It is widely accepted that by means of suitable monetary policies the US central bank can navigate the economy towards a growth path of economic stability and prosperity. The key ingredient in achieving this is price stability.

Most experts are of the view that what prevents the attainment of price stability are the fluctuations of the federal funds rate around the neutral rate of interest. The neutral rate, it is held, is one that is consistent with stable prices and a balanced economy.

In short, what is required is Fed policy makers successfully targeting the federal funds rate towards the neutral interest rate. Once the Fed brings the federal funds rate in line with the neutral interest rate, price stability and thus economic stability can be reached. This framework of thinking, which has its origins in the 18th century writings of the British economist Henry Thornton1 , was articulated in late 19th century by the Swedish economist Knut Wicksell.

In fact, it is safe to suggest that the current framework of central bank operations throughout the world is based to a large degree on Wicksellian writings. Now, if what we are suggesting is correct obviously then the key to understanding the rationale of central banks actions is the writings of Knut Wicksell.

Knut Wicksell's framework for price stability

The central element in Wicksell's framework is the natural interest rate, which Wicksell defined as follows,

There is a certain rate of interest on loans which is neutral in respect to commodity prices, and tend neither to raise nor to lower them. This is necessarily the same as the rate of interest which would be determined by supply and demand if no use were made of money and all lending were effected in the form of real capital goods. It comes to much the same thing to describe it as the current value of the natural rate of interest on capital.2

In other words, the natural rate of interest is defined as the rate at which the demand for physical loan capital coincides with the supply of savings expressed in physical magnitudes.3

To elaborate this point further Wicksell wrote,

For the sake of simplicity it will be assumed that the present owners of the available consumption goods are capitalists; that is to say, that they have no immediate need either for the goods themselves or for such proceeds as they obtain for them in the form of other goods or of money. They are in a position, if necessary, to postpone payment up to a period of, let us say, one year. It may be supposed in theory that the entrepreneur borrows these consumption goods from the capitalists in kind and then pays them out in kind in the shape of wages and rents. At the end of the period of production he repays the loan out of his own product, either directly or after exchanging it for other commodities (relative prices being assumed to remain unaltered). If this procedure were adopted by all entrepreneurs who work with borrowed capital, competition would bring about a certain rate of interest that would have to be paid to the capitalists in the form of some commodity or other. The amount of this rate of interest would be determined by the “supply and demand” for capital.4

In his framework Wicksell makes a clear distinction between the interest rate that is determined in financial markets and the interest rate that is set in the real world without money. Whilst the interest rate in financial markets is determined by demand and supply for money, the natural interest rate is set by real factors. In other words, money has nothing to do with the determination of interest rates in the real world of goods. Thus he wrote,

Now if money is loaned at this same rate of interest, it serves as nothing more than a cloak to cover a procedure which, from the purely formal point of view, could have been carried on equally well without it. The conditions of economic equilibrium are fulfilled in precisely the same manner.5

In the Wicksellian framework money only affects the price level. The effect of money on the price level is however not direct, it operates via the gap between the money market interest rate and the natural rate. The mechanism works as following, if the market rate falls below the natural rate, investment will exceed saving implying that aggregate demand will be greater than aggregate supply.

Assuming that the excess demand is financed by the expansion in bank loans this leads to the creation of new money, which in turn pushes the general level of prices up. Conversely, if the market rate rises above the natural rate, savings will exceed investment, aggregate supply will exceed aggregate demand, bank loans and the stock of money will contract, and prices will fall.6 Hence whenever the market rate is in line with the natural rate the economy is in a state of equilibrium and there are neither upward nor downward pressures on the price level. It is deviations in the money market interest rate from the natural rate that sets in motion changes in the money supply which in turn disturb the general price level. According to Wicksell,

If it were possible to ascertain and specify the current value of the natural rate, it would be seen that any deviation of the actual money rate from this natural rate is connected with rising or falling prices according as the deviation is downward or upward.7

Wicksell held that because the supply of real capital is limited, whereas the supply of money can be regarded as fairly elastic, there is no reason to assume that the money market interest rate would normally agree with the natural real rate.8 Now, if this is the case obviously it calls for some central authority to make sure that these deviations are smoothed out.

Furthermore, Wicksell maintained that to establish whether monetary policy is tight or loose it is not enough to pay attention to the level of money market interest rates, but rather one needs to contrast money market interest rates with the natural rate. Thus if the market interest rate is above the natural rate then the policy stance is tight. Conversely, if the market rate is below the natural rate then the policy stance is loose. Thus,

In the place of attempts to discover whether high prices are accompanied by high or by low rates of interest, it would have been well to elucidate the real meaning of a high or of low rate of interest. It might then have been seen that it is an essentially relative conception, and that a further datum must be supplied, namely, the level of the natural rate, before it is possible to determine whether any particular rate of interest is to be regarded as high or as low.9

The Invisible Nature Rate

However, how is one to implement this framework of thinking? The main problem here is that the natural interest rate can't be observed. How can one tell whether the market interest rate is above or below the natural rate? Wicksell suggested that policy makers pay close attention to changes in the price level. Thus a rising price level would call for an upward adjustment in the money rate, while a falling price level would signal that the money interest rate must be lowered. He wrote,

This does not mean that the banks ought actually to ascertain the natural rate before fixing their own rates of interest. That would, of course, be impracticable, and would also be quite unnecessary. For the current level of commodity prices provides a reliable test of the agreement of diversion of the two rates.

The procedure should rather be simply as follows: So long as prices remain unaltered the banks' rate of interest is to remain unaltered. If prices rise, the rate of interest is to be raised; and if prices fall, the rate of interest is to be lowered; and the rate of interest is henceforth to be maintained at its new level until a further movement of prices calls for a further change in one direction or the other. The more promptly these changes are undertaken the smaller is the possibility of considerable fluctuations of the general level of prices; and the smaller and less frequent will have to be the changes in the rate of interest…..In my opinion, the main cause of the instability of prices resides in the inability or failure of the banks to follow this rule.10

In short, banks should adjust the money market interest rate in the same direction as movements in the price level. Note that this procedure is followed today by all central banks. Thus in response to rises in price indexes above an accepted figure the Fed raises the federal funds rate target. Conversely, when price indexes are growing at a pace considered as too low the Fed lowers the target.

Despite the fact that the natural interest rate cannot be observed modern economists are of the view that it can be estimated by various indirect means. For instance one can establish what it is simply by averaging the value of the real fed funds rate (fed funds rate minus price inflation) over a long period of time.

Some other economists hold that the natural rate fluctuates over time and reject the notion that the natural rate can be approximated by an average figure. In order to extract the unobservable moving natural interest rate economists now employ sophisticated mathematical methods such as the Kalman filter.11

According to this method a researcher partially adjusts the estimate of the natural rate based on how far off the model's prediction of GDP is from actual GDP. If the prediction coincides with the actual GDP then the assumption regarding the natural rate is kept unchanged. If actual GDP is higher than that predicted by the model then it is assumed that this must mean that monetary policy was more stimulative than expected by the researcher, meaning that the assumption about the natural rate is too low. The estimate of the natural rate goes up by an amount proportional to the GDP prediction error. The assumed natural rate is lowered if actual GDP is lower than the prediction of the model.12

But does all of this make much sense?

Are interest rates in financial markets and the real economy distinct phenomena?

The essence of the phenomenon of interest is the cost that the saver of saved money endures. This cost stems from the fact that the saver has given up some benefits at present. On this Mises wrote,

That which is abandoned is called the price paid for the attainment of the end sought. The value of the price paid is called cost. Costs are equal to the value attached to the satisfaction which one must forego in order to attain the end aimed at.13

The fact that the saved dollar incurs a cost to the saver means that the same dollar that is employed to secure goods at present carries a premium over the saved dollar, which will be employed by the saver to secure goods only in the future. According to Carl Menger:

To the extent that the maintenance of our lives depends on the satisfaction of our needs, guaranteeing the satisfaction of earlier needs must necessarily precede attention to later ones. And even where not our lives but merely our continuing well-being (above all our health) is dependent on command of a quantity of goods, the attainment of well-being in a nearer period is, as a rule, a prerequisite of well being in a later period……..All experience teaches that a present enjoyment or one in the near future usually appears more important to men than one of equal intensity at a more remote time in the future.14

Likewise, according to Mises,

Satisfaction of a want in the nearer future is, other things being equal, preferred to that in the farther distant future. Present goods are more valuable than future goods.15

Hence an individual will undertake the act of saving only if the return on the saved dollar will be in excess of the cost of saving. According to Mises,

The postponement of an act of consumption means that the individual prefers the satisfaction which later consumption will provide to the satisfaction which immediate consumption could provide.16

By assigning a higher valuation to the present dollar versus the future dollar on account of the cost incurred by the act of saving an individual therefore expresses a positive time preference.

Would it be possible in a world without money, such as suggested by Wicksell, to establish the rate of return on present goods in terms of future goods? In a world without money all that one would have are the rates of exchanges between various present and future real goods. For instance, one present apple is exchanged for two potatoes in a one-year's time. Or, one shirt is exchanged for three tomatoes in a one-year's time. Again all that we have here are various ratios.

There is, however, no way to establish from these ratios what the rate of return is for one present apple in terms of future potatoes (It is not possible to calculate the percentage since potatoes and apples are not the same goods). Likewise we cannot establish the rate of return on a shirt in terms of future tomatoes. In other words, we can only establish that one present apple is exchanged for two future potatoes, and one present shirt is exchanged for three future tomatoes. Only in the framework of the existence of money can the rate of return be established.

For instance, the time preference of a baker, which is established in accordance with his particular set-up, determines that he will be ready to lend ten dollars - which he has earned by selling ten loaves of bread - for a borrowers promise to repay eleven dollars in a one year's time. Similarly the time preference of a shoemaker, which is formed in accordance with his particular set-up, determines that he will be a willing borrower. In short, once the deal is accomplished both parties to this deal have benefited. The baker will get eleven dollars in one-year's time that he values much more than his present ten dollars. For the shoemaker the value of the present ten dollars exceeds the value of eleven dollars in one-year time.

As one can see here, both money and the real factor (time preferences) are involved in establishing the market interest rate, which is 10%. Note that the baker has exchanged ten loaves of bread for money first (i.e., ten dollars). He then lends the ten-dollars for eleven dollars in one-year's time. The interest rate that he secures for himself is 10%. In one-year's time the baker can decide what goods to purchase with the obtained eleven dollars. As far as the shoemaker is concerned he must generate enough shoes in order to enable him to secure at least eleven dollars to repay the loan to the baker.

Observe however, that without the existence of money – the medium of exchange – the baker isn't able to establish how much of future goods he must be paid for his ten loaves of bread that would comply with the rate of return of 10%.

So if the rate of return cannot be established in the real economy apart from money it also cannot be established in the world of money apart of real goods. It will be absurd to lend money without any connection to the real world - after all the role of money is to facilitate the exchange of real goods and services.

Consequently, there cannot be any separation between the real and financial market interest rates. There is only one interest rate, which is set by the interaction between individuals' time preferences and the supply and demand for money. Since the influences of demand and supply for money and individuals' time preferences regarding interest rate formation are intertwined, there are no ways or means to isolate these influences. Hence, the commonly accepted practice of calculating the so-called real interest rate by subtracting percentage changes in the consumer price index from the market interest rate is erroneous. So if the real interest rate cannot be ascertained it follows that the natural interest rate cannot be established either.

Additionally, recall that according to Wicksell the natural rate is defined as the rate at which the demand for physical capital coincides with the supply of real savings. However, the total physical demand and supply of capital cannot be established since capital goods are heterogeneous and cannot be added up to a total.

We can thus conclude that economists' and central bankers' attempts to establish the natural interest rate must therefore be regarded as an impossible mission.

Furthermore, the fact that the driving force of interest rate determination is individuals time preferences means that the causality emanates from individuals and not some other outside factor. For instance, mainstream economists generally accept that an increase in inflationary expectations automatically pushes interest rates up.

It is true that a change in inflationary expectations is likely to be reflected in higher interest rates. However, there is no automatism here since it is individuals that assess the nature of inflationary expectations and adjust their time preferences in accordance with their own circumstances. Likewise an increase in uncertainty will not automatically raise interest rates without individuals' assessments first. In short, it is individuals' assessments regarding various events that alter their time preferences and in turn the market interest rate.

The central bank and interest rates

According to the Wicksellian framework in order to maintain price and economic stability, once the gap between the financial market interest rate and the natural rate is closed the central bank must at all times ensure by means of a suitable monetary policy that the gap does not emerge. In other words, in the Wicksellian framework a monetary policy that maintains the equality between the two rates becomes a factor of stability. But is this possible? After all, maintaining this equality means that the central bank would have to manipulate the supply of money, which in turn will make things unstable.

For instance, whenever the central bank loosens its monetary stance the injection of new money into the economy benefits individuals who receive the newly created money first, and at the expense of those individuals who don't receive the new money at all, or who receive it late. The early recipients can now purchase a greater amount of goods while the prices of these goods are still unaffected. In other words, the early recipients' real wealth has increased. According to Rothbard,

The individuals who receive the new money first are the greatest gainers from the increased money; those who receive it last are the greatest losers.17

The increase in wealth also means that the early recipients of money can now undertake various projects that before the increase in money they couldn't afford - implying that, all other things being equal their time preferences will decline.18

A person with a very meagre money income can only afford means that will enable him to just sustain his physical survival. For him to undertake savings would entail a very high cost hence his time preference will be very high. However, as his purchasing power rises he can now undertake various ventures that he previously couldn't afford, which will generate benefits some time in the future. In other words, with a rise in purchasing power his time preference tends to decline i.e. he is likely to increase his savings. Consequently, this will reinforce the lowering of the interest rate in the money market by the central bank.

In other words, a fall in the time preferences of the early recipients of money provides the support for the act of lowering of interest rates by the central bank. Without this fall in time preferences the central bank's plan of lowering of interest rates in the economy couldn't be implemented. After all as we have seen financial markets without the real stuff don't have a life of their own.

Furthermore, because the early recipients of money are much wealthier now compared to before the monetary injections took place, they are likely to alter their patterns of consumption. With greater wealth at their disposal, their demand for less essential goods and services expands. The increase in the real wealth of the first recipients of money gives rise to the demand for goods which, prior to monetary expansion, would not have been considered.

A change in the pattern of consumption draws the attention of entrepreneurs who, in order to secure profits, start to adjust their structure of production in accordance with this new development. Now, on account of loose money policy entrepreneurs' find it easy to secure new loans from the banking system - an economic boom ensues.

Once however, the newly pumped money by the central bank and commercial banks starts to spread across the economy it pushes up the prices of goods and services, which undermines the purchasing power of the last recipients of money, or those who weren't recipients at all. This is likely to lift their time preferences, which in turn puts upward pressure on interest rates. In order then to sustain the lower interest rate structure the central bank must inject another dosage of new money.

Note that the act of lowering of the interest rate by the central bank leads to the diversion of real wealth from last recipients of money to the early recipients. In the process this gives rise to the various structures of production that a free market economy would not support. Again, the key to this diversion is monetary pumping, which is followed by a lowering of interest rates. There is however, a limit to all this, which is set by the pool of real funding, or the subsistence fund.19

As long as this pool is growing the central bank can get away with loose monetary policies for a long period of time. However, once the pool begins to shrink a sharp fall in economic activity ensues. This leads to the accumulation of bad debts by banks and to the subsequent curtailment of bank lending. As a result the money that sprang-up on the back of fractional reserve lending tends to evaporate.

Consequently, the fall in the supply of money sets in motion tendencies for a rise in interest rates. Note that the increase in interest rates is supported here by the rise in individuals' time preferences on account of a fall in the pool of real funding. Also note that the fall in the pool has set the platform for the disappearance of money created through fractional reserve banking. The fall in the pool of real funding raises individuals' time preferences and also sets in motion a decline in the stock of money. As a rule however, central banks tend to arrest the boom before it becomes excessive by lifting the money market interest rate once price inflation begins to rise.

We can thus conclude that even if the Fed could know the level of the natural rate, it could not achieve economic stability. The reason is that the Fed would have to pursue active monetary policies in order to maintain the natural rate target. This very act, however, leads to boom-bust cycles and economic instability. Hence there cannot be such a thing as a ‘neutral' interest rate policy.

Rather than targeting the money market interest rate towards the unknown natural rate by means of monetary tampering, which leads to more instability, a better alternative is to leave the economy alone. In a free market economy without a central bank no one would be conducting any kind of monetary policies. In the absence of central bank monetary policies, which enrich some individuals at the expense of other individuals, the interest rates that emerge will be truly neutral. In a free market then, no one would be required to establish whether the interest rate is above or below some kind imaginary equilibrium. Furthermore, in a free market with the absence of money printing there cannot be the issue of a general rise in prices that must be countered.

The likely implications of Fed's monetary policy

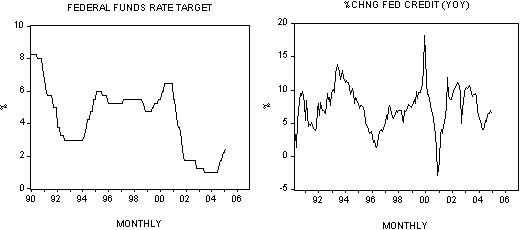

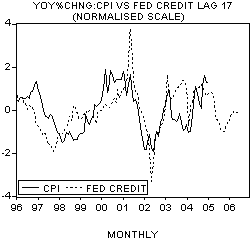

Between January 2001 and June 2004 the Fed pursued an aggressive lowering of the federal funds rate target. The target was lowered from 6.5% in January 2001 to 1% in June 2003. Since June 2004 the Fed has reversed its interest rate stance raising the fed funds rate target by 1.5% to 2.5% in early February. Now to attain a given federal funds rate target the US central bank must constantly manage the flow of money to financial markets. Changes in the Federal Reserve balance sheet, also known as the Federal Credit, depict the variability in the monetary pumping by the US central bank in order to sustain a given federal funds rate target.

For instance, year-on-year the rate of growth in the Fed Credit jumped from –0.7% in January 2001 to 12% by September 2001. Another sharp swing in the rate of growth took place between April 2003 and May 2004. The yearly rate of growth fell from 10.6% in April 2003 to 4% in May of the following year. Currently it seems that the pace of monetary injections by the Fed has stabilised at around 7%.

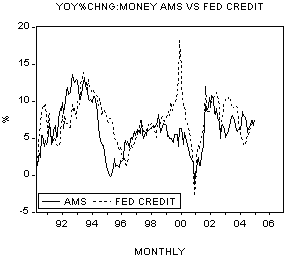

These fluctuations in monetary injections that are involved in achieving the federal fund rate target have a direct effect on the growth momentum of money AMS (see chart).

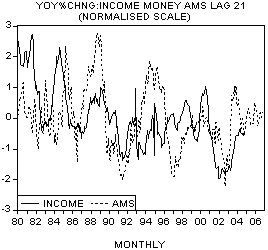

In turn, fluctuations in the growth momentum of money AMS sets, with a time lag, fluctuations in nominal economic activity. In short, the pace of money injected dictates the pace of money spent in the economy. The greater the pace of injections the greater the pace of spending is going to be, all other things being equal. We have estimated that between the 1980 to present the average time lag between changes in money and changes in nominal economic activity, as depicted by personal income, stands at 21 months (see chart).

Based on this time lag we can suggest that there is a high likelihood that the growth momentum of nominal economic activity will weaken from the second half of this year.

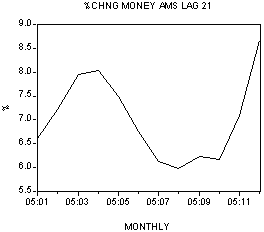

Furthermore, our monetary analysis, also indicates that the growth momentum of price inflation may actually subside (see chart).

Observe that price inflation is driven by the past actions of US central bank policy makers aimed at achieving price stability. Consequently, by responding to changes in the CPI, as prescribed by the Wicksellian framework, Fed policy makers in fact react to the symptoms of their own past policies, which generates more volatility as far as prices and economic activity is concerned.

According to the minutes of the Federal Open Market Committee (FOMC) meeting held on December 17 US central bank policy makers sent a clear signal that they are aiming at a higher federal funds rate in order to attain price stability - the ‘neutral' fed funds rate. Some experts hold that the range of this rate is somewhere between 3.5% and 5%.

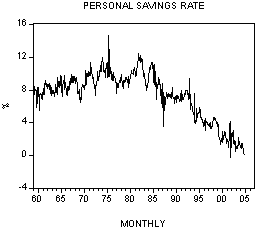

Obviously, if the Fed were to tighten its stance further this would put more pressure on various activities that emerged on the back of previous loose monetary policy. The severity of the future decline in economic activity is likely to be determined by the magnitude of the current interest rate tightening and the state of the pool of real funding, or the subsistence fund, all other things being equal. There are some indications that the pool of funding may be in trouble. For instance, the personal savings rate stood at 0.1% in December 2004 (adjusted for Microsoft dividend payments of $32 bill) against 12.5% in November 1981. Also note that the savings rate is way below its historical average of 7.3%.

Since it is quite likely that US central bank policy makers will overreact to any sudden strengthening in economic activity in coming months, it is also quite likely that central bank officials will halt or reverse the tighter stance if economic activity was to fall sharply.

Conclusion

Our examination of the framework of thinking that the Fed's decision makers use reveals that policies pursued by the US central bank will only promote more instability rather than achieving a balanced economy. The essence of the Fed's thinking emanates from writings of Knut Wicksell, who suggested that the key to economic stability is targeting the financial market interest rate at the natural interest rate.

Our analysis however, has shown that it is not possible to isolate the so-called natural rate. Consequently, policies that are aimed at an unknown interest rate target run the risk of promoting more rather than less instability. Also, even if one was to know what the natural rate was, the act of reaching and maintaining this target by means of monetary policies will destabilise the economy.

Any attempt therefore by means of policies to bring the market interest rate towards the natural rate and keep it there cannot be neutral with regard to the economy. A better way to reach healthy economic conditions is by leaving the economy free of any tampering by the central authorities. We have estimated that based on the past money supply rate of growth the growth momentum of economic activity as measured by personal income at current prices is likely to weaken from the second half of this year.

Monetary data also points to a likely softening in the growth momentum of so-called price inflation, as depicted by the CPI. Consequently, it will not surprise us if the US central bank refrains from a further tightening of its interest rate stance from Q2. It is quite likely that Fed policy makers may even abort the current tight stance altogether.

- 1Robert L. Hetzel, Henry Thornton: seminal monetary theorist and father of modern central bank. Economic Review, July/August 1987, Federal Reserve Bank of Richmond. Also, see Murray N. Rothbard, Classical Economics, An Austrian Perspective on the History of Economic Thought,Volume 2, Edward Elgar, p. 177.

- 2Knut Wicksell "Interest and Prices" Reprints of Economic Classics, New York 1965. p. 102. Originally written in January 1898.

- 3Karl Pribram, A History of Economic Reasoning, The John Hopkins University Press,1983, p322.

- 4Wicksell, p. 103.

- 5Wicksell, p. 104.

- 6Thomas M. Humphrey, "Interest rates, expectations, and the Wicksellian policy rule." Federal Reserve Bank of Richmond July 1975

- 7Wicksell, p. 107.

- 8Karl Pribram, p. 323.

- 9Wicksell, p. 108.

- 10Knut Wicksell, "Interest and Prices," A study of the causes regulating the value of money. Reprints of economic classics, Augustus M. Kelley, Bookseller, New York 1965 p189.

- 11Thomas Laubach and John C Williams, “Measuring the Natural Rate of Interest”. Board of Governors of the Federal Reserve System, November 2001.

- 12John C. Williams, "The Natural Rate of Interest," FRBSF Economic Letter, October 31,2003.

- 13Ludwig von Mises, Human Action, Contemporary Books, 3rd revised edition, p. 97.

- 14Carl Menger Principles of Economics, New York University Press, pp. 153-154.

- 15Ludwig von Mises, Human Action, 3rd revised edition, p. 483-484.

- 16Ludwig von Mises, Human Action, p. 482.

- 17Murray N. Rothbard, Man Economy, and State, Nash Publishing, p. 711.

- 18Murray N.Rothbard, Ibid, p. 380.

- 19Frank Shostak, " The Subsistence Fund," Mises.org Daily Articles, August 24, 2004.