parts and speak of them as independent entities. Furthermore, there are far more than two influences on demand. In the final analysis, the demand for money, like all utilities, cannot be reduced to simple determinants; it is the outcome of free, independent decisions on individual value scales. There is, therefore, no “transaction demand” uniquely determined by the size of income.

The “speculative demand” is mysterious indeed. Modigliani explains this “liquidity preference” as follows:

we should expect that any fall in the rate of interest ... would induce a growing number of potential investors to keep their assets in the form of money, rather than securities; that is to say, we should expect a fall in the rate of interest to increase the demand for money as an asset.20

This is subject to the criticism, as we have seen, that the rate of interest is here determining, and is not itself explained by any cause. Furthermore, what does this statement mean? A fall in the rate of interest, according to the Keynesians, means that less interest is being earned from bonds, and therefore there is a greater inducement to hold cash. This is correct (as long as we allow ourselves to think in terms of the interest rate as determining instead of being determined), but highly inadequate. For if a lower interest rate “induces” greater cash holdings, it also induces greater consumption, since consumption also becomes more attractive. In fact, one of the grave defects of the liquidity-preference approach is that the Keynesians never think in terms of three “margins” being decided at once. They think only in terms of two at a time. Hence, Modigliani: “Having made his consumption-saving plan, the individual has to make decisions concerning the assets he owns”; i.e., he then allocates them between money and securities.21 In other words, people first decide between consumption and saving (in the sense of not consuming); and then they decide between investing and hoarding these savings. But this is an absurdly artificial construction. People decide on all three of their alternatives, weighing one against each of the others. To say that people first decide between consuming and not consuming and then choose between hoarding and investing is just as misleading as to say that people first choose how much to hoard and then decide between consumption and investment.22

People, therefore, allocate their money among consumption, investment, and hoarding. The proportion between consumption and investment reflects individual time preferences. Consumption reflects desires for present goods, and investment reflects desires for future goods. An increase in the demand-for-money schedule does not affect the rate of interest if the proportion between consumption and investment (i.e., time preference) remains the same.

The rate of interest, we must reiterate, is determined by time preferences, which also determine the proportions of consumption and investment. To think of the rate of interest as “inducing” more or less saving or hoarding is to misunderstand the problem completely.23

Admitting, then, that time preference determines the proportions of consumption and investment and that the demand for money determines the proportion of income hoarded, does the demand for money play a role in determining the interest rate? The Keynesians assert that there is a relation between the rate of interest and a “speculative” demand for cash. Should the schedule of the latter rise, the former rises also. But this is not necessarily true. A greater proportion of funds hoarded can be drawn from three alternative sources: (a) from funds that formerly went into consumption, (b) from funds that went into investment, and (c) from a mixture of both that leaves the old consumption-investment proportion unchanged. Condition (a) will bring about a fall in the rate of interest; condition (b) a rise in the rate of interest, and condition (c) will leave the rate of interest unchanged. Thus hoarding may reflect either a rise, a fall, or no change in the rate of interest, depending on whether time preferences have concomitantly risen, fallen, or remained the same.

The Keynesians contend that the speculative demand for cash depends upon and determines the rate of interest in this way: if people expect that the rate of interest will rise in the near future, then their liquidity preference increases to await this rise. This, however, can hardly be a part of a long-run equilibrium theory, such as Keynes is trying to establish. Speculation, by its very nature, disappears in the ERE, and hence no fundamental causal theory can be based upon it. Furthermore, what is an interest rate? One grave and fundamental Keynesian error is to persist in regarding the interest rate as a contract rate on loans, instead of the price spreads between stages of production. The former, as we have seen, is only the reflection of the latter. A strong expectation of a rapid rise in interest rate means a strong expectation of an increase in the price spreads, or rate of net return. A fall in prices means that entrepreneurs generally expect that factor prices will fall further in the near future than their selling prices. But it requires no Keynesian labyrinth to explain this phenomenon; all we are confronted with is a situation in which entrepreneurs, expecting that factor prices will soon fall, cease investing and wait for this happy event so that their return will be greater. This is not “liquidity preference,” but speculation on price changes. It involves a modification of our previous discussion of the relation between prices and the demand for money, caused by a fact that we shall explore soon in detail, namely, that prices do not change equally and proportionately.

The expectation of falling factor prices speeds up the movement toward equilibrium and hence toward the pure interest relation as determined by time preference.24

If, for example, unions keep wage rates artificially high, “hoarding” will increase as unions keep wage rates ever higher than the equilibrium rate at which “full employment” can be maintained. This induced hoarding lowers the money demand for factors and increases unemployment still further, but only because of wage-rate rigidity.25

The final Keynesian bogey is that people may acquire an unlimited demand for money, so that hoards will indefinitely increase. This is termed an “infinite” liquidity preference. And this is the only case in which neo-Keynesians such as Modigliani believe that involuntary unemployment can be compatible with price and wage freedom. The Keynesian worry is that people will hoard instead of buying bonds for fear of a fall in the price of securities. Translating this into more important “natural” terms, this would mean, as we have stated, not investing because of expectation of imminent increases in the natural interest rate. Rather than act as a blockade, however, this expectation speeds the ensuing adjustment. Furthermore, the demand for money could not be infinite since people must always continue consuming, whatever their expectations. Of necessity, therefore, the demand for money could never be infinite. The existing level of consumption, in turn, will require a certain level of investment. As long as productive activities are continuing, there is no need or possibility of lasting unemployment, regardless of the degree of hoarding.26

A demand for money to hold stems from the general uncertainty of the market. Keynesians, however, attribute liquidity preference, not to general uncertainty, but to the specific uncertainty of future bond prices. Surely this is a highly superficial and limiting view.

In the first place, this cause of liquidity preference could occur only on a highly imperfect securities market. As Lachmann pointed out years ago in a neglected article, Keynes’ causal pattern—“bearishness” causing “liquidity preference” (demand for cash) and high interest rates—could take place only in the absence of an organized forward or futures market for securities.

If such a market existed, both bears and bulls on the bond market

could express their expectations by forward transactions which do not require any cash. Where the market for securities is fully organized over time, the owner of 4% bonds who fears a rise in the rate of interest has no incentive to exchange them for cash, for he can always “hedge” by selling them forward.27

Bearishness would cause a fall in forward bond prices, followed immediately by a fall in spot prices. Thus, speculative bearishness would, of course, cause at least a temporary rise in the rate of interest, but accompanied by no increase in the demand for cash. Hence, any attempted connection between liquidity preference, or demand for cash, and the rate of interest, falls to the ground.

The fact that such a securities market has not been organized indicates that traders are not nearly as worried about rising interest rates as Keynes believes. If they were and this fear loomed as an important phenomenon, then surely a futures market would have developed in securities.

Furthermore, as we have seen, interest rates on loans are merely a reflection of price spreads, so that a prediction of higher interest rates really means the expectation of lower prices and, especially, lower costs, resulting in a greater demand for money. And all speculation, on the free market, is self-correcting and speeds adjustment, rather than a cause of economic trouble.

- 19Cf. Lindahl’s critique of Lawrence Klein’s The Keynesian Revolution in “On Keynes’ Economic System—Part I,” p. 162. Also see Leontief, “Postulates: Keynes’ General Theory and the Classicists.”

- 20Modigliani, “Liquidity Preference and the Theory of Interest and Money,” pp. 139–40.

- 21Ibid., p. 137.

- 22See the critique of the Keynesian doctrine by Tjardus Greidanus, The Value of Money (2nd ed.; London: Staples Press, 1950), pp. 194–215, and of the liquidity-preference theory by D.H. Robertson, “Mr. Keynes and the Rate of Interest” in Readings in the Theory of Income Distribution, pp. 439–41. In contrast to Keynes’ famous phrase that the rate of interest is “the reward for parting with liquidity,” Greidanus points out that buying consumers’ goods (or even producers’ goods in Keynes’ sense of “interest”) sacrifices liquidity and yet earns no interest “reward.” Greidanus, Value of Money, p. 211. Also see Hazlitt, Failure of the “New Economics,” pp. 186 ff.

- 23Mises, Human Action, pp. 529–30.

- 24Hutt concludes that equilibrium

is secured when all services and products are so priced that they are (i) brought within the reach of people’s pockets (i.e., so that they are purchasable by existing money incomes) or (ii) brought into such a relation to predicted prices that no postponement of expenditure on them is induced. For instance, the products and services used in the manufacture of investment goods must be so priced that anticipated future money incomes will be able to buy the services and depreciation of new equipment or replacement. (Hutt, “Significance of Price Flexibility,” p. 394) - 25“Postponements (in purchases) arise because it is judged that a cut in costs (or other prices) is less than will eventually have to take place, or because the rate of fall of costs is insufficiently rapid.” Ibid., p. 395.

- 26As Hutt points out, if we can conceive of a situation of infinitely elastic liquidity preference (and no such situation has ever existed), then “we can conceive of prices falling rapidly, keeping pace with expectations of price changes, but never reaching zero, with full utilization of resources persisting all the way.” Ibid., p. 398.

- 27L.M. Lachmann, “Uncertainty and Liquidity Preference,” Economica, August, 1937, p. 301.

G. The Purchasing-Power and Terms-of-Trade Compenents in the Rate of Interest

G. The Purchasing-Power and Terms-of-Trade Compenents in the Rate of Interest

Many economists, beginning with Irving Fisher, have asserted that the market rate of interest, in addition to containing specific entrepreneurial components superimposed on the pure rate of interest, also contains a “price” or a “purchasing-power component.” When the purchasing power of money is generally expected to rise, the theory asserts that the market rate of interest falls correspondingly; when the PPM is expected to fall, the theory declares that the market rate of interest rises correspondingly.

These economists erred by concentrating on the loan rate rather than on the natural rate (the rate of return). The reasoning behind this theory was as follows: If the purchasing power of money is expected to change, then the pure rate of interest (determined by time preference) will no longer be the same in “real terms.” Suppose that 100 gold ounces exchange for 105 gold ounces a year from now—i.e., that the rate of interest is 5 percent. Now, suddenly, let there be a general expectation that the purchasing power of money will increase. In that case, a lower amount to be returned, say 102 ounces, may yield 5 percent real interest in terms of purchasing power. A general expectation of a rise in purchasing power, therefore, will lower the market rate of interest at present, while a general expectation of a fall in purchasing power will raise the rate.28

There is a fatal defect in this generally accepted line of reasoning. Suppose, for example, that prices are generally expected to fall by 50 percent in the next year. Would someone lend 100 gold ounces to exchange for 53 ounces one year from now? Why not? This would certainly preserve the real interest rate at 5 percent. But then why should the would-be lenders not simply hold on to their money and double their real assets as a result of the price fall? And that is precisely what they would do; they certainly would not give money away, even though their real assets would be greater than before. Fisher simply shrugged off this point by saying that the purchasing-power premium could never make the interest rate negative. But this flaw vitiates the entire theory.

The root of the difficulty consists in ignoring the natural rate of interest. Let us consider the interest rate in those terms. Then, suppose 100 ounces are paid for factors that will be transformed in one year into a product that sells for 105 gold ounces, for an interest gain of five and an interest return of 5 percent. Now a general expectation arises of a general halving of prices one year from now. The selling price of the product will be 53 ounces in a year’s time. What happens now? Will entrepreneurs buy factors for 100 and sell at 53 merely because their real interest rate is preserved? Certainly not. They will do so only if they do not at all anticipate the change in purchasing power. But to the extent that it is anticipated, they will hold money rather than buy factors. This will immediately lower factor prices to their expected future levels, say from 100 to 50.

What happens to the loan rate is analytically quite trivial. It is simply a reflection of the natural rate and depends on how the expectations and judgment of the people on the loan market compare with those on the stock and other markets. For the free economy, there is no point in separately analyzing the loan market. Analysis of the Fisher problem—the relation of the interest rate to price changes—should concentrate on the natural rate of interest. Discussion of the relation between price movements and the (natural) rate of interest should be divided into two parts: first, assuming “neutral money”—that all prices change equally and at the same time—and second, analyzing conditions where factor and product change at different rates. And these changes should first be analyzed without considering that they had been anticipated by people on the market.

Suppose, first, that all prices change equally and at the same time. Instead of thinking in terms of 100 ounces borrowed on the loan market, let us consider the natural rate. An investor buys factors in period 1 and then sells the product, say in period 3. Time, as we have seen, is the essence of the production structure. All the processes take time, and capitalists pay money to owners of factors in advance of production and sale. Since factors are bought before products are sold, what is the effect of a period of rising general prices (i.e., falling PPM)? The result is that the entrepreneur reaps an apparent extra profit. Suppose that he normally purchases original factors for 100 and then sells the product for 120 ounces two years later, for an interest return of 10 percent per annum. Now suppose that a decrease in the demand for money or an increase of money stock propels a general upward movement in prices and that all prices double in two years’ time. Then, just because of the passage of time, an entrepreneur who purchases factors for 100 now will sell for 240 ounces in two years’ time. Instead of a net return of 20 ounces, or 10 percent per annum, he reaps 140 ounces, or 70 percent per annum.

It would seem that a rise in prices creates an inherent tendency for large-scale profits that are not simply individual rewards for more accurate forecasting. However, more careful analysis reveals that this is not an extra profit at all. For the 240 ounces two years from now is roughly equivalent, in terms of purchasing power, to 120 ounces now. The real rate of net return, based on money’s services, is the same 10 percent as it has always been. It is clear that any lower net return would amount to a decline in real return. A return of a mere 120 ounces, for example, would amount to a drastic negative real return, for 100 ounces would then be invested for the equivalent gross return of only 60 ounces. It has often been shown that a period of rising prices misleads businessmen into thinking that their increased money profits are also real gains, whereas they only maintain real rates of return. Consider, for example, “replacement costs”—the prices which the businessmen will now have to pay for factors. The capitalist who earns 240 ounces on a 100-ounce investment neglects to his sorrow the fact that his factor bundle now costs 200 ounces instead of 100. Businessmen who under such circumstances treat their monetary profits as real profits and consume them soon find that they are really consuming their capital.

The converse occurs in the case of falling prices. The capitalist buys factors in period 1 and sells the product in period 3, when all-around prices are lower. If prices are to fall by a half in two years, an investment of 100, followed by a sale at 60, does not really involve the terrific loss that it appears to be. For the 60 return is equivalent in real terms, both in generalized purchasing power and in replacement of factors, to 120 previous ounces. His real rate of return remains the same. The consequence is that businessmen will be likely to overstate their losses in a period of price contraction. Perhaps this is one of the major reasons for the deep-seated belief of most businessmen that they always gain during a general price expansion and lose during a period of general contraction. This belief is purely illusory.

In these examples, the natural interest rate on the market has contained a purchasing-power component, which corrects for real rates, positively in money terms during a general expansion, and negatively during a general contraction. The loan rate will be simply a reflection of what has been happening in the natural rate. So far, the discussion is similar to Fisher’s, except that these are the effects of actual, not anticipated, changes and the Fisher thesis cannot take account of the negative interest rate case. We have seen that rather than take a monetary loss, even though their real return will be the same, entrepreneurs will hold back their purchases of factors until factor prices fall immediately to their future low level. But this process of anticipatory price movement does not occur only in the extreme case of a prospective “negative” return. It happens whenever a price change is anticipated. Thus, suppose all entrepreneurs generally anticipate that prices will double in two years. The fact of an anticipated rise will lead to an increase in the price level now and an approach immediately toward a doubled price level. An anticipated fall will lead to an immediate fall in factor prices. If all changes were anticipated by everyone, there would be no room for a purchasing-power component to develop. Prices would simply fall immediately to their future level.

The purchasing-power component, then, is not the reflection, as has been thought, of expectations of changes in purchasing power. It is the reflection of the change itself; indeed, if the change were completely anticipated, the purchasing power would change immediately, and there would be no room for a purchasing-power component in the rate of interest. As it is, partial anticipations speed up the adjustment of the PPM to the changed conditions.